Foreigners Rush to Lend Billions to Europe Inc. in Global Shift

Who Needs ECB as Foreigners Seen Rushing to Lend to Europe Inc.

(Bloomberg) --

Christian Hantel is exactly the kind of investor European companies are wooing as they adjust to a world of diminished monetary largesse.

Based in Zurich, he channels cash from outside the eurozone, the kind that corporate borrowers from the 19-member bloc on the potential precipice of another decade of economic stagnation need as the European Central Bank retreats.

The money manager at Vontobel Asset Management is at the vanguard of a wave of foreigners that will bring 35 billion euros ($39 billion) to the region this year and is poised to replace the ECB as the single largest investor, according to HSBC Holdings Plc.

It’s a big bullish claim. And it’s stirring debate in credit circles about how far the region’s issuers can rely on the kindness of strangers to soften the hard reality of political risk and the prospect of a slowdown in corporate-revenue growth.

“We expect a sustained internationalization of the euro credit investor base,” according to HSBC credit strategists Song Jin Lee and Peter Barnshaw in a recent note.

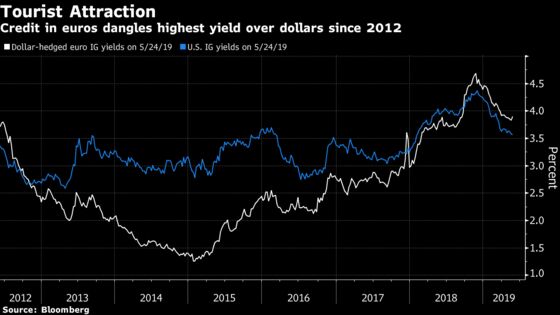

European credit markets need new friends. Since 2015, they’ve suffered dwindling purchases from abroad and seen mixed demand at home in the past year. Right now, the most favorable hedging costs in seven years bolsters their case.

But HSBC’s roadmap faces all manner of political and technical bumps. For one, not even Hantel thinks the world’s investors will follow his example.

Investors chasing currency-adjusted yields could leave as quickly as they came, Hantel warns. “Many investors are very opportunistic,” he said. “If the currency hedge looks favorable, they will buy and if not, they will pull back.”

Hantel, who helps oversee 118 billion Swiss francs ($117.2 billion), is taken by hedging math in favor of euro credit for now, like many of his peers with global portfolios.

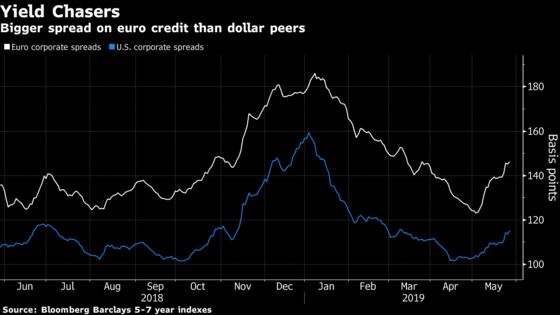

But it’s obviously only part the equation; relative credit spreads also drive the investment calculus. Over the past year, euro credit has largely paid bigger premiums. Bonds due in five-to-seven years offer an average premium of 148 basis points to government benchmarks, according to Bloomberg Barclays index data, a pick-up of about 30 basis points over U.S. peers.

Even if euro debt is relatively cheap, it’s dogged by patchy trading that may deter those who want liquidity. And America is where all the action is. The average daily trading volume of U.S. corporate bonds stood at $26.8 billion in April, based on Trace data. In Europe, daily trading barely exceeded $6.2 billion, according to MarketAxess.

Political risk in Europe is likely to keep the foreign bid fickle as well. A wellspring of populism underscored results of the European parliament election while Italy heads for a showdown with Brussels over its budget.

“European politics is the biggest hurdle for global investors to come to European credit,’’ said Henrietta Pacquement, portfolio manager at Wells Fargo Asset Management, which oversees $466 billion. “Global flows into Europe hinge on no negative news for a few months. It takes time for things to get into gear.’’

The latest available ‘Who-to-whom’ statistical report from the ECB showed the stock of corporate debt held by foreigners at 238.9 billion euros in the fourth quarter, down from 254.4 billion euros the year before. The central bank now only reinvests proceeds from maturing bonds to maintain the size of the portfolio, now 177.7 billion euros.

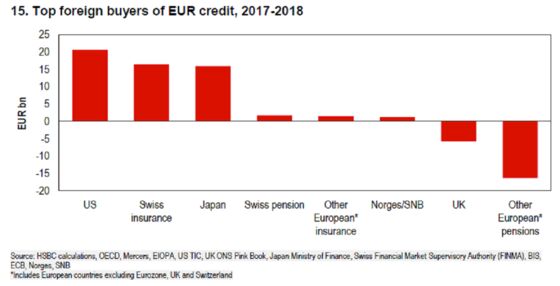

Last year Americans, Swiss insurers and Japanese investors were the top three buyers of euro credit in 2018, while U.K. and other European pension funds were net sellers, according to HSBC.

And there are compelling forces to keep them coming back.

Japanese investors buying high-grade bonds in euros and swapping them back to yen now earn higher yields than they would get from U.S. dollar bonds. No surprise then that they’ve been scooping up from everything from plain-vanilla corporates to risky bank debt to collateralized loan obligations, where Japan’s Norinchukin Bank has established itself as an anchor investor of European CLOs.

“Non-Eurozone investors will be the key pillar of demand for euro credit in 2019,” according to HSBC credit strategists.

To contact the reporter on this story: Tasos Vossos in London at tvossos@bloomberg.net

To contact the editors responsible for this story: Hannah Benjamin at hbenjamin1@bloomberg.net, Cecile Gutscher, Sid Verma

©2019 Bloomberg L.P.