U.S. Money-Market Investors Face Multiple Grim Trends in 2021

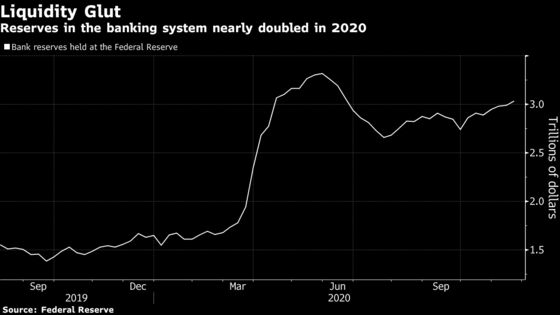

Supply of investable assets will shrink by about $300 billion while the amount of cash chasing them has doubled to $3 trillion.

(Bloomberg) -- Investors in the U.S. money market are facing a grim year ahead.

That’s the vision laid out by JPMorgan Chase & Co. strategists, who predict that the supply of investable assets will shrink by about $300 billion while the amount of cash chasing them has nearly doubled to $3 trillion.

A key factor on the supply side is that the quantity of Treasury bills is poised to shrink as the U.S. government replaces with longer-term debt much of the short-term borrowing it undertook in 2020 to pay for fiscal stimulus. Meanwhile demand for securities is rising, with bank reserves having increased by $1.4 trillion since the start of the year as the Federal Reserve ramped up asset purchases in response to the March liquidity crisis. On top of that, the central bank plans to keep its policy rate close to zero at least through 2023.

These factors and others “should make 2021 a challenging year to stay invested, and a challenging time to earn yield in the money markets,” JPMorgan’s Alex Roever and colleagues wrote in note published earlier this week. “Liquidity-focused investors inhabiting the cash money markets are in a fix.”

Benchmark reform complicates matters further, the JPMorgan team said. Global regulators are keen for the London interbank offered rate to leave the stage by the end of next year. In the dollar market, the Secured Overnight Financing Rate, or SOFR, has been selected to replace it.

Yet “there is still plenty of uncertainty around benchmark reform as it relates to existing Libor exposures in the cash markets,” Roever said. Markets aren’t pricing in Libor cessation as a substantial risk, possibly because they’re “more focused on staying invested given the imbalance between supply and demand.”

Euribor

A European Central Bank-backed committee exploring options for a transition away from Euribor in the event that it ceases to exist, should not be seen as a threat to the benchmark, according to Andrea Appeddu, a strategist at Citigroup Inc.

The outcome of the committee’s first consultation should be of limited consequence to most interest-rate derivative traders, since the market that references the ECB’s short-term rate is small and focuses mostly on contracts maturing in under one year, Appeddu wrote in a note to clients.

What’s more, a second consultation seeking views about so-called trigger events that could help set off the transition process, “should help reduce ambiguity about pre-cessation events ahead of the working group meeting in February,” he added.

©2020 Bloomberg L.P.