U.K. Debt Chief Says Gilt Liquidity Behind Calm on Bond Rout

U.K. Debt Chief Hails Gilt Liquidity as Reason for Calm on Rout

(Bloomberg) -- The head of the U.K.’s Debt Management Office is hardly batting an eye over the meltdown in U.S. Treasuries that sent shockwaves across global bond markets last week for one key reason: liquidity at home.

Chief Executive Officer Robert Stheeman argues gilts are more insulated from the turmoil because of the market’s smaller size and network of primary dealers, or banks tasked with backstopping the market by buying and selling the securities even at times of unexpected volatility.

“I think that will certainly help us cope with whatever the market decides to throw at us this year,” he said in an interview on Wednesday. “We’re not the world’s reserve currency, but we do have, without any doubt -- and I say this with a very high degree of confidence because I see the numbers -- a level of liquidity in gilts which frankly stands out.”

Last week’s startling gyrations in U.S. Treasury yields sparked investor concern over liquidity in the world’s most important bond market, with reverberations felt across the globe through poorly-received government bond auctions and rising borrowing costs. And it poses a challenge to the DMO, which plans to sell more debt than expected next fiscal year.

In Perspective

Yet for all of the turmoil in recent weeks, U.K. 10-year yields, at 0.78% on Wednesday, remain around 15 basis points below their average going back to the Brexit referendum in June 2016.

The 30-year yield premium over five-year counterparts has fallen from the highest level since 2018, back toward the range set in the final four months of last year. Recent bond auctions show that demand for gilts remains robust, with bids for five- and 10-year notes almost triple the amount on offer and the highest since May and October, respectively.

“I’m not for a minute denying that it was a significant move over the last few weeks,” Stheeman said of the rise in gilt yields. “But one does need to look at the longer-term context of where yields are today on a historical basis.”

No Crisis

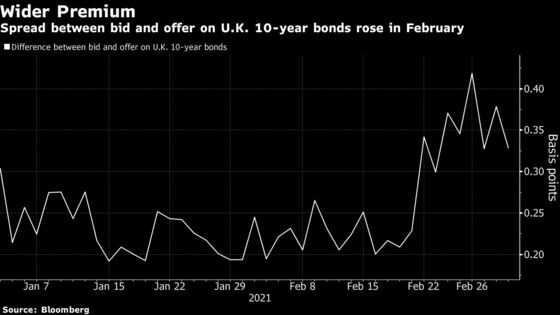

While several measures indicate more elevated funding stress and stretched liquidity in gilt markets, they are far from crisis-era levels.

Bid-ask spreads for 10-year gilts have risen in the past two weeks, but are down from the end-February peak. Meanwhile, the premium between three-month sterling Libor and the overnight rate rose to almost four basis points, the highest since July. That’s well below the high set last March at 61 basis points.

Heightening borrowing costs have caught the attention of U.K. politicians, with Chancellor Rishi Sunak warning that rates may rise. Yet while the national debt has risen past a record 2 trillion pounds ($2.8 trillion), historically low interest rates means the cost of servicing it is low.

Green Plans

The U.K. will likely take advantage of cheaper borrowing costs when it issues its first green debt, Stheeman said. Britain plans to sell green gilts twice in 2021 as it looks to build out a green bond curve, with a minimum issuance of 15 billion pounds in the coming financial year. Strategists at HSBC Holdings Plc see issuance beginning with a 10-year bond followed quickly by a longer maturity.

Britain will be a relatively late entrant to the green bond market, which surpassed a record $1 trillion in issuance last year. The Treasury and DMO are working on the technical aspects of the instruments, Stheeman said, and looking at questions such as whether the country will create its own green bond standards similar to those in development from the European Union.

There is some evidence that governments that borrow using green debt can save money, as demand drives up prices and pushes down yields. With the Treasury committed to reducing Britain’s debt levels, green gilts could provide slightly cheaper financing by tapping a rush of pent-up demand from specialist funds.

“Right now, the chances of us also doing something which could be extremely attractive from a cost effectiveness perspective are certainly rising,” Stheeman said.

©2021 Bloomberg L.P.