We Can’t Give You a Loan, CLO Managers Told Now Bankrupt Deluxe

We Can’t Give You a Loan, CLO Managers Told Now Bankrupt Deluxe

(Bloomberg) -- When Deluxe Entertainment Services Group Inc. was struggling to stay afloat earlier this year, its lenders wanted to give it money. But their investment rules blocked them, a twist that could have a wide-reaching impact on distressed U.S. companies.

The lenders in this case were collateralized loan obligations, or groups of loans that asset managers package into bonds. Those investment firms are increasingly powerful in debt markets and have strict rules limiting when they can give more money to troubled borrowers. In the case of Deluxe, an ill-timed ratings downgrade prevented CLO managers from fronting more cash.

When Deluxe sought new funds, CLO managers said, “We can’t give you a loan,” according to the company’s lawyer Jon Henes of Kirkland & Ellis LLP. That limited its ability to get money outside of bankruptcy, Henes told a New York court after the media company filed for Chapter 11 protection from creditors.

A representative for Deluxe said the company looks forward to emerging with a “significantly stronger balance sheet” and completing the process quickly, in an e-mailed statement to Bloomberg.

CLOs are the biggest holders of loans to junk-rated companies, which is a $1.2 trillion market. The CLO market has mushroomed in recent years as investors have clamored for higher-yielding bonds. Concerns are mounting about how the structures owning so much of corporate America’s debt will react when a recession hits and the number of company downgrades rises.

“When the downturn does come,” with CLOs involved in capital structures, it’s going to be an “interesting process to get all of these companies restructured,” Henes said in court.

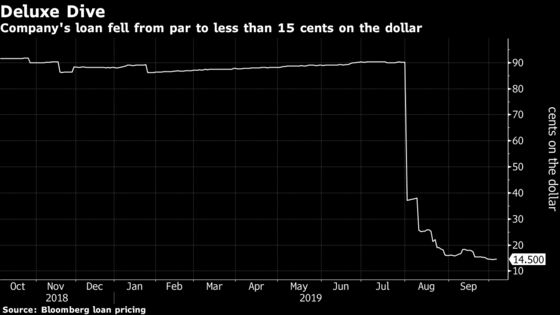

Deluxe, backed by Ron Perelman’s MacAndrews & Forbes Inc., had avoided filing for bankruptcy protection for years, continually raising new money to give it more breathing room to turn itself around. Amid an effort to curb its $1 billion debt load, it had considered spinning off its creative services business, planning to use proceeds to help manage those obligations. It dropped that plan in favor of a $73 million loan from its lenders after winning their support.

Deluxe Downgraded

In August, soon after Deluxe ended the spinoff plan, S&P Global Ratings downgraded the company three notches to CCC-, citing the company’s risk in refinancing maturing debt. Later that month, Deluxe said it had entered a restructuring support agreement with its lenders, which sought to swap debt for equity and raise additional funds.

The ratings downgrade blocked some lenders from participating in new financing the company was seeking under the restructuring. The documentation for most CLOs prevents the firms that manage the underlying loans from holding more than 7.5% of their portfolios in CCC rated loans. Some of the CLO managers had sought advice from lawyers around their documents, but a number told the company they’d be unable to provide a new loan, Henes said.

Those that were able to -- either because they’d not maxed out their CCC rated capacity, or because they were among the few deals that have expanded capacity to buy more than 7.5% -- were able to provide new capital to support the company to where it ended up: in bankruptcy court.

The events underscore the reason why regulators globally have expressed concerns about the CLO industry. Still, others in the industry point to the lack of defaults on senior tranches and say many of their investors are long-term holders that won’t be forced to sell in a rout.

To contact the reporter on this story: Katherine Doherty in New York at kdoherty23@bloomberg.net

To contact the editors responsible for this story: Rick Green at rgreen18@bloomberg.net, Sally Bakewell, Dan Wilchins

©2019 Bloomberg L.P.