Trump’s Trade War Is Uniting ECB Hawks and Doves

Trump’s Trade War Is Uniting ECB Hawks and Doves

(Bloomberg Opinion) -- Europe's central bankers suddenly appear more unified than at any time since the 2008 financial crisis. That's good for euro-zone stability and growth; and, ironically, Europe can thank U.S. President Donald Trump for it.

Since the financial crisis, the European Central Bank's governing council has essentially been divided into two feuding camps: The German representatives, with their aversion to inflation, and the Mediterranean members who want to keep central bank asset purchases and easy money flowing. Inflation fears are so ingrained in German thinking that quantitative easing, and the decline in the euro it provoked, has often seemed a bitter pill for savings-focused Germans, and especially for the ultra-conservative Bundesbank.

But thanks to Trump, the ECB governors now had more in common as they sat down on Thursday than they do sources of disagreement. A major objective of Trump's tariff war is to restrict German exports into the U.S. market and encourage German car companies like Volkswagen to move production facilities and jobs to the U.S. to take advantage of protectionist barriers; Wednesday’s news of possible further tariffs of up to 25 percent on foreign-made automobiles will no doubt alarm Germans. Trump has also sought to use the threat of tariffs and sanctions to force European countries to increase their military spending as well as to pressure Germany into supporting sanctions against Iran.

A sharp cut in exports to the U.S., which is a huge market for Germany, would also cost profits and jobs, neither of which would be easy to make up without currency declines. Other Trump policies also impact German interests. Both German and Italian firms do considerable business with Iran and stood to benefit from the end of sanctions there.

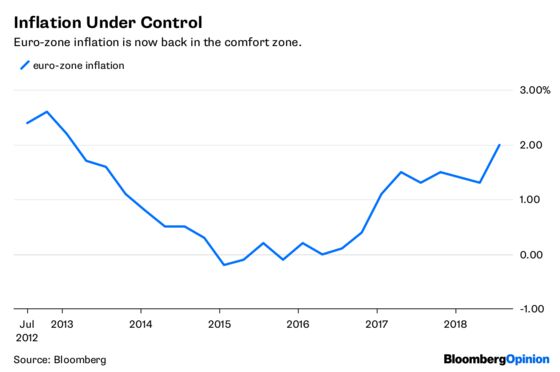

Meanwhile, Germans appear to be catching on to the fact that there are bigger threats than inflation. Inflation has been extremely stable since the ECB was formed in 1998. If inflation has been a problem for Germany and Europe it is because it has been too low to stimulate economic growth, not too high.

At the June ECB meeting the Bundesbank displayed uncharacteristic nonchalance in supporting the change to the ECB’s forward guidance to postpone future interest rate increases until at least the end of the summer 2019, even though that was certain to put downward pressure on the euro’s value. There was also agreement to hold off for an "extended" period of time from shrinking the ECB balance sheet, which markets have taken to mean two to three years from this December when the QE program is due to end.

Trump has accused Germany of supporting a cheap euro to boost its exports. But, ironically, it’s thanks to Trump that Germany’s interests are more aligned with neighbors it once saw as undermining the credibility of the euro zone with their demand for looser money generated by more QE asset purchases.

The U.S. president sees the multilateral, sovereignty-pooling EU as embodying everything he disdains. The Germans should counter this by setting aside their inflation aversion and also by being more willing to share financial risks with, and even transfer income to, the Mediterranean countries. An EU-level deposit insurance — something the Germans have been resisting — would also demonstrate that Europe's biggest power is committed to further integration and that euro zone economies will not easily be divided.

There are those in Germany who will still argue the hawkish line. But in the current international environment, the Bundesbank would be right to go along with a policy of stretching out the withdrawal from QE. It should be open to the possibility of bringing back QE policies should the euro-zone economy falter -- or even to go for a further postponement of interest rate increases into 2020, if the need arises. The need to worry about inflation risks is much less urgent for Germany now that it is facing a hostile presence in the White House.

Trump’s attack on the existing order has raised the stakes for European integration. If Trump and Russian President Vladimir Putin, another destabilizer, are to be thwarted, it will require a deeper German commitment to euro-zone growth and integration. It will also take the realization that monetary policy, migration policy, Brexit and European reforms are all related. That may make the inflation hawks uneasy and will trouble those Germans who feel less disciplined euro-zone countries lean too heavily on Germany. But those arguments carry less weight these days. The man who would divide the EU may turn out to be its great unifier.

To contact the editor responsible for this story: Therese Raphael at traphael4@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Melvyn Krauss is a senior fellow at the Hoover Institution at Stanford University and an emeritus professor of economics at New York University.

©2018 Bloomberg L.P.