Wall Street Swaps Steepening for Inversion in a Yield-Curve Bet

Wall Street Swaps Steepening for Inversion in a Yield-Curve Bet

(Bloomberg) -- Investment banks are offering a fresh way to profit from a U.S. yield curve flashing renewed warnings of recession.

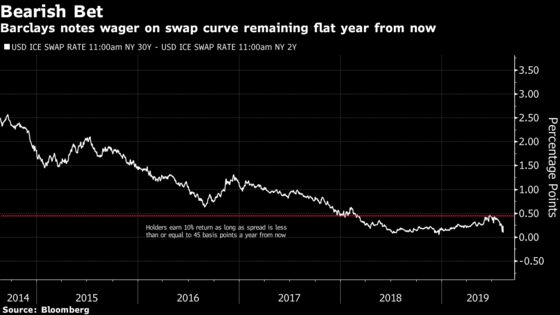

Barclays Plc has sold $2 million worth of structured notes that benefit if the U.S. swap curve fails to steepen materially, or if it inverts a year from now. The product would typically pay off in a scenario in which bond investors fear the outlook for growth and inflation, amid diminished Federal Reserve firepower.

It appears to be the first issued this year by a major investment bank riding a flatter yield curve.

Wall Street tends to sell a slew of “steepeners” that profit from a wider gap between short- and long-term rates, commonly associated with a bullish growth environment.

Buyers of the Barclays notes might be subscribing to one of Wall Street’s oldest but most dangerous maxims: “This time it’s different.”

The Treasury curve has generally tended to steepen amid Fed easing cycles, as shorter-dated maturities are more sensitive to the decline in policy rates than longer-term debt. Monetary accommodation in theory should also boost the inflation-risk premium, a negative for longer-dated bonds.

But not everyone’s convinced that past will be prologue this time.

Bob Michele, chief investment officer at JP Morgan Asset Management, told Bloomberg TV to “throw the history books away” earlier this year. As short-term rates fall, buyer interest will migrate to intermediate and longer-dated Treasuries as investors seek to avoid increasingly paltry returns, he said. That would lead to a curve that’s “as flat as a pancake,” he said.

The Treasury two-to-10-year cash curve, which has been flattening for much of the last two years, inverted last week on both sides of the Atlantic after a wave of soft economic data globally. The U.S. curve steepened Monday after the government said it would reach out to investors on the potential issuance of 50- or 100-year bonds.

The spread between the 30-year and 2-year swap rates currently sits at around 9 basis points. With the Barclays notes, as long as that gap stays under or equal to 45 basis points, investors receive a 10% return in about a year’s time. Noteholders lose 1% of their principal for every one-basis point increase over 45 basis points, up to a maximum loss of 15%. A spokesperson for Barclays declined to comment.

Globally banks have sold more than $4 billion of notes linked to the spread between short- and long-term swap rates this year, according to data compiled by Bloomberg. Virtually all these products reflect wagers on the curve steepening, or at least dodging a material inversion.

To contact the reporters on this story: Yakob Peterseil in London at ypeterseil@bloomberg.net;Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Todd White, Sid Verma

©2019 Bloomberg L.P.