Wayfair Can’t Relax on the Easy Chair of Sales Growth

Wayfair Can’t Relax on the Easy Chair of Sales Growth

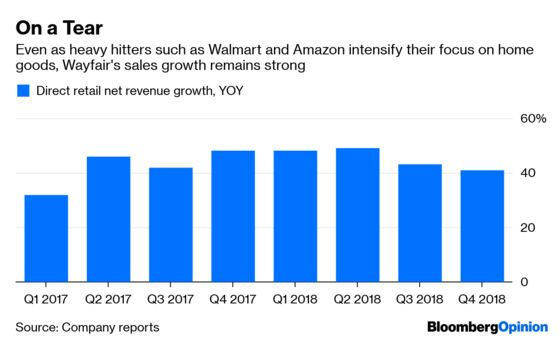

(Bloomberg Opinion) -- No one should be surprised that Wayfair Inc.’s earnings report on Friday showed that it had a gangbusters holiday season, with retail sales growing 41 percent from a year earlier.

After all, the digital home-goods seller had already said its sales were up 58 percent from a year earlier during the five-day stretch that includes Black Friday and Cyber Monday, suggesting it had started the season with a bang.

Other figures in Wayfair’s fourth-quarter earnings report also suggested strength and helped send its shares up more than 32 percent in morning trading to a record high. Active customer count rose to 15.2 million, up 38 percent from a year earlier. And repeat customers placed a greater share of orders, a sign it is cultivating customer loyalty.

I noted last year that Wayfair was going to have a fresh challenge from a field of formidable competitors that were more intently focused on the online home goods business, including behemoths Walmart Inc., Amazon.com Inc. and Target Corp. It’s impressive that Wayfair has been resilient to these challenges from far larger players.

Yet I’m still finding it difficult to completely throw aside caution about Wayfair’s long-term prospects. Its operating expenses as a percentage of sales have climbed as it plows millions of dollars into developing its software and logistics network. With a net loss in 2018 that was more than double that of the previous year, that’s particularly concerning.

Its long-term target for operating expenses is 15 to 19 percent, and it’s simply hard to feel confident Wayfair can achieve that given that it has moved even further away from that range despite blockbuster sales growth.

Also, Wayfair is an insurgent in the home goods business in the sense that it’s a relatively new entrant and that its business model is different. But its size is now more like that of an incumbent. Wayfair’s sales in 2018 totaled $6.7 billion, a figure that almost certainly will catapult it on a revenue basis past Williams-Sonoma Inc., the corporate parent of the eponymous chain as well as Pottery Barn and West Elm. And the company said in a Friday presentation that it has 89 percent “aided awareness” in the U.S., meaning the vast majority of shoppers in its largest market have heard of it.

So why does it still have to spend so much on marketing? The company’s advertising spending equaled 11.4 percent of sales in fiscal 2018. While that is down slightly from the previous year, it is still far above the company’s long-term target of 6 to 8 percent.

Building awareness in new overseas markets is clearly fueling some of the spending, but I can’t help but fear that when Wayfair taps the brakes on this, the revenue growth is going to cool, too.

We’ve seen this happen before to a digital swashbuckler. Blue Apron Holdings Inc. pulled back its marketing spending as it grappled with some operational challenges that made it difficult to fulfill orders accurately. As it did so, customers disappeared. To be fair, this is not a perfect comparison because Blue Apron has a more niche business model and is far smaller than Wayfair. But it raises questions about how much these digital-first disruptors can keep growing their ranks of customers when they are not spending heavily to do.

I commend Wayfair for navigating a changing competitive landscape and for making smart choices, such as expanding its private label offerings. But it’s time for it to show more progress in places other than top-line growth.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Sarah Halzack is a Bloomberg Opinion columnist covering the consumer and retail industries. She was previously a national retail reporter for the Washington Post.

©2019 Bloomberg L.P.