U.K. Bond Curve Seen Pivoting as Investors Brace for QE Shift

U.K. Bond Curve Seen Pivoting as Investors Brace for QE Shift

(Bloomberg) -- Bond-market speculation is brewing that a scarcity of short-dated U.K. debt may prompt the Bank of England to skew its purchases in favor of long tenors.

If it does, it would narrow the gap in yield between the bonds, flattening the so-called yield curve, according to BNP Paribas SA and Aberdeen Standard Investments. BOE policy makers, who boosted the asset-purchase plan by 150 billion pounds ($198 billion) last week, have signaled the program may be modified as required.

A sharper drop in long-term yields would help cap debt costs for Prime Minister Boris Johnson’s government as it pushes ahead with a record borrowing plan to fund the nation’s economic recovery from the coronavirus crisis. It would also mean a reversal of a market trend in recent quarters, which saw Britain’s bond curve steepen steadily in response to the surge in issuance.

“There are fewer short-dated bonds available, and they tend to be quite rich already,” said Marco Meijer, a senior fixed-income strategist at BNP Paribas in London. “From this point of view, skewing the purchases a bit longer would make sense. On balance it should put flattening pressure on the gilt curve.”

Heightened focus on quantitative easing reflects expectations that it will be the U.K. central bank’s main policy tool as it fights the economic damage from the coronavirus. The institution, which has already cut interest rates close to zero, is seen as having limited room to lower them further -- money markets have priced out any prospect of the nation’s rates turning negative.

Still, BOE Governor Andrew Bailey said Thursday that the policy known as yield curve control isn’t something he sees a great need for at the moment. The method involves using bond purchases to pin down rates on certain maturities to a specific target. For now, the BOE buys debt equally from three-to-seven-year, seven-to-20-year and 20 year-plus segments.

QE Comfort

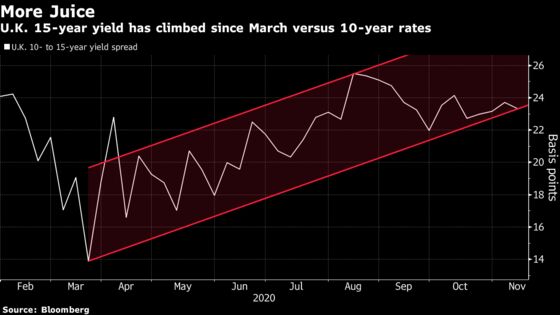

To position for a flatter slope, BNP favors buying 15-year gilts over the Sterling Overnight Index Average, an alternative to Libor, and selling 10-year debt over the same benchmark. This so-called flattener trade would pay off if the longer-term yield fell against the shorter one, relative to Sonia.

NatWest Markets also suggests purchasing 15-year gilts, but against interest-rate swaps. Both the banks are targeting that maturity as its yields look relatively attractive versus the rest of the curve.

The BOE’s willingness to boost quantitative easing is a source of comfort for investors and should help contain volatility, according to Theo Chapsalis, head of U.K. rates strategy at NatWest Markets.

“Dealers should feel more comfortable holding gilt inventory given the support from QE,” he said.

Being Predictable

Not everyone expects the BOE to modify its buying pattern.

The institution likes to be as predictable as possible and has always preferred to keep purchases equal across sectors, according to John Wraith, head of U.K. and European rates strategy at UBS Group AG. Also, larger buying in the far maturities could undermine longer-term investors by driving down yields.

“Going beyond 15 years helps the economy how?” said John Roe, head of multi-asset funds at Legal & General Investment Management. “It hurts pension schemes.”

And, the availability of short-dated gilts could improve as the U.K. issues more debt, reducing the need for the BOE to step up purchases of longer maturities.

What Bloomberg Economics Says:

“Right now if the BOE tried to buy the 150 billion pounds in equal buckets across the curve it wouldn’t be able to without breaking the 70% constraint at the short end (three-seven-year bucket). There is a lot more space at the long end. What that ignores is what the Debt Management Office does in coming months. They have been issuing a lot more short-dated debt so if they continue that (and it is eligible) it will automatically make space for the BOE to buy more without changing the parameters.”

-- Dan Hanson, Senior U.K. Economist

Yet it’s a debate that’s unlikely to go away soon.

“As the BOE owns more and more of the gilt market, they may be forced to buy further out on average,” said James Athey, a money manager at Aberdeen Standard. If this happens, “I would expect the yield curve to flatten, depending on the magnitude of the BOE change of approach, of course.”

Next Week:

- Auctions of conventional bonds from Germany, France and Spain are expected to total 20 billion euros ($24 billion), according to Citigroup Inc.

- There are no redemptions until France pays 20 billion euros on Nov. 25, while Italy is due to pay small coupons next week

- The U.K. will hold three regular gilt auctions, selling a combined 7.75 billion pounds and buying back 4.4 billion pounds of debt across three operations

- Data releases in the euro-area and Germany are backward-looking and second-tier

- U.K. continues with a busy data schedule with October inflation figures on Wednesday and retail sales numbers on Friday

- ECB President Christine Lagarde makes five appearances next week, offering her opportunity to expand on views expressed this week that more bond buying and ultra-cheap loans are the main policy measures in the central bank’s toolbox

- BOE Governor Andrew Bailey speaks on Tuesday; Jonathan Haskel, Dave Ramsden and Andy Haldane are also on the speaker docket next week

- Fitch Ratings reviews Portugal on Friday

©2020 Bloomberg L.P.