ADVERTISEMENT

U.S. Rates Volatility on Policy Uncertainty Roller-Coaster Ride

U.S. Rates Volatility on Policy Uncertainty Roller-Coaster Ride

07 Aug 2019, 11:21 PM IST

(Bloomberg) -- A surge in U.S. rates volatility faces the uncertain life expectancy of an ageing business cycle.

The market is tilting toward a more conventional easing cycle from the Fed rather than a scenario of just insurance cuts. That means that volatility can move higher, especially if recessionary impulses force policy makers to cut to zero. If, on the other hand, the Fed and the economy convince the market into pricing an insurance-easing scenario, then short-term rates volatility will decline.

- Harvesting value from short rates volatility on the 1m10y point has been an attractive yield-enhancement strategy in recent years

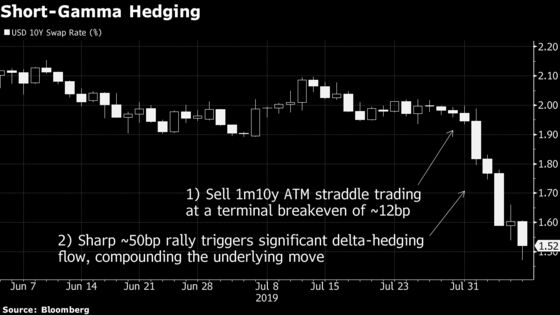

- Receiving flows related to delta hedging of these positions during outsized declines in yields compounds the underlying moves

- USD rates gamma is spiking higher following heightened U.S.-China trade tensions, after cheapening since mid-June as yields stabilized owing to positive U.S. data surprises

- Selling vol via 1m10y ATM straddles at the end of July would have had a terminal breakeven of ~12bp

- The subsequent rally of ~50bp in 10y swap rates would therefore have triggered significant delta-hedging receiving flows

- The gamma profile on these shorts has moved close to zero given the large market move away from the strike, which leaves no need to receive rates on any further rally in this case

- If it turns out that this is a mid-cycle adjustment in policy rates, then the upper left of the swaption grid will lead the move lower in implieds across the surface

- However, a U.S.-China trade deal remains elusive and breaking confidence in global supply chains can be a trigger that brings on a recession rather a 1990s-style mid-cycle correction

- Fed’s reaction function, although unclear, has created a link between trade uncertainty and further easing; Trump will know that the U.S. administration can effectively push the Fed to cut further by escalating trade tensions

- Policy uncertainty and increased macro vol should help underpin vols from revisiting record lows, while previous cycle highs seems unlikely given the proximity to the zero lower bound which should leave vols structurally cheap

- Curve vol straddles may be preferable over outright long vol exposure for those inclined to protect themselves against recession risks

- These will perform with a potential increase in delivered curve vol as the rates curve goes from bull flattening to bull steepening on aggressive Fed cuts

- Confusion about the Fed’s new reaction function could also set up scenarios where the future messaging doesn’t meet dovish market expectations, which would help drive 2s10s flatter and see delivered correlation of the curve fall

- With money markets are already pricing over 100bps of cuts by December 2020, the risk-reward points to options that limit the risk to the premium paid -- such as mid-curve call spreads -- to position for any deeper Fed cut pricing being bought forward

- The Fed may also go uber-dovish in an attempt to lift the inflation risk premium from historic lows given how exposed it is to conduct QE in the next recession with policy rates so close to the zero lower bound

| Read Year-Ahead Outlook Here: USD Rates Volatility Is Waiting for the Business Cycle to Turn |

- NOTE: Tanvir Sandhu is a global fixed income and derivatives strategist who writes for Bloomberg. The observations he makes are his own and are not intended as investment advice

To contact the reporter on this story: Tanvir Sandhu in London at tsandhu17@bloomberg.net

To contact the editor responsible for this story: Ven Ram at vram1@bloomberg.net

©2019 Bloomberg L.P.