Wall Street Pros From Dan Fuss to Bob Michele on Bubble Trouble

Wall Street Pros From Dan Fuss to Bob Michele on Bubble Trouble

Everything from European bonds and U.S. Treasuries to high-yield credit and tech stocks is trading near the highest valuations in decades -- even as the inflation bogeyman risks breaking out at long last.

Market participants from Goldman Sachs Group Inc. to BlackRock Inc. are divided on whether all this constitutes an unsustainable frenzy. To Dan Fuss, the legendary 87-year-old vice chairman at Loomis Sayles & Co. LP, it certainly looks that way thanks to unprecedented liquidity that is now set to tighten on good economic news.

Meanwhile, Kathy Jones of Charles Schwab & Co. is telling clients to beware the “nuttiness” in junk debt. And JPMorgan Asset Management’s Bob Michele is calling on Fed officials to discuss tapering asset purchases soon enough, before market bubbles form.

Others are more sanguine -- betting that the economic reopening and the re-leveraging cycle will pave the way for more cross-asset gains.

Interviews have been edited for clarity.

Dan Fuss, vice chairman, Loomis Sayles

“We are in ‘bubble’ territory. It is primarily a liquidity bubble, combined with the resulting valuation distortion. Stocks with high P/Es, marginal credit bonds, and pooled vehicles are the most vulnerable. In the 1960s and 1970s, I was lucky enough to spot the small stock valuation bubble and the growth stock bubble. The similarity between then and now was valuation. This one is a liquidity bubble that is unique in my experience.

The markets are awash in liquidity caused by the central bank supporting the Treasury’s needs in fighting the Covid war. It is slightly analogous to the formal accord of the late 1930s to mid 1950s between the Fed and the Treasury. It is different in that it caused layers of increased liquidity as various market participants can borrow shorter term money cheaply.

When prices decline somewhat, there can be, as there was last March, a magnified drop in the liquidity, causing more sales. This can destabilize the broader market.”

Kathy Jones, chief fixed-income strategist, Charles Schwab

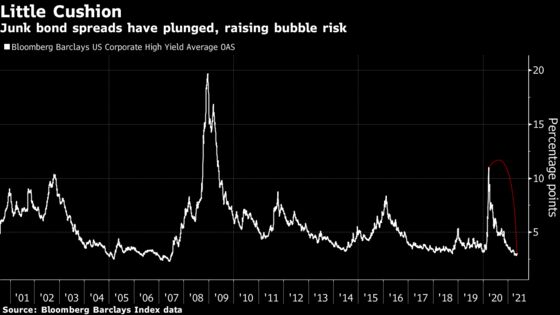

“We are warning people about not overdoing it. We are saying it’s OK to hold high yield but to try not to hold a concentrated position at the low end and realize this can change pretty fast. This is when diversification really helps you, when things are a little nutty like this, and you don’t know when the nuttiness will end.

When I look at CCC’s rallying so hard -- even if the default rates are at the low end of historical average -- your chances of making money over the long run aren’t great. You’d be lucky to break even.”

Bob Michele, CIO, JPMorgan Asset Management

“My biggest concern is that the Fed waits too long to start the normalization process. Their view is that there is a reopening surge that creates a short term spike in inflation, but it will be transitory. If they’re wrong, that’s when things could become painful.

The economy and markets would binge on the prolonged period of cheap money and the risk of bubbles would be far greater. They would be forced to take away the proverbial ‘punch bowl’ by tightening monetary policy more aggressively than the markets expect.

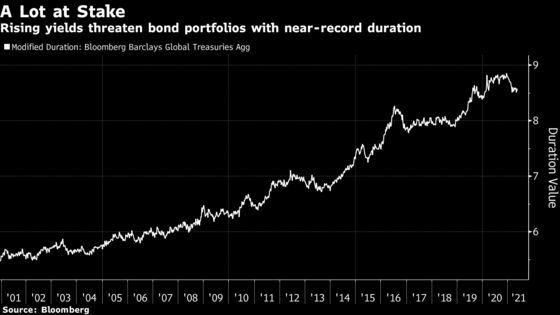

I don’t want to be involved in that experiment of owning negative real yields and hoping the Fed can manage an unusually complex normalization process by letting the economy and inflation run hot for a period of time! Consequently, we’re using rallies to sell duration.”

“I’m inviting the Fed to start the normalization process now. They should start the conversation on tapering QE no later than the August Jackson Hole meetings. I never thought in my career I would be asking the Fed to begin withdrawing liquidity from the system. But I’m asking because growth and inflationary pressures are just too high.

They should start actual tapering no later than January 2022 and then start raising rates no later than mid 2023. There is no reason for them to be running the same level of accommodation as a year ago.”

Elga Bartsch, head of macro research, BlackRock Inc.

“Markets are not in bubble territory, but they are in unusual terrain given that we are in an economic restart, not a regular business-cycle recovery. For the Fed to move faster than indicated by market pricing, it would essentially need to abandon its new policy framework, which it adopted only last August.

We deem this unlikely and see a later lift-off for rates than the market. One pre-condition for the emergence of bubbles is the build-up of financial imbalances. Prior to Covid-19 there was little indication of such imbalances. Since then private sector balance sheets have become stronger, not weaker.”

Read more: Fund That Made 929% on Equities Crash Targets Big Short in Bonds

Vineer Bhansali, founder, LongTail Alpha

“Bonds are in a massive bubble that we’ve never seen the likes of and inflation, which is the biggest risk to bonds, is coming back. My biggest worry right now is if there’s suddenly a sharp rise in yields, especially in Europe and Japan.

I’m massively short the bond market. A big rise in rates can upend everything. If the thing you are counting on to protect you is not protecting you and it’s hurting you, you are going to have to start liquidating -- your Bitcoin, your equities and more. There will be collateral damage.

Everybody is counting on the Fed to keep stepping in and buying bonds. At some point the Tsunami may just wash them and they have to say we just can’t buy any more. That to me is the biggest danger.”

Peter Oppenheimer, chief global equity strategist, Goldman Sachs

“There are pockets of over optimism and excessive valuations in equities. But the key thing is whether this is broad enough in its manifestation to become systemically risky. I would say that there isn’t really a strong evidence of that yet. We may have high multiples, but they are not that high when you consider where interest rates are.

We don’t have huge leverage in the private sector. We found that private sector leverage is a very common driver of financial bubbles. Households have very strong savings and they don’t have high levels of leverage. That’s true for banks as well. We expect global growth to accelerate strongly and in a synchronized way. We are overweight stocks and commodities and underweight bonds.”

©2021 Bloomberg L.P.