ADVERTISEMENT

USD Rates Volatility Is Waiting For the Business Cycle to Turn

USD Rates Volatility Is Waiting For the Business Cycle to Turn

20 Dec 2018, 09:58 PM IST

(Bloomberg) -- A higher USD rates volatility regime may not happen before the yield curve re-steepens, which might not be seen until at least the second half of next year.

In the meantime, systematic short-volatility strategies may continue to harvest value from vol spikes, although returns may be lower than in recent years.

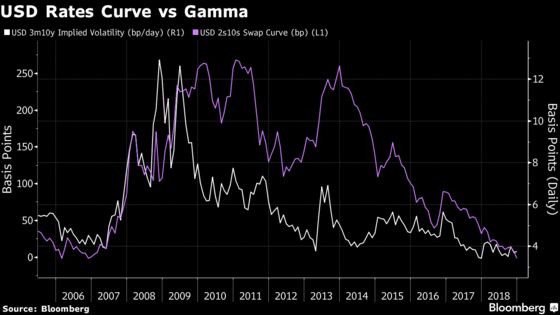

- The relationship between the shape of the yield curve and implied volatility is intuitive in the sense that periods of great uncertainty, when the curve bull-steepens, exhibit higher implieds than times when curves are flat and convexity cost is small

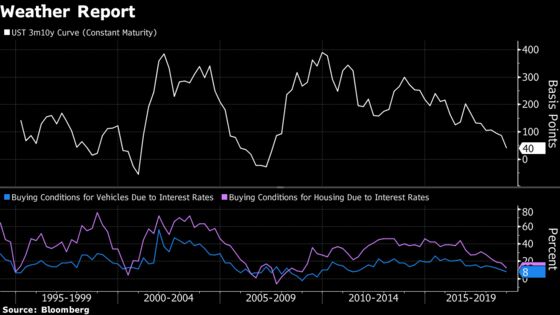

- The flattening of the 3m/10y Treasury yield curve, now around 40bps, may continue and invert next year, with the Fed projecting a baseline of two hikes next year and another in 2020; an inverted curve would suggest increased recession risk in 2020, given it has been historically a powerful indicator

- As the market shapes expectations of the neutral rate, the central bank is shifting from autopilot to a more data-dependent approach, with the Fed hinting that rate increases may be nearing an end; early warning metrics are showing higher rates are hurting, such as underlying weakness in housing and autos (the most rate-sensitive sectors) as consumer sentiment sours

- Harvesting value from short rates vol on the 1m10y point has remained an attractive yield enhancement strategy, which is being monetized and compounded by systematic short-gamma programs, given the efficiency of central bank predictability, stable economic data and volatility a function of the business cycle

- Delivered vol needs to see higher inflation, greater macro dispersion and changes in central bank communication with Powell stressing data dependency, while relatively benign inflation gives room to be patient in setting policy

- The interplay between the increase in real rates and sell-off in equities will continue as uncertainty around the neutral rate plays out amid the main driver of quantitative tightening

- Spread vol is the most leveraged play on a move higher in the rate-vol regime and curve caps that benefit from a re-steepening may come into vogue as fears of a recession increase

- NOTE: Tanvir Sandhu is a global interest-rate and derivatives strategist who writes for Bloomberg. The observations he makes are his own and are not intended as investment advice

©2018 Bloomberg L.P.