A $2.5 Billion Default Shows China’s Lack of Mercy for Firms

A fresh signal that Beijing is willing to let ailing state-linked firms fail in order to instill stronger financial discipline.

(Bloomberg) -- China will almost certainly let a high-flying chipmaker default on $2.5 billion worth of dollar debt, the strongest signal yet that foreign investors shouldn’t count on Beijing to bail them out.

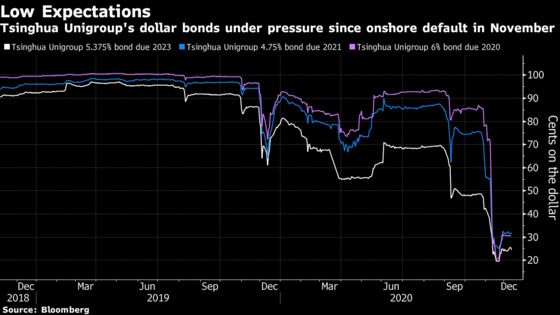

Tsinghua Unigroup Co. said it won’t be able to repay the principal on a $450 million dollar bond due Thursday, which would trigger cross defaults on a further $2 billion of debt. This would be the company’s first dollar bond repayment failure and came after it defaulted on a 1.3 billion yuan ($199 million) local bond last month.

While investors weren’t exactly taken by surprise -- the bond was indicated at about 29 cents on the dollar before it was suspended -- the default will force them to reassess the creditworthiness of weaker state-linked companies. The news had little immediate effect on broader financial markets in China, which will be reassuring to authorities aiming for more realistic pricing of bonds without triggering wider contagion.

The impending default is yet another example of the downfall of a Chinese company that relied on debt to expand. About five years ago, Unigroup was one of China’s most aggressive acquirers, with its then-chairman becoming a billionaire and the company even planning to make a bold $23 billion bid for memory-chip giant Micron Technology Inc.

“The government has been gradually breaking implicit guarantees of weak SOEs,” said Wu Qiong, executive director at BOC International Holdings Ltd.

There has been a spate of defaults by state-owned enterprises in recent weeks, including Brilliance Auto Group Holdings Co., an automaker linked to BMW AG, and Yongcheng Coal & Electricity Holding Group Co. Speculation has increased that Beijing will let weaker SOEs fail, especially as the economy recovers from the pandemic-driven slump.

Such a drive would fit with the Communist Party’s strategy of giving markets greater sway as it seeks to build a stronger, more efficient economy. While the government has taken measures to unshackle its capital markets, such as a flexible approach to pricing initial public offerings, the moves have been accompanied by crackdowns on firms and sectors seen as posing a threat to the financial system.

Still, Unigroup’s potential $2.5 billion dollar-bond defaults is shocking for its scale given the relative scarcity of payment failures outside the domestic market. That’s more than 60% of the total defaulted debt seen in China’s offshore bond market all of last year.

The chipmaker also won’t pay interest on a 5 billion yuan, 5.2% note due Thursday, something it had previously warned might happen. Issuing an apology to bondholders, Unigroup said in a filing to the Shanghai Stock Exchange it’s looking for fresh funding and will seek payment extensions and debt resolution.

The company’s finances deteriorated sharply in the last three years after it embarked on a borrowing spree to fund takeovers and other investments intended to boost its position in the chip industry.

The firm is a business arm of Tsinghua University, the country’s top tertiary institution that counts President Xi Jinping as an alumnus. The company’s net loss widened to 3.38 billion yuan in the first half this year from 3.2 billion yuan a year ago, according to the firm’s latest interim financial report.

“We should see rising refinancing and repricing risk for weaker state-linked firms, which will lead to a rising default rate,” said Andrew Chan, an analyst for Bloomberg Intelligence. “Bailouts are unlikely, in our view, as China aims to restructure, consolidate and eliminate zombie-like state-linked firms unless it leads to systemic risk.”

| Read more about China’s defaults |

|---|

| When 31% Recovery Is Beautiful for Bond Holders: Shuli Ren |

| Why China’s Debt Defaults Are More Alarming This Time: QuickTake |

| China State Firms Once Deemed ‘Safe’ Now Rocked by Defaults |

| The Ticking Debt Bomb in China’s $15 Trillion Bond Market |

| China University-Backed Chipmaker Shows Fresh Signs of Stress |

Unigroup’s three other bonds to be affected by the cross defaults are a $1.05 billion note due 2021, a $750 million bond due 2023 and a $200 million bond due 2028, the company said in a filing to the Hong Kong stock exchange late Wednesday.

“The next default event to watch out for could be its parent company Tsinghua Holdings, but their bonds are already trading at distressed levels so it’s being priced in,” Chan said. “This event will prompt rising concern about onshore stress spilling over into the offshore market.”

On Monday, a Unigroup official said during a meeting with creditors that a working group led by government officials and Tsinghua Holdings Corp. were drawing up proposals for resolving its debt problems, people familiar with the matter said. They added the official said there’s hope that a detailed plan will emerge in the near term, with the likelihood of bringing in new funds or investors.

©2020 Bloomberg L.P.