Virus Surge Steepens Malaysian Yield Curve Before Rate Decision

Virus Surge Steepens Malaysian Yield Curve Before Rate Decision

(Bloomberg) -- Malaysia’s yield curve has reached the steepest in almost four years amid a surge in virus cases. Two local events next week -- a policy meeting and budget announcement -- may hasten the spread-widening trend.

Another potential risk leading to further spread widening is from the U.S. presidential election, where an unexpected outcome could sap demand for the Asian nation’s longer-maturity debt.

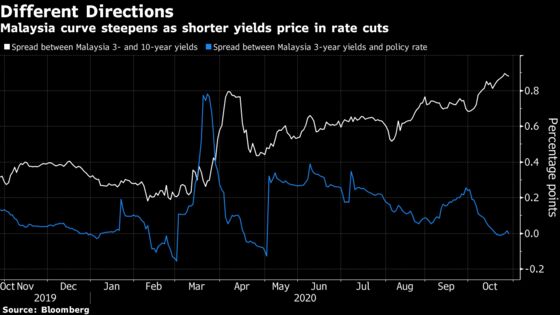

Malaysia’s longer-dated yields have been climbing since August on concern the need for additional government spending to counter the pandemic will require greater issuance of longer-dated debt. At the same time, shorter-term yields are being pushed lower by expectations the central bank will cut interest rates again to support economic growth.

The spread between three- and 10-year yields widened to 88 basis points this week, the most since January 2017. The gap had been as narrow as 17 basis points in February before the global outbreak of the virus lead to a sell-off in risk assets.

The latest spike up in the spread came after new virus cases jumped to a record of more than 1,000 a day, leading the government to tighten its partial lockdown -- known as a conditional movement control order -- on Oct. 26. This entailed extending the partial lockdown by an additional two weeks to Nov. 9 in Kuala Lumpur, Selangor and Putrajaya, following a similar decision in Sabah a few days before.

These areas contribute close to 50% of the nation’s gross domestic product, and every two weeks of the control order are projected to shave 0.2 to 0.3 percentage points from baseline annual economic growth, according to Citigroup Global Markets. Slower growth means additional need for stimulus and a greater prospect of lower interest rates.

Key Local Events

The central bank will announce its next policy decision on Tuesday. A majority of economists surveyed by Bloomberg expect the central bank to stay on hold, possibly to preserve “room for possible action in 2021,” according to Bloomberg Economics. Nonetheless, the latest virus tally may nudge policy makers to signal the prospect for further easing.

This will be followed three days later by the release of the government’s 2021 budget, which will include its latest target for next year’s budget deficit. The current projection for this year is 5.8% to 6% of gross domestic product, already the highest in more than a decade.

“We expect the government’s fiscal deficit this year to hit 6% of GDP, and any overshooting will mainly stem from GDP coming in lower than expected,” said Wellian Wiranto, an economist at Oversea-Chinese Banking Corp. in Singapore. “We are forecasting a fiscal deficit of 5.5% of GDP next year,” which would be a balance between a gesture toward fiscal consolidation, and the need to offer fiscal support to help the still-fragile economic recovery, he said.

The budget may also reignite political tensions. Although Prime Minister Muhyiddin Yassin’s position has become more assured in recent days after the largest partner in his ruling coalition voiced support for him, he faces another key test when he presents the budget in parliament. Failing to pass the resolution may count as losing a no-confidence vote, which could unleash another outbreak of political uncertainty and push long-term yields even higher.

A previous Southeast Asia rates column in July carried the headline: “Shorter is better is the mantra for Malaysia bonds.” If anything, the prospect of further curve steepening is even stronger now than it was then.

What to Watch

- Indonesia will publish inflation data on Monday and is targeting to sell 20 trillion rupiah ($1.4 billion) of conventional bonds on Tuesday. Third-quarter GDP figures will be released Thursday

- The Philippines will report export numbers Wednesday and inflation data the following day

- Thailand will publish inflation figures Thursday after seven consecutive months of deflation

Note: Marcus Wong is an EM macro strategist who writes for Bloomberg. The observations he makes are his own and not intended as investment advice.

(An earlier version of this story was corrected to say next week in first deck headline.)

©2020 Bloomberg L.P.