Who Are You Going to Trust, Adjusted Earnings or Your Lying Eyes?

Who Are You Going to Trust, Adjusted Earnings or Your Lying Eyes?

(Bloomberg Opinion) -- Corporate executives and their accountants have long contended that the use of adjusted earnings, which ignore costs like acquisition expenses, interest payments or just about anything they find inconvenient, gives investors a better picture of companies’ performance. Under no circumstances is it manipulation, they say. But a new study suggests it just might be.

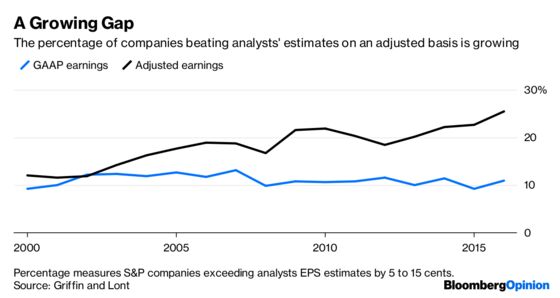

The study, which will be presented for the first time on Tuesday at the American Accounting Association’s annual meeting, found that over the past decade or so, as more and more companies have shifted to emphasizing adjusted earnings, the percentage of companies in the S&P 500 Index that consistently report better-than-expected earnings by a relatively wide margin on that basis has increased. But those same companies’ results under generally accepted accounting principles, or GAAP, often only match or slightly exceed analysts’ predictions.

The authors of the study, Paul Griffin of the University of California at Davis and David Lont of the University of Otago in New Zealand, say that suggests those adjusted earnings are manipulated. Worse, Griffin and Lont found that the adjustments companies make are often asymmetric, meaning they regularly include one-time gains that boost earnings but exclude temporary costs that would drag them down. “There are those who might claim that so far this century the U.S. economy has experienced such an unusual period of economic growth that it has taken analysts and investors by surprise each quarter … for almost two decades,” Griffin and Lont write. “This view strains credulity.”

The key to the study is that it matches up adjusted earnings results with analysts’ estimates that tried to factor in those adjustments in advance, and GAAP results with estimates based on standard accounting metrics. Griffin and Lont looked at hundreds of thousands of quarterly earnings forecasts and reports of 4,700 companies over 17 years.

Griffin and Lont believe companies now shoot well above analysts’ targets because consistently beating earnings per share by only a penny or two became a red flag. If they pull out all the accounting tricks to get their earnings much higher than expected, according to Griffin and Lont, then they are less likely to be accused of manipulation.

There is a slightly less nefarious explanation, though not any less troublesome. Stocks go up when companies beat their numbers. And analysts are generally biased toward wanting the stock they cover to go up. There are far more buy ratings on Wall Street than there are sell recommendations. So it may be the analysts who are setting their estimates lower so the companies can beat them, and adjusted earnings are making it easier for them to do it.

Regardless of who’s leading in the adjusted-earnings dance, it’s the same discordant tune for investors, and there’s little help on the way. The Securities and Exchange Commission has blessed the use of adjusted results as long as companies disclose how they are calculated. Those disclosures don’t go far enough and they are easy to get around when it comes to forecasts. Worse, adjusted earnings are used to determine executive bonuses and whether companies are meeting their loan covenants. No wonder CEO pay and leverage goes up and up.

That leaves investors in the world of adjusted earnings, where every company is way above average every quarter. Imaginary worlds are nice, it’s just impossible to live there.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2018 Bloomberg L.P.