Wall Street Calls Out JPMorgan’s ‘Very Un-JPMorgan-Like’ Earnings

Wall Street Calls Out JPMorgan’s ‘Very Un-JPMorgan-Like’ Earnings

(Bloomberg) -- JPMorgan Chase & Co.’s fourth-quarter earnings report initially stung, with a plunge in fixed-income trading revenue that Wolfe Research labeled “very un-JPMorgan-like.” Wells Fargo & Co. results disappointed, too, hurt by lower fees and a drop in mortgages.

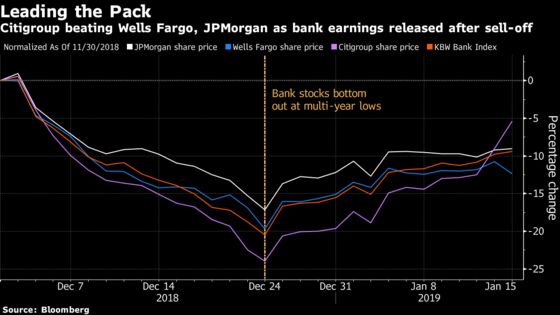

That weighed on their shares Tuesday morning, although JPMorgan shares started to rally alongside the broader market by mid-day. Bank of America Corp., due to report later this week, also rose, while Goldman Sachs Group Inc. underperformed. Citigroup Inc. was a standout, extending a five-day gain to rise as much as 4.9 percent. The bank on Monday signaled better days were ahead -- and it’s been underperforming peers in recent weeks.

Moves in Citigroup’s stock compared with JPMorgan’s suggest investors may be “focusing on costs in an uncertain revenue environment,” said Bloomberg Intelligence analyst Alison Williams. Wells Fargo’s stock took a hit with its commentary about planning to operate under the Federal Reserve’s asset cap through the end of 2019 instead of the middle of the year, she said.

Here’s what some analysts are saying:

Wolfe Research, Steven Chubak

Chubak flagged JPMorgn’s broad-based core miss. The bank “has a strong track record of delivering strong revenue/earnings beats and these results appear rather unremarkable,” he wrote in a note. “The lone bright spot was strong NII/core loan growth, but optimism here will likely be tempered by muted NII guidance” for the first quarter of “flat” versus the prior quarter. “We expect shares to underperform, with the rest of the group likely to trade in sympathy.”

Barclays, Jason Goldberg

JPMorgan’s below-expectation EPS was the first miss in 16 quarters, Goldberg wrote. He underscored a higher-than-expected “loan loss provision (added to card and wholesale reserves) and managed tax rate, as well as lower than anticipated fee income (driven by FICC).” Results were also weighed down by “charitable contributions, private equity markdowns, securities losses and a MSR hedge loss.”

Morgan Stanley, Betsy Graseck

Graseck’s read-across from JPMorgan’s results is bad for investment banks, credit cards and large regional banks. The trading miss has negative implications for Bank of America and for Goldman in particular, given Goldman’s “investor client skew and less corporate client skew.” Card spending missed Morgan Stanley’s estimate, and Graseck called no change in JPMorgan commercial banking loan growth -- versus her estimate of a 2 percent gain -- “negative for super-regional bank loan growth.”

KBW, Bose George

JPMorgan’s mortgage banking trends missed expectations, George wrote in a note, citing volumes tumbling 24 percent quarter-over-quarter versus average expectations of a 14 percent decline, along with a gain-on-sale margin drop of 64 basis points (turning to a loss of 16 basis points). At the same time, Wells Fargo’s mortgage banking results were “largely in line” with expectations.

KBW, Sanjay Sakhrani

For both JPMorgan and Wells Fargo, total card purchase volume growth (including credit and debit) decelerated compared with the prior quarter, which was “in-line to slightly weaker” than KBW’s expectations for Visa and a bit worse than the quarter-to-date trends for Visa. Results for both were also similar to Citigroup’s; on Monday, Sakhrani said Citi’s card volume trends were “slightly weaker” than expectations for Mastercard.

Evercore ISI, John Pancari

At Wells Fargo, Pancari said, weaker fees and expenses were masking better balance sheet trends and called the quarter “mixed.”

Nomura Instinet, Bill Carcache

Wells Fargo’s results “were noisy and included several significant items,” while “core operating trends held up reasonably well in light of last quarter’s volatility.” Results were characterized overall by “a softer-than-expected top line, offset by a combination of better expenses, credit, and taxes.”

Read more: Citigroup Rises as Some Analysts Focus on Earnings Bright Spots

To contact the reporter on this story: Felice Maranz in New York at fmaranz@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Richard Richtmyer

©2019 Bloomberg L.P.