U.S. Junk Bond Rally Will Be More Muted in 2020 After 13.5% Year

U.S. Junk Bond Rally Will Be More Muted in 2020 After 13.5% Year

(Bloomberg) -- U.S. junk bonds won’t provide the stellar returns that investors enjoyed this year, but they’re still on track to do reasonably well in 2020 as long as defaults remain muted and the economy stays steady.

Wall Street credit analysts are forecasting gains of between 1% and 7.5%, which would be a sharp decline from the more than 13.5% total returns so far in 2019, according to Bloomberg Barclays index data.

Those expectations are based on views that economic growth will slow rather than slide into a full-blown recession, that U.S. credit in general still offers decent relative value and that the Federal Reserve will remain on hold for at least the next few months.

Read more: Returns, Supply and Spread Forecasts for 2020

“The conclusion we’ve come to is that the music is still playing, the cycle is still rolling,” said Bank of America Corp. strategist Oleg Melentyev. “Probably the music is not as loud as it was a couple of years ago, but nevertheless you can still hear it.”

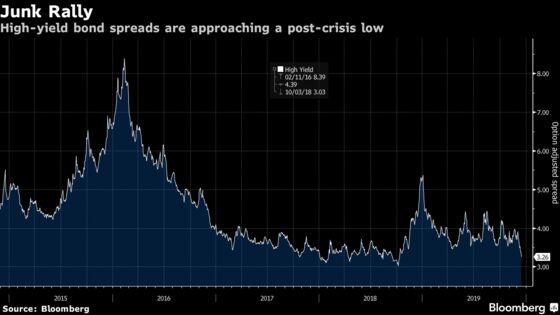

Still, it’s difficult to get too excited as valuations have become stretched after a rally that has driven yields to a five-year low of 5.15% and risk premiums to within 23 basis points of post-crisis tights.

Analysts mostly expect spreads to widen by at least 1 percentage point by the end of next year.

Barclays strategists favor single B bonds over BBs in an environment of low single-digit returns for the asset class overall. They’re concerned the potential upside for BBs is limited after yields for the highest-rated junk bonds sank to an all-time low of just 3.51%.

Read more: Junk rally crushes spread between BBB, BB to record low

Triple Cs, the lowest tier of junk debt that has lagged the broader rally this year, are likely to remain under pressure.

Supply is running at more than $264 billion this year, a 60% increase in new issue volumes in 2018. Most analysts expect similar to slightly lower figures next year with refinancings likely to continue to make up the bulk of that unless there’s a pick-up in acquisitions.

Among the deals that could surface in the first quarter are multibillion debt sales for the take-private of Zayo Group Holdings Inc. and the buyout of Nestle SA’s U.S. ice cream business.

To contact the reporter on this story: Gowri Gurumurthy in New York at gurug@bloomberg.net

To contact the editors responsible for this story: Natalie Harrison at nharrison73@bloomberg.net, Claire Boston

©2019 Bloomberg L.P.