Wayfair Climbs to Record as E-Retailer's Results Rack Up a Win

Wayfair Climbs to Record as E-Retailer's Results Rack Up a Win

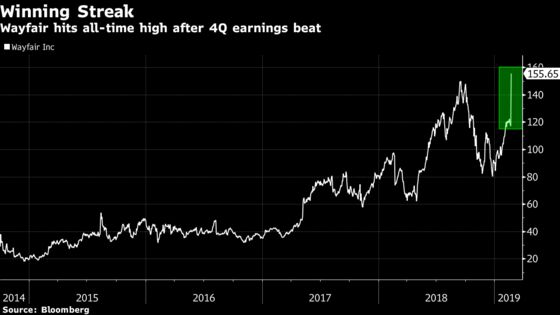

(Bloomberg) -- Wayfair Inc. shares jumped to their highest since the 2014 initial public offering as fourth-quarter sales soared more than 40 percent and results beat the Street’s expectations after a banner holiday season.

"W delivers a W in the fourth quarter," Oppenheimer analyst Brian Nagel wrote. "As the Wayfair model continues to take shape, we expect more traditional consumer-type money to flow into these shares."

Wayfair appeared to avoid macroeconomic pressure tied to the partial shutdown of the U.S. government and investments look to be paying off nicely, analysts wrote. However, the net loss in 2018 more than doubled from a year earlier. Bloomberg Intelligence analyst Seema Shah notes that company appears to be focused on growth and market share gains, rather than just being profitable.

The meteoric share jump was partly fueled by shorts exiting their positions, said a D.A. Davidson analyst who is a bear on the stock. Financial analytics firm S3 Partners shows short interest in the stock in the stock has climbed since its October 12-month low, reaching 27 percent of the shares available to trade.

The stock rose as much as 34 percent at 12:46 p.m. in New York as the S&P 500 increased less than a percent.

Here’s what Wall Street is saying:

Oppenheimer, Brian Nagel

Wayfair took another step forward as it saw direct retail accelerating and topping guidance with house brands resonating well with consumers.

The earnings proved supportive of the firm’s positive, longer-term stance on the shares as "sector sales growth is increasingly leveraging a dynamic expense infrastructure."

Repeat customers placed about two-thirds of orders in the quarter, a new high-water mark for the company.

Rates outperform PT $140

Baird, Colin Sebastian

The company is seeing little impact from macro-headwinds.

“The results demonstrate continued strong top-line growth as investments are paying off through positive repeat customer trends, and complemented by higher gross margins and a return to U.S. segment profitability.”

The first-quarter 2019 outlook reflects a “high level of confidence in the business,” and the revenue forecast was “better-than-feared.” However, he noted that the Ebitda margin forecast of -5.5 percent to -5.2 percent is below the -3.6 percent consensus, driven by investments in advertising spend, global logistics investments and the carry-over impact from 2018 hiring.

Rates neutral, PT $108

D.A. Davidson, Tom Forte

Wayfair doesn’t seem to be seeing negative macro-environment pressure from the U.S. government shutdown and Brexit, Forte said in a phone interview. He said shares also rose as a result of the company’s ability to leverage the trend of customers willing to consume advertising on e-commerce platforms and as a result of short covering.

Forte is one of two bears on the stock, saying that until the company shows “an ability to maintain elevated sales growth while scaling back investment spend, it’s hard to recommend shares.”

Rates underperform, PT $60

Loop Capital, Laura Champine

Loop raised revenue estimates for 2019 to $200 million above consensus, based on strong customer growth as Wayfair continues to invest in advertising and “e-commerce takes share from brick-and-mortar competitors.”

Expects Wayfair’s “early mover advantage in the home furnishings category to prove sustainable, with its best-in-class selection, personalized marketing, and price leadership as its key competitive advantages.”

Rates buy, PT $155 from $145

To contact the reporters on this story: Natasha Rausch in New York at nrausch@bloomberg.net;Rebecca Choong Wilkins in New York at rchoongwilki@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Will Daley

©2019 Bloomberg L.P.