The Retail Apocalypse Now Threatens Drugstores, Too

The Retail Apocalypse Now Threatens Drugstores, Too

(Bloomberg Opinion) -- Are we headed for a drugstore apocalypse?

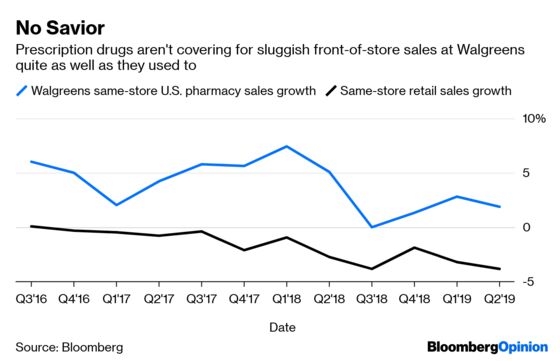

CVS Health Inc., America’s biggest pharmacy chain, rang a warning bell in February with a disappointing 2019 forecast that reflected pressure on its prescription-drug business. A month later, Rite Aid Corp., another big pharmacy operator, jettisoned executives amid continuing struggles as its stock price traded below $1. Then on Tuesday, No. 2 chain Walgreens Boots Alliance Inc. announced dismal second-quarter results and slashed its full-year guidance. Its shares tumbled more than 12 percent as both retail and pharmacy performance fell substantially short of expectations.

Trouble on the convenience-store side of the business isn’t news. But pharmacy sales have helped cover up those issues for years; the fact that these chains are now making less money on prescriptions is a matter of real concern. A once consistently profitable differentiator that helped insulate drugstores from the headwinds facing the rest of the retail world is no longer as reliable.

Pressure on the pharmacy business is coming from all sides. Increased political scrutiny and outcry over the high cost of medications means fewer drugmakers are raising prices on medications, and the Food and Drug Administration has sped up the generic approval process, which has helped bring down the cost of older treatments. The Trump administration has proposed a series of policies that could bring down prices even more.

The drugstore giants aren’t just competing with each other and smaller chains anymore. More internet-savvy startups such as Capsule and Blink Health have entered the market and will only continue to snatch customers out of stores and add to reimbursement pressure. Last year, Amazon.com Inc. bought PillPack, one of those upstarts, and could be a fearsome pharmacy competitor in time.

It all adds up to a prescription drug and pharmacy business that looks a bit more like a regular retail market instead of a comfortable niche where prices only go up and two big megachains, CVS and Walgreens, dominate. That’s pretty bad news for these companies; milk, makeup, and Mucinex won’t provide much growth or support more than 17,000 stores apiece.

CVS has responded to these growing pressures by spending $68 billion on health insurer Aetna Inc. and committing to devoting big chunks of its stores to health-care services. It will be years before investors know whether that was a good gamble, but at least it’s trying something big. Walgreens looks more exposed. It has a diversifying European business, but U.S. pharmacies make up three-quarters of its sales. Its Tuesday earnings call emphasized internally driven digitization, changes to its stores, and “transformational cost management” as strategic priorities.

Those are all fine goals, but may not add up to an adequate response to big structural changes to the firm’s most important business.

Big retail drugstores aren’t going to vanish any time soon. But we may be heading towards a future where there are fewer of them, they look a lot different, and potentially aren’t as profitable.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Max Nisen is a Bloomberg Opinion columnist covering biotech, pharma and health care. He previously wrote about management and corporate strategy for Quartz and Business Insider.

©2019 Bloomberg L.P.