Warren Buffett's Next Deal Will Be His Most Important

Warren Buffett's Next Deal Will Be His Most Important

(Bloomberg Opinion) -- Everybody wishes they knew what Warren Buffett will acquire next. Buffett wishes he knew, too.

For the 88-year-old chairman and CEO of Berkshire Hathaway Inc., the next purchase won’t be just another deal amid decades of doing them. It could be Buffett’s final “elephant-sized” acquisition and one that leaves a lasting imprint on Berkshire. The billionaire wrote in his annual letter to shareholders in February that just the thought of doing another megadeal “is what causes my heart and Charlie’s to beat faster.” (“Charlie,” of course, refers to his 95-year-old business partner, Charlie Munger.)

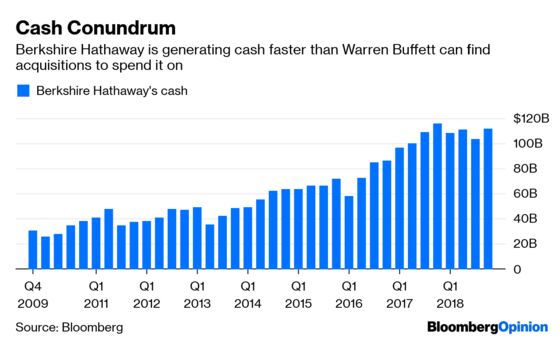

Berkshire’s last megadeal was the $37 billion purchase of Precision Castparts, which closed in February 2016. The world’s most renowned dealmaker has struggled to find another suitable big target, even though with more than $100 billion of cash at his disposal one would think possibilities abound. Buffett won’t want to leave his successor – who already has such big shoes to fill – the added challenge of figuring out what to do with such an unproductive level of cash, so my guess is Berkshire will strike soon.

With crystal balls in short supply to predict Berkshire’s next move, it helps to go back to the basics. Recall how Berkshire’s past acquisitions share two main qualities: 1) They usually fit certain financial criteria, and 2) the businesses were – how do I put this – just oh, so very Buffett. There was the railroad, the batteries, industrial parts, truck stops, utilities, and so on.

Lately, investor speculation has centered on airlines, according to a Bloomberg News story last week. That’s because Buffett – at one time totally averse to the industry – has taken quite a liking to it again. Since late 2016, Berkshire has been the biggest shareholder of Delta Air Lines Inc. It’s also the second-largest holder of Southwest Airlines Co., United Continental Holdings Inc. and American Airlines Group Inc. All together, those stakes are worth $9 billion, almost 5 percent of Berkshire’s equity portfolio.

According to my tracker of potential Berkshire takeover candidates, both Delta and Southwest technically do meet Buffett’s criteria for takeover targets. He looks for consistently profitable businesses with high returns on equity. (As an aside, that this now describes the airline industry shows how consolidation has reduced competition to the detriment of travelers, as my colleague Joe Nocera wrote last week.) Buffett also prefers businesses with little to no debt and relatively cheap share prices.

But would Buffett really buy an airline? I’m not so sure. By owning stakes in all the biggest U.S. carriers, Buffett seems to be making a bet on the industry rather than looking to acquire a single one – would he exit the other stakes to do so? It also just feels like the idea is missing that Buffett flavor. (To be fair, some of Berkshire’s recent stock-market choices – such as buying Red Hat Inc. and a large, short-lived position in Oracle Corp. – were out of the box by Buffett standards.)

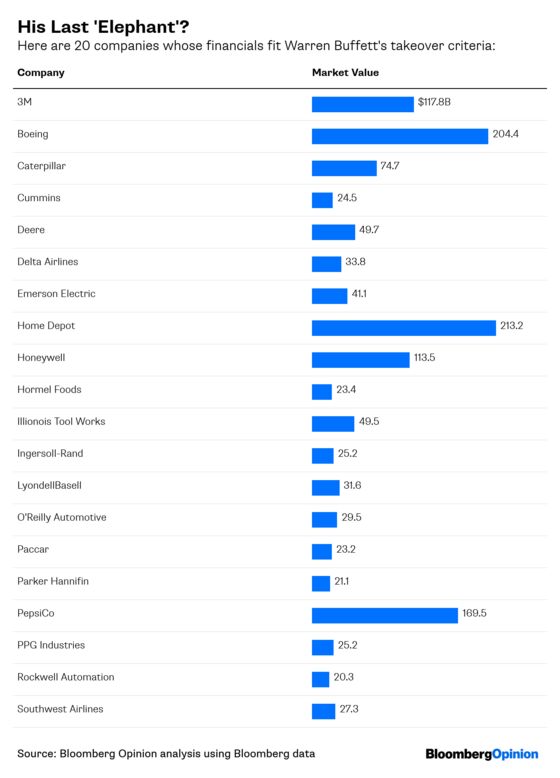

There are a number of companies that have all the hallmarks of a Buffett target, beyond just their financial metrics – brands with durability that remain part of America’s economic pulse. They include companies such as machinery manufacturer Caterpillar Inc., adhesives maker 3M Co., tractor supplier Deere & Co. and home-improvement retailer Home Depot Inc., to name a few. Here’s a list of some select names from my financial screening (I’ve left out the really outlandish ones that filter through, although some of these may still be too large for even Buffett’s appetite):

At 88, Buffett himself may not be slowing down yet – in fact, he told me last fall that he’s busier than ever. But the cadence of M&A at Berkshire has been disrupted due to a combination of richly valued targets and increased competition for the best ones. Berkshire’s deal for Texas utility Oncor fell apart in 2017. That was after Kraft Heinz Co. was rebuffed by Unilever, another megadeal Berkshire was going to help bankroll. Buffett also recently admitted to overpaying for the merger of Kraft and Heinz, after the packaged-food maker disclosed a $15.4 billion writedown, a Securities and Exchange Commission subpoena and a dividend cut alongside earnings in February – evidence that Buffett’s trust in 3G Capital was misplaced.

After the Kraft Heinz ordeal, and with so much buildup now for Berkshire’s next acquisition, maybe the he should just return to his roots.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tara Lachapelle is a Bloomberg Opinion columnist covering deals, Berkshire Hathaway Inc., media and telecommunications. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.