Trump Pounces on Wavering Fed to Hammer Home Rate Cuts

Trump Pounces on Wavering Fed to Hammer Home Rate Cuts

(Bloomberg Opinion) -- In his first comments on Twitter about the Federal Reserve since its decision last week to leave interest rates unchanged (but signal that a cut may be coming soon), President Donald Trump seemed to sense that policy makers were on the verge of giving him what he wanted.

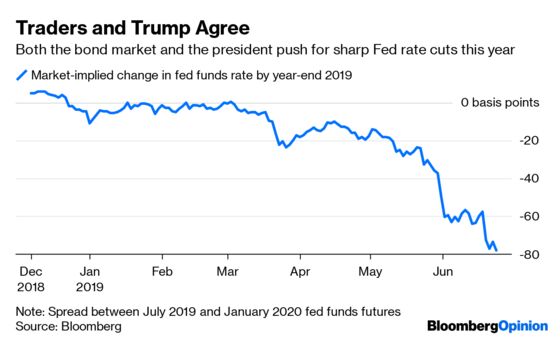

So in between a couple of insults, he laid out why they ought to lower interest rates in July, as bond traders fully expect:

Whether he typed this out off-the-cuff is anyone’s guess (though the fact that the second tweet came instantaneously suggests it was pre-written). But with inflation still below the central bank’s target, job gains slowing a bit and other key data missing estimates, Trump and his team probably feel they have the wind at their backs in advocating for easing policy. Perhaps more important, though, is that this unprecedented public criticism has reached a sort of tipping point — rather than the Fed being seen as exerting its independence by defying the president’s calls for rate cuts, Chair Jerome Powell and others now risk being seen as unduly political if they refuse to lower rates.

In fact, former Fed Vice Chairman Stanley Fischer made some stunning comments before the central bank’s latest decision. During a talk in Israel, he said policy makers might not have raised interest rates in December if Trump hadn’t been pounding the table for cuts. “It’s not a desirable thing to have the president pronouncing on monetary policy,” he said. “What the president has understood is that he can have a one-way bet by announcing what he thinks they should have done.” Basically, Trump has nothing to lose from accusing the Fed of bringing about a recession — either the economy slows down and the Fed becomes his scapegoat, or it doesn’t and he boasts about its strength.

If the December interest-rate increase was at all political, it was only at the margin. Sure, equity prices were falling, but the general consensus was that policy makers would hike and then signal an extended pause, which Powell did in early January. That has never been good enough for Trump, who has called for reducing interest rates by a full percentage point and demanded the Fed immediately “stop with the 50 B’s” when it came to monthly reductions in its balance sheet. Neither has happened yet.

Again, it’s virtually impossible to know whether Trump’s criticism played a role. If anything, the bond market has been a bigger factor than the president in getting the Fed to alter course.

At the same time, the political stakes are only mounting. Bloomberg News reported last week that the president believes he has the authority to demote Powell to the level of board governor. Powell responded at his press conference that “I have a four-year term, and I fully intend to serve it.” Then, in an NBC interview aired Sunday, Trump said that he didn’t threaten to demote his pick to lead the Fed but that he’d “be able to do that if I wanted.”

There are few winners in a world in which the most important central bank becomes politicized, but Trump senses he may be one of those rare victors. It doesn’t take a political mastermind to realize that the strength of the U.S. economy in recent years — not to mention record stock-market prices — will be one of the main talking points as he seeks re-election. His very next tweet after his Fed comments, in fact, was to reveal a new fund-raising platform. To top it off, the first Democratic presidential primary debates are this week. Trump has a lot riding on keeping the good times going, and he sees easier monetary policy as a way to make that happen.

One of the stranger things is that if Trump truly wants the Fed to lower interest rates in a hurry, he has an incentive to keep trade tensions with China elevated after this week’s pivotal Group of 20 meeting. A recent Bloomberg Economics’ analysis of data on more than 10,000 U.S. import categories showed the trade war has struck a significant blow. “The break in supply of crucial inputs is imposing significant costs on U.S. manufacturers,” Tom Orlik and Maeva Cousin wrote. Indeed, on Monday, a Dallas Fed manufacturing index fell to the lowest since mid-2016.

Because of these trends, the Fed’s new favorite word appears to be “uncertainty.” Officials seem to have tilted a bit away from data dependency and are thinking more about the path forward in the months ahead. Clearly, based on their updated dot plot, many see a case for reducing rates in the coming 18 months. Just in time for the 2020 election.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.