Full Employment Looks as If It’s Finally Here

Full Employment Looks as If It’s Finally Here

(Bloomberg Opinion) -- How long will it be until the U.S. economy runs out of people to put back to work? That’s a question that’s on the minds of both the Federal Reserve and private businesses. If the U.S. hits full employment, it means that keeping interest rates low might cause inflation. It also means that businesses will have to raise wages in order to poach workers from each other.

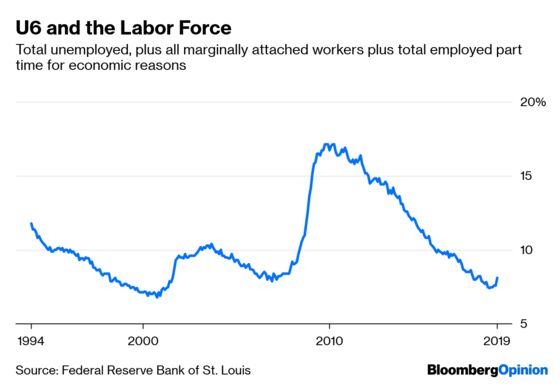

The U.S. labor market looks strong. In January the U.S. economy added 304,000 jobs, a larger-than-average number. Meanwhile, U6, the broadest measure of unemployment — which includes marginally attached workers and people who are working part-time but would like full-time jobs — is at prerecession levels (though it ticked up a bit in January):

And of those who are unemployed, the fraction out of a job for 27 weeks or longer has fallen steadily.

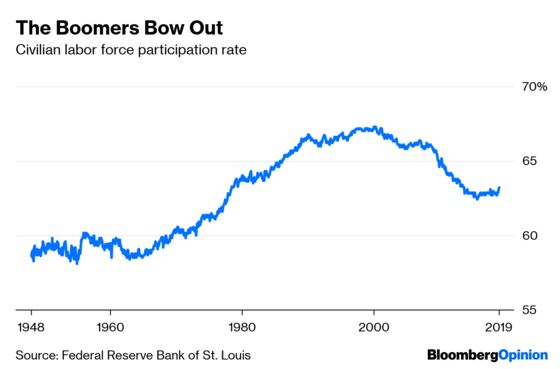

But some people claim that there are still lots of people out there waiting to come back to the workforce — an army of the shadow unemployed. As evidence for this, they point out that labor force participation — the percent of people either employed or seeking employment — hasn’t really recovered from the Great Recession:

One problem is that the whole concept of unemployment is fuzzy. If you don’t have a job, whether you’re unemployed or out of the labor force depends on whether you say you’re actively looking for work. But how active is active? Does it mean sending out one resume a month, or casually asking your friends every now and then if they know an employer that’s looking for workers? Government surveys don’t offer a hard-and-fast definition. And how many people who are out of the labor force would gladly take a job, but just don’t know how to look, or have been turned down so often that they’re exhausted?

If there are a lot of the latter group, it means that official numbers, even the broad U6 measure shown above, understate the true number of people who could be drawn into the ranks of the employed by better economic conditions.

Fortunately, the government keeps track of the people who aren’t in the labor force, and asks them why they’re not looking for work. The Current Population Survey, a joint project between the Census Bureau and the Bureau of Labor Statistics, is administered to 60,000 households every month. It asks people whether they’re retired, disabled or ill, in school, tending to family responsibilities or want a job but aren’t actively searching. A new website from the Federal Reserve Bank of Atlanta has made the data easily displayable with user-friendly charts.

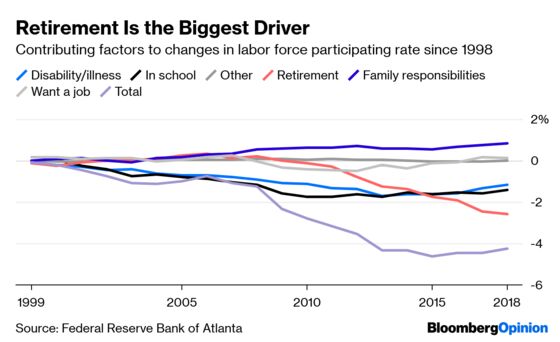

Here’s a picture of how various factors have contributed to the change in labor force participation since 1998:

The number of people who say they want a job but aren’t actively looking for work rose in the recession, but has fallen since, and is actually at a lower level than in 1998. If there’s still shadow unemployment in the U.S. economy, it probably won't be found here.

A much bigger factor is aging — retirement represents 61 percent of the total decline in labor force participation. About the time of the Great Recession, more people started retiring, and the trend hasn’t stopped. The mass retirement of the baby boom generation had been long anticipated, but it looks like the Great Recession sped it up. The oldest boomers were born in 1946, right after the end of World War II; these people were 62 when the financial crisis hit in 2008, just on the cusp of retirement. Seeing the economic devastation, many probably chose to simply retire early.

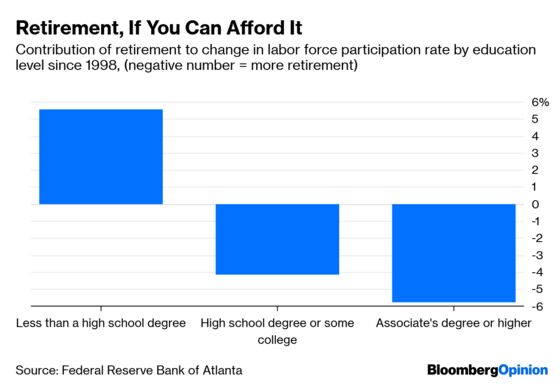

That hypothesis seems confirmed by the fact that it was educated Americans who started retiring en masse in 2009:

More educated people tend to earn higher incomes and save more, so they’re probably more likely to be able to take early retirement. In any case, retired people probably aren’t coming back into the workforce, especially as boomers continue to age.

The other big factors that are holding down labor force participation are disability/illness and school. If there is still shadow unemployment, it might be people hiding out in school until the labor market is better, or disabled people who could go to work but only with difficulty. The surge in disability applications during the recession and the fall in disability applications since the economy has recovered suggest that there are some of the latter. Meanwhile, college enrollment has fallen a bit as job prospects have improved. But both of these processes are probably limited — most disabled people probably can’t work, and the increasing importance of education in labor markets implies that quitting school is unlikely to be a popular option.

So shadow unemployment is probably drying up — months of strong job growth as in January are likely to become rarer. But this doesn’t mean the Fed should raise interest rates, or that the federal government should switch to austerity mode. Now that the U.S. economy is reaching full employment, increases in aggregate demand are more likely to translate into wage increases. Now is exactly the time for policy makers to keep their foot on the gas pedal, to help make up for the wage stagnation of recent decades.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2019 Bloomberg L.P.