‘Convexity Hedging Beast’ Blamed for Lower Bond Yields

‘Convexity Hedging Beast’ Blamed for Lower Bond Yields

(Bloomberg) -- Analysts and traders are blaming an increasingly familiar culprit for last week’s plunge in bond yields -- and they’re asking if it’s just the beginning.

At issue is the relationship between bond yields and the impact of their decline on different portfolios. For large investors who hold mortgages, like money managers and banks, a drop in rates means the duration of these portfolios tends to fall since mortgages have negative convexity. This leaves the holders scrambling to compensate by adding duration to their holdings in a phenomenon known as “convexity hedging.”

There are similar hedging needs from those using derivatives to bet on market stability and insurance companies whose liabilities are rising as a result. This hedging activity can wind up exacerbating the moves in interest rates, as was said to be the case in March, when the spread between 3-month and 10-year U.S. Treasuries inverted for the first time in over a decade.

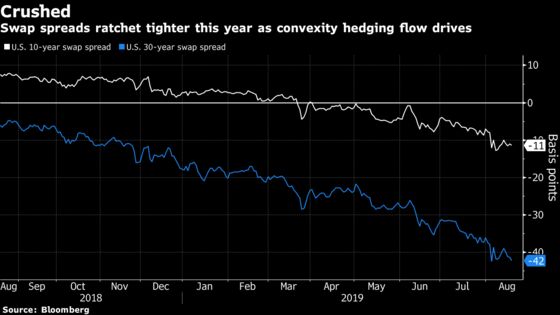

Once again, analysts are pointing to swap spreads for evidence of big investors reaching for interest rate derivatives to tweak their portfolios in the face of falling bond yields. As of Friday’s close, the yield on the benchmark 10-year U.S. Treasury had dropped 46 basis points in August to 1.55%, while the rate on equivalent maturity swaps declined by 50 basis points.

JPMorgan analysts led by Josh Younger estimate that convexity hedging has totaled roughly $90 million per basis-point move in bond yields since the end of last month.

“Taking a longer view, the dollar duration of year-to-date convexity flows is now comparable to that triggered by the 2008 financial crisis,” the analysts wrote in a note published late last week. “It suggests that we have in fact entered a new regime in which convexity hedging is impacting not just spreads -- as is usually the case -- but duration as well, though with swaps as the primary instrument through which this risk is delivered.”

The moves beg the question of whether convexity hedging is likely to pick up or ease. JPMorgan says current levels in rates are close to ‘maximum negative convexity’ for mortgages and investors may need to hedge portfolios further. “The longer we remain at depressed levels the more likely banks are to look to add duration,” they said.

Analysts at Barclays, HSBC and Morgan Stanley, among others, have slashed forecasts for 10-year Treasuries, suggesting this could just be the start.

“The convexity hedging beast is likely to awaken soon,” TD Securities strategist Ned Rumpeltin wrote on Aug. 15. “Specifically, the fall in rates to levels not seen since 2016 and the drop in stocks increase the odds of convexity hedging from mortgage servicers, REITs, short gamma players and insurance companies.”

To contact the reporters on this story: Tracy Alloway in Hong Kong at talloway@bloomberg.net;Stephen Spratt in Hong Kong at sspratt3@bloomberg.net

To contact the editors responsible for this story: Tracy Alloway at talloway@bloomberg.net, Joanna Ossinger, Tan Hwee Ann

©2019 Bloomberg L.P.