Watching the Global Flows Explains Why the Dollar Won't Be Kept Down

Watching the Global Flows Explains Why Dollar Won't Be Kept Down

(Bloomberg) -- The dollar’s resilience after what some have categorized as the most dovish Federal Reserve turnaround in history comes as little surprise to Exante Data’s Jens Nordvig.

U.S. President Donald Trump may be looking to jawbone the greenback. But for Exante, it’s still all about the grab for yield, with rates on dollar-denominated assets remaining more attractive relative to the painfully low or negative ones found in Europe and Asia. The firm’s analysis of the holdings of global asset managers suggests that isn’t going to change anytime soon.

Exante’s flagship global flow analytics product aggregates fund managers positioning in fixed income and currencies to pinpoint extremes. It’s readings -- which have helped snag Exante clients willing to pay $60,000 a year for its insights -- include gauges of activity tied to carry trades.

Inflows into this strategy, a bet in which an investor borrows in a lower-yielding currency and invests in one with higher rates, using purchases of dollar-denominated assets surged this quarter to multiyear highs. That’s come even as Fed Chairman Jerome Powell and his colleagues have indicated a resolve to stand pat on policy normalization for now.

“People are using the dollar as the long in the carry trade, with European investors still having very little to buy at home that they can accumulate yield in,” said Nordvig, who launched Exante in 2016. “You can absolutely see this in the global fund flows we track. It really explains the dollar holding up in the face off this U-turn by the Fed.”

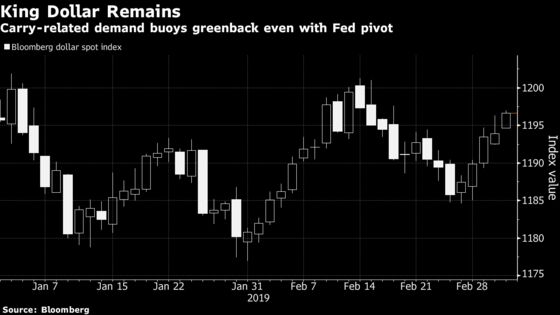

The Bloomberg Dollar Spot Index is barely changed this year, while money-market traders have pretty much priced out all Fed hikes for 2019 and see a cut as the most likely path for 2020. The greenback was stronger Wednesday, with the Bloomberg gauge up about 0.2 percent to 1,197.84.

Low volatility in currencies has also been a boon to carry trades, as it reduces the chance that changes in currency values will erode gains made on interest-rate differentials. A JPMorgan Chase & Co. option index of swings in global currencies has tumbled to about 7 percent from 9.4 percent in January.

Exante aggregates and filters reams of fund holdings, then breaks the data down into individual currency exposures. The firm pulls from publicly-distributed sources, pays some managers directly for information and uses joint ventures with data providers for intelligence of other funds’ positioning. The New York-based team then uses quantitative tools to piece it all together and model it.

While some of the biggest hedge funds likely are doing similar analysis, they aren’t sharing it. That’s helped Exante attract clients, to several dozen from just a few when the first began about two and a half years ago.

One of the firm’s clients is Sao Paulo-based Verde Asset Management, whose chief investment officer is Luis Stuhlberger. He’s became one of the most revered managers in Brazil after posting a total return of over 16,000 percent since his fund’s inception two decades ago.

“What’s key to us about Exante is its ability to put a lot of data sources into one single place and make it coherent and then help us with what story that data is telling,”said Luiz Parreiras, chief strategist and portfolio manager at Verde, which has about $9 billion in assets. “We as of the fourth quarter were getting very bullish on Brazil. Exante’s data helped us believe that the move has a lot of legs because positioning across EM was fairly low.”

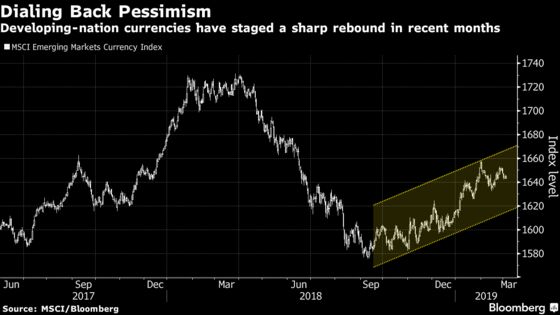

Exante’s data showed in the fourth quarter, during a rout in emerging markets, that global fund managers’ allocation to the region overall had fallen to about zero. That compared to about a 5 percent to 10 percent average allocation to emerging markets and marked an extreme level of pessimism that only happens every five to six years, said Nordvig, who advised clients that a reversal was coming. Emerging markets shares and currencies have mostly rebounded since.

Another value of Exante for Verde is what Nordvig’s team and its indicators can tell them about the intricacies of foreign-exchange dynamics in China.

This is important because the yuan is a “heavily-intervened currency and China is a country where there are massive capital controls and a lot of opacity in terms of what is really happening,” Parreiras said.

Trump and Chinese counterpart Xi Jinping are still trying to come to an agreement on trade, with the U.S. asking China to keep its currency stable. The U.S. president deferred a March 1 deadline that would have triggered a batch of new tariffs on China.

But even Nordvig admits positioning data has its limits, such as the unanticipated hit India’s currency and debt incurred upon escalating friction with Pakistan.

“Our capital flow data on emerging markets has remained very bullish but then India attacked Pakistan,” said the 44-year-old Nordvig. “That’s the kind of stuff that we can’t pick up in the flows. But still, people do always want to know how real money is positioned.”

--With assistance from Sarah Wells, Tian Chen and Ben Bartenstein.

To contact the reporter on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, ;Jeremy Herron at jherron8@bloomberg.net, Dave Liedtka

©2019 Bloomberg L.P.