Here’s Why Bristol-Myers Needs a $74 Billion Shot in the Arm

Here’s Why Bristol-Myers Needs a $74 Billion Shot in the Arm

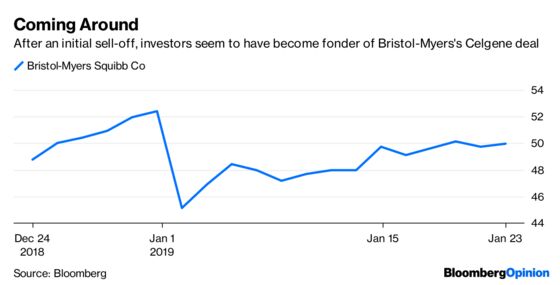

(Bloomberg Opinion) -- Bristol-Myers Squibb Co.’s impending $74 billion acquisition of biotechnology giant Celgene Inc. makes it easy to overlook something as relatively prosaic as the firm’s fourth-quarter earnings results Thursday. They do, however, provide a window into the firm’s deal motivation.

Bristol-Myers’s profit exceeded analysts’ estimates. But sluggish performances from its key medicines, blood-thinner Eliquis and immune-boosting cancer drug Opdivo, make it clear why it is gambling on a risky biotech megadeal.

Eliquis and Opdivo made up nearly 60 percent of Bristol-Myers’s sales in 2018, and both fell short of analysts’ sales estimates, as compiled by Bloomberg. While neither of the misses was by an enormous margin, both drugs carry serious risks that make signs of weakness troubling.

Bloomberg Intelligence highlighted a warning for Eliquis in Johnson & Johnson’s earnings results Tuesday. The larger firm makes Xarelto, a competing blood thinner, which also fell short of estimates, in part due to pricing pressure. Pricing may have impacted Eliquis in the quarter as well, and could dampen sales in years to come. Bristol-Myers also is in a fight over Eliquis patents that could conceivably result in earlier-than-expected generic competition.

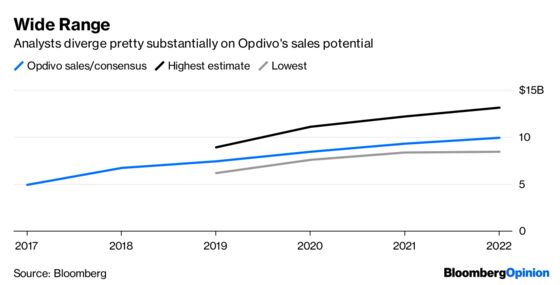

Opdivo is more important to Bristol-Myers’s bottom line, as half of Eliquis’s sales go to partner Pfizer Inc. It’s also arguably a greater risk. Sales of the drug rose 36 percent in the fourth quarter relative to the same period last year, but barely increased from the prior quarter.

Rival Merck & Co.’s Keytruda is eating at Opdivo’s market share in the hugely important lung cancer market after a series of clinical trial successes. Bristol-Myers is trying to fight back, but may be confined to something of a niche. The company has made questionable bets around Opdivo that have handed Merck the lead. It was too aggressive with an early clinical trial design and bet too heavily on a drug combination approach. On Thursday, the company announced that a prominent lung cancer effort will be substantially delayed because it needs more data. (This latest delay is the result of chasing a risky and unproven tumor-testing strategy.)

Even markets where Opdivo is doing better, such as kidney cancer and melanoma, are likely to become highly competitive over time, with six competing drugs in the same class now available.

All of this helps support Bristol-Myers’s case for buying Celgene. The biotech firm certainly comes with risks of its own. Its blood cancer drug Revlimid accounts for more than 60 percent of the firm’s revenue on its own, and potential patent issues are especially acute: Generics could start eating at sales as soon as 2020 and shave billions off of the drug’s sales potential. But Bristol-Myers got a pretty serious discount as a result. The deal was the lowest-valued big biotech deal in recent history. That at least somewhat mitigates the Revlimid risk. Celgene’s large roster of interesting pipeline projects helps as well.

The rewards could be great. Celgene could generate $50 billion in cash flow over time and help propel Bristol to industry-best earnings growth. And though the deal adds more exposure for Bristol-Myers, it also diversifies its risk.

Bristol-Myers will likely continue to project optimism about its blockbuster drugs. But its actions speak louder than words.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Max Nisen is a Bloomberg Opinion columnist covering biotech, pharma and health care. He previously wrote about management and corporate strategy for Quartz and Business Insider.

©2019 Bloomberg L.P.