Wall Street Sees Treasuries Yield Curve Flattening Into 2019

Wall Street Sees Treasuries Yield Curve Flattening Into 2019

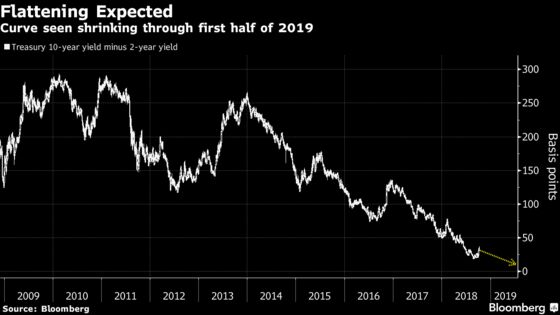

(Bloomberg) -- This month’s bond-market slump hasn’t jolted the majority of Wall Street strategists from one core view: that the Treasuries yield curve will keep flattening well into next year.

Strategists at most of the Federal Reserve Bank of New York’s primary dealers expect the spread between 2- and 10-year yields to narrow through the first half of 2019, according to yield forecasts compiled by Bloomberg. From about 30 basis points now, the average prediction is for the gap to shrink to 21 basis points by year-end, and to about 11 basis points by June. Still, it may be a bumpy ride, with forecasts for mid-2019 ranging from a 30 basis point inversion to a positive slope of a half-point.

The key to the majority view is the expectation that the Fed will keep tightening, while subdued growth and contained inflation cap longer-maturity yields. Further flattening could make things uncomfortable for those leaning the other way. It may also be problematic for policy makers because some investors see the march toward inversion as signaling a recession.

“The flattening continues, and it’s really a grind,” said Shahid Ladha, head of Group-of-10 rates strategy for the Americas at BNP Paribas. “It’s painful for the Fed. It’s also painful for the market.”

The climb in yields gained momentum at the start of this month, pushing the benchmark 10-year rate to the highest since 2011 and sparking the biggest jolt of curve steepening since February. The reversal led some strategists to conclude that flattening had run its course. The curve narrowed in August to levels last seen in 2007, which is also the last time it was inverted.

‘Flashing Yellow’

“The bond market is sending us flashing yellow signs, saying, ‘Hey, it may not be all roses looking ahead,”’ Minneapolis Fed President Neel Kashkari, who doesn’t vote on monetary policy this year, said this month.

Twenty of the 23 primary dealers contributed yield forecasts to the survey. At least five see the curve from 2 to 10 years inverting by the end of September next year, with some saying that will happen as early as the first quarter. In the view of Barclays Plc, yields at the front end will keep climbing while those on the 10-year will stay near 3 percent. The bank forecasts an inversion to minus 10 basis points by the end of March and to minus 25 by the end of the third quarter.

“Even though the fiscal stimulus is lifting near-term growth, we don’t think it materially changes the outlook over the medium- to long-term,” said Anshul Pradhan, a Barclays strategist. “Growth is likely to move back down toward a subdued trend.”

But several banks disagree. Deutsche Bank AG, for example, expects a spread of 50 basis points at mid-year. Jefferies LLC sees that level by the end of September 2019 amid reduced pension-fund demand and European Central Bank accommodation, along with increased longer-maturity issuance as deficits deepen.

“You are going to get more sources of longer-term supply, just as sources of demand will wane,” said Ward McCarthy, chief financial economist at Jefferies.

| 2018 Q4 | 2019 Q1 | 2019 Q2 | 2019 Q3 | |||||||||

| 2y | 10y | Spd | 2y | 10y | Spd | 2y | 10y | Spd | 2y | 10y | Spd | |

| BofA | 2.9 | 3.25 | 35 | 3 | 3.3 | 30 | 3.1 | 3.35 | 25 | 3.2 | 3.35 | 15 |

| Scotiabank | 3 | 3.25 | 25 | 3 | 3.15 | 15 | 3.1 | 3.2 | 10 | 3.3 | 3.4 | 10 |

| Barclays | 3 | 3 | 0 | 3.1 | 3 | -10 | 3.2 | 3 | -20 | 3.25 | 3 | -25 |

| BNP | 2.95 | 3.1 | 15 | 3.05 | 3.15 | 10 | 3.1 | 3.2 | 10 | 2.75 | 3.1 | 35 |

| Cantor | 2.95 | 3.125 | 17.5 | 3 | 3.125 | 12.5 | 3.1 | 3.25 | 15 | 3.2 | 3.25 | 5 |

| Citigroup | 2.75 | 2.8 | 5 | 2.9 | 2.85 | -5 | 2.9 | 2.85 | -5 | |||

| Daiwa | 3.15 | 3.35 | 20 | 3.4 | 3.5 | 10 | 3.6 | 3.65 | 5 | 3.65 | 3.65 | 0 |

| Deutsche | 3 | 3.5 | 50 | 3.05 | 3.6 | 55 | 3.1 | 3.6 | 50 | 3.15 | 3.65 | 50 |

| Goldman | 3 | 3.1 | 10 | 3.2 | 3.2 | 0 | 3.35 | 3.3 | -5 | 3.45 | 3.3 | -15 |

| HSBC | 2.6 | 2.8 | 20 | 2.7 | 2.8 | 10 | 2.8 | 2.8 | 0 | 2.5 | 2.65 | 15 |

| Jefferies* | 2.95 | 3.25 | 30 | 3.15 | 3.5 | 35 | 3.35 | 3.6 | 25 | 3.5 | 4 | 50 |

| JPMorgan | 3.05 | 3.2 | 15 | 3.2 | 3.3 | 10 | 3.35 | 3.4 | 5 | 3.55 | 3.5 | -5 |

| Mizuho | 2.75 | 2.75 | 0 | 2.9 | 2.9 | 0 | 3 | 3.1 | 10 | 3.1 | 3.3 | 20 |

| Morgan Stanley | 2.75 | 2.75 | 0 | 2.8 | 2.5 | -30 | ||||||

| NatWest | 2.9 | 3.25 | 35 | 3.1 | 3.3 | 20 | 3.25 | 3.35 | 10 | 3.2 | 3.3 | 10 |

| Nomura | 3 | 3.25 | 25 | 3.125 | 3.375 | 25 | 3.125 | 3.25 | 12.5 | 3.125 | 3.125 | 0 |

| RBC | 2.9 | 3.3 | 40 | 3 | 3.45 | 45 | 3.25 | 3.6 | 35 | 3.4 | 3.7 | 30 |

| SocGen | 2.7 | 3 | 30 | 3 | 3.25 | 25 | 2.9 | 3 | 10 | 2.9 | ||

| TD | 2.9 | 3.1 | 20 | 3 | 3.15 | 15 | 3.1 | 3.2 | 10 | 3.2 | 3.25 | 5 |

| Wells Fargo | 3 | 3.35 | 35 | 3.1 | 3.45 | 35 | 3.15 | 3.55 | 40 | 3.25 | 3.65 | 40 |

| Average | 21.4 | 17.8 | 10.6 | 14.1 |

NOTE: BMO, Credit Suisse and UBS didn’t provide quarterly yield forecasts. *Jefferies figures represent averages for the quarter

To contact the reporters on this story: Sydney Maki in New York at smaki8@bloomberg.net;Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum, Vivien Lou Chen

©2018 Bloomberg L.P.