Fidelity, Vanguard Buy Turkish Debt as New Central Banker Tested

Turkey Bulls Regroup in Dollar-Debt Market as Default Risk Ebbs

(Bloomberg) --

By certain measures, Turkey looks a lot like Latin America’s worst serial defaulters. But some investors -- including Fidelity International Ltd. and Vanguard Asset Management Ltd. -- are finding plenty to like.

Since President Recep Tayyip Erdogan fired his market-friendly central bank governor last month, the cost of insuring Turkish sovereign debt has risen to the highest in emerging markets after Argentina. The lira nosedived and a gauge of one-year default probability jumped to a record on concern about central bank reserves, foreign borrowing needs, and a surge in coronavirus cases that imperils tourist revenue.

The new governor, Sahap Kavcioglu, has sought to calm investors ahead of his first interest-rate meeting on Thursday, saying a rollback of his predecessor’s hikes shouldn’t be assumed.

For the bulls, the selloff went too far, and Fidelity and Vanguard have both raised their exposure to Turkish hard-currency debt to overweight. Unlike Argentina and Lebanon, which defaulted in 2020, Turkey has sufficient cash buffers, while climbing default swaps are a technical quirk, they say.

“We think a Turkish debt default is unlikely in the near-term,” said Paul Greer, a London-based money manager at Fidelity. “Turkey is heavily reliant on foreign capital to fund its natural current account deficit and the external financing requirements of its corporate and financial sectors. To that end, we expect Turkey to continue to demonstrate its willingness and ability to service its foreign and domestic debt obligations.”

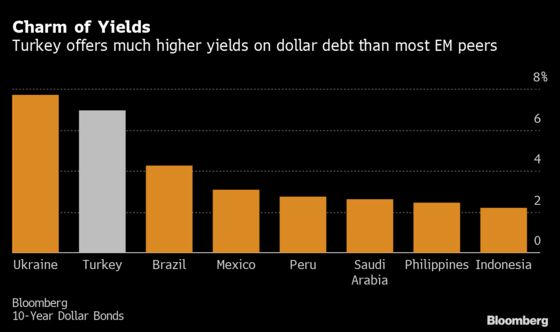

Investors are gravitating toward the foreign-bond market after Naci Agbal’s shock dismissal on March 20 hammered the local currency and left local-debt investors burned. The gains on Turkey’s dollar bonds are triple the emerging-market average this month, a Bloomberg Barclays index shows. The extra yield Turkey pays on government dollar debt compared with U.S. Treasuries fell one basis point on Tuesday to 505 basis points, a higher premium than that of Nigeria and Egypt.

Turkey offers “attractive entry points for alpha opportunities,” Greer said.

Rates Debut

The lira is down more than 8% against the dollar this year, the worst performance after the Brazilian real and the Argentinian peso. But there are signs the worst is over for now. The currency gained 0.2% on Wednesday and has been range-bound this week, while credit-default swaps have unwound some of their gains since late March.

The swaps’ surge was due more to their use as a hedge by investors trapped in overweight positions than as a true wager on default, according to Nick Eisinger, co-head of emerging-markets active fixed income at Vanguard in London.

Compared with defaulted sovereigns, Turkey’s debt burden is comparatively low at 37% of gross domestic product. The equivalent level for Lebanon and Argentina is 172% and 97%, respectively.

“Turkey’s financial sector is very well embedded in global financial architecture,” said Sergey Dergachev, senior portfolio manager for emerging-market debt at Union Investment in Frankfurt. Those close ties to European and Gulf lenders means any default would be a huge reputational blow for the lenders.

“This is a big difference versus Argentina,” Dergachev said.

Akbank TAS, which typically sets the benchmark for other Turkish banks, borrowed about $677 million in a two-tranche syndication last week at a similar cost to a facility in October.

Reserves Risk

At the same time, investors are paying close attention to Turkey’s foreign reserves. Before Agbal’s arrival at the central bank in November, the previous Treasury and Finance Minister came under attack for burning through the stockpile in a bid to stem the lira’s losses. Erdogan has said no reserves were lost.

One possible danger lies in the central bank’s practice of borrowing tens of billions of dollars from lenders via swaps. While banks are sitting on $221 billion of hard currency deposits, lira weakness could prompt Turks to withdraw their savings from lenders, forcing the central bank to close its swap positions.

“They are walking a tightrope, which is why the market is so obsessed about them needing to run tight monetary policy,” said Manik Narain, the head of EM cross-asset strategy at UBS AG.

©2021 Bloomberg L.P.