Guess Who’s Defending Active Bond Funds? Vanguard.

Guess Who’s Defending Active Bond Funds? Vanguard.

(Bloomberg Opinion) -- Quick — what’s the first word you associate with Vanguard Group Inc., the $5.1 trillion investing giant? Perhaps it’s “indexing” or “passive,” referring to some of the asset manager’s largest fund offerings, such as its $577 billion Vanguard Total Stock Market Index Fund or the $154 billion Vanguard Total Bond Market II Index Fund.

John Hollyer, global head of fixed income at Vanguard, would much prefer you use the term “low cost.”

The distinction seems like semantics at first glance. After all, many tributes last month to Jack Bogle, the founder of Vanguard who died at age 89, interchangeably referenced the rise of index mutual funds and the decline in investor fees, sometimes in the same breath. Yet, in what may be unknown to some, Vanguard has $1.3 trillion in actively managed funds, including $413 billion in active bond funds. And Hollyer only expects that fixed-income figure to grow: The firm is building out a high-yield team to go along with its current roster, which includes specialists in U.S. investment-grade corporate debt and emerging markets, part of its push to extend its reach beyond the U.S.

“Vanguard isn’t index versus active — it’s low cost versus high cost,” Hollyer said in an interview. “We feel strongly that low-cost active fixed-income management can be a valuable part of clients’ portfolios,” he said, adding that “there’s no debate: If it’s high cost, it’s usually not a winning formula.”

This defense of active management comes at a pivotal time for the bond market. For one, legendary investor Bill Gross announced his retirement this week from Janus Henderson Group Plc after a stretch of bad bets and client withdrawals, raising fresh doubts about whether star managers can deliver consistently superior returns. On top of that, large money managers like Fidelity Investments and Invesco Ltd. have recently introduced exchange-traded funds that use the quantitative finance concept of “factor investing” to put decisions in the hands of machines. Broadly, Moody’s Investors Service has said it expects passive strategies to overtake active ones no later than 2024.

At this point, the trend toward passive investing is clear: If anything, it should overtake active even sooner than Moody’s anticipates. Still, when it comes to the bond markets, Hollyer’s stance holds up.

For one, trading single bonds can be prohibitively expensive, particularly in less liquid pockets like the U.S. municipal market, Hollyer said. “For the average retail investor, just getting good institutional management at a low cost can save them on trading costs, even before the manager adds value,” he said. The retail class of Vanguard’s two biggest muni funds each have no front- or back-load fees (meaning it doesn’t cost extra to buy or sell fund shares) and charge a relatively meager 0.16 percent management fee. The next-largest competitor, the Tax-Exempt Bond Fund of America, has a 0.21 percent management fee and costs associated with buying and selling.

The other reason active management probably won’t disappear from fixed income is because indexes are inherently biased toward the most-indebted borrowers. U.S. Treasuries are becoming a larger share of the Bloomberg Barclays U.S. Aggregate Bond Index, for example, because the federal government is running big budget deficits. More worrisome is the proliferation of company debt rated in the lowest tier of investment grade because corporate behemoths ramped up borrowing at low interest rates and got downgraded as a result. While the demise of those companies may be overblown, investors may not want to increase their exposure to potential fallen angels by purchasing passive bond funds.

I don’t get the sense that the same level of concentration and passive focus is inevitable for bonds. The better question might be what active management style is most desirable. My Bloomberg Opinion colleague Nir Kaissar made an interesting contrarian argument that Gross had the right idea with his unconstrained bond fund:

“To the extent that investors need a bond manager, it’s to make the kind of unconstrained calls that Gross made at Janus Henderson, knowing full well that those calls could be a bust just as easily as a boon. You can’t get that from an index.”

I’m not quite sold on that — boom-bust trades sound more like something a hedge fund would do than a bond manager. Alternatively, investors could turn to more subtle active strategies that (to borrow a tired baseball metaphor) are looking to hit singles rather than home runs. This is effectively what quants want to bring to fixed-income ETFs, though it’s too soon to say whether their strategy will pan out.

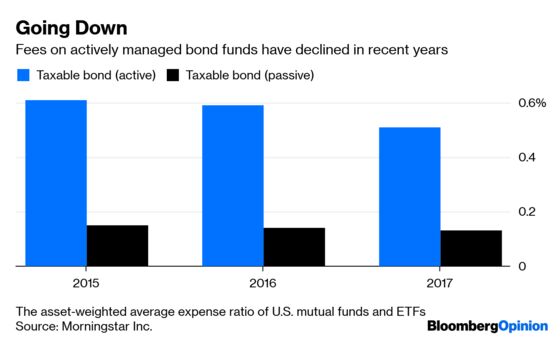

This brings us back to Hollyer and his preference for thinking of funds in terms of cost. It’s not hard to envision active bond managers still roaming the markets in a decade or two — but only if their fees continue to come down. The indexing revolution and the rise of ETF trading have forever changed what people have come to expect as far as the ease and affordability of investing. As of 2017, Vanguard’s actively managed bond funds had an average expense ratio of 0.11 percent. That’s lower than the average industry fee on passive taxable and tax-exempt funds, according to Morningstar Inc. data.

The “Vanguard Effect” is estimated to have saved investors hundreds of billions of dollars. It’s worth remembering who lost money from that trend, too. But for bond managers, there’s no going back now.

The Vanguard Intermediate-Term Tax-Exempt Fund and Vanguard Limited-Term Tax-Exempt Fund. They are technically actively managed, though they track their respective benchmarks very closely.

According to the most recent fund data compiled by Bloomberg.

Disclaimer: The Bloomberg Barclays suite of bond indexes are widely used as benchmarks across mutual funds.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.