Why Divided Lebanon Has Left a Decision on Bond Default So Late

Why Divided Lebanon Has Left a Decision on Bond Default So Late

(Bloomberg) --

Lebanon is undecided whether it should repay $1.2 billion of Eurobonds maturing on Monday or default for the first time in its history.

Prime Minister Hassan Diab will meet his cabinet on Saturday and could make an announcement soon after that.

The government, which is being advised by Lazard Ltd. and law firm Cleary Gottlieb Steen & Hamilton, has weighed several proposals in the past month. They include asking local banks to buy Eurobonds off foreign funds to make any restructuring talks easier, and getting investors to swap into new notes with lower coupons.

There’s “a fatal deadlock and an urge, once more, to gain time,” Michael Young of the Carnegie Middle East Center in Beirut, said in a blog this week. “But that useless game has reached an end.”

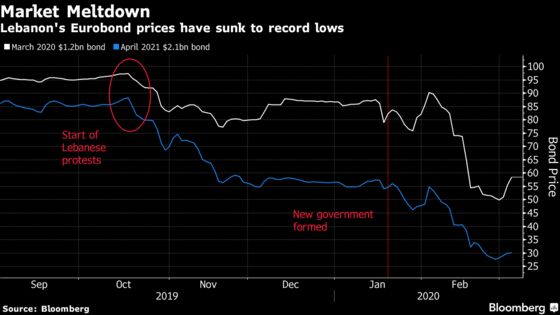

There are plenty of reasons for Lebanon to stop paying its debts: the economy is tanking, reserves are falling, inflation is in double digits and banks are restricting how much customers can transfer abroad.

Markets believe it’s only a matter of time. Lebanon’s credit default swaps -- a form of insurance for debt investors -- are the most expensive in the world. Most of its dollar bonds trade at less than 30 cents, suggesting the market expects the country to wipe roughly 70% off their value.

Yet there’s plenty of resistance to a default, especially if it forces the country to turn to the International Monetary Fund for a bailout.

Should Lebanon opt against repaying next week’s bond, the terms of which allow it a seven-day grace period until March 16, that would trigger a default on all its other Eurobonds, which total around $30 billion.

Here’s a look at the most important players:

The Government and Hezbollah

Lebanon’s government has been in power only since January, after massive protests forced the previous premier, Saad Hariri, to stand down in October. While Diab, a professor of computer engineering, has not publicly stated his preference on the bonds, he described the government’s position in bleak terms on Monday.

“The state is no longer able to protect the Lebanese and guarantee them a decent life,” he said. “We are facing immense difficulties.”

Even if he does decide on a restructuring, it’s unclear whether he’d be able to carry out the deep reforms -- such as raising taxes and ending a currency peg -- that investors might insist upon.

He and his ministers face “an impossible task,” Marcus Chenevix, a Middle East analyst at London-based TS Lombard, said. They “lack popular legitimacy, serving instead as ciphers for elite sectarian interests. A technocratic government cannot negotiate a viable path between the interests of those sectarian elites and widespread public discontent.”

Key to any decision will be Hezbollah, an Iran-backed political party that’s classified as a terrorist organization by the U.S. Diab’s government was formed only after Hezbollah gave its assent and it continues to have influence over major policies.

The group’s allies have suggested in recent weeks that default could be Lebanon’s best option. But it insists that any restructuring or reform plan cannot include a loan from the IMF, which it views as a tool of U.S. foreign policy.

That will make any resolution to Lebanon’s crisis more difficult, since the country seemingly has no other options for getting the dollars it desperately needs.

“Undoubtedly, Hezbollah holds Lebanon hostage,” said Young. “Unless Hezbollah wants the whole system to come tumbling down, with no prospect of a resolution, it will have to compromise on the IMF.”

Lebanese Lenders, Central Bank

Lebanon’s lenders, who own almost $14 billion of government Eurobonds, are firmly against a default. That would crush the financial system and worsen the economy’s plight, Salim Sfeir, head of the Association of Banks in Lebanon, said in an interview last week.

He proposes that the government swaps bondholders into longer-dated securities and announces a package of reforms to fix its finances and attract diaspora remittances, which have shriveled in recent years.

Central bank Governor Riad Salameh has said the regulator is willing to pay the debt if the government instructs it to do so. The central bank holds about $5.7 billion of Eurobonds itself.

Foreign Bondholders

Some foreigners who own Lebanon’s bonds have expressed support for a debt restructuring, saying the country’s situation is too dire to avoid that outcome.

But London-based fund Ashmore Group Plc, which manages almost $100 billion of assets, has amassed large positions in the March bond, as well as $1.3 billion of notes maturing in April and June. It’s acquired enough of those bonds to block any restructuring proposal and could make life difficult for the government.

--With assistance from Netty Ismail and Dana Khraiche.

To contact the reporter on this story: Paul Wallace in Dubai at pwallace25@bloomberg.net

To contact the editors responsible for this story: Alex Nicholson at anicholson6@bloomberg.net, Marton Eder

©2020 Bloomberg L.P.