Treasury Yields May Take Another Step Down Thanks to Mortgages

Treasury Yields May Take Another Step Down Thanks to Mortgages

(Bloomberg) -- The mortgage market was supposed to be quiet this year, but suddenly it’s moving the biggest bond markets.

When Treasury yields started falling in March after a surprise Federal Reserve policy shift, mortgage-bond investors helped push them even lower as they looked to hedge their holdings. Now yields have taken another leg down, given another nudge on Wednesday by weaker-than-expected U.S. inflation data. Traders could be poised to do more hedging, especially if rates on home loans drop about 0.3 percentage point from last week’s levels, said Walt Schmidt, head of mortgage strategies at FTN Financial in Chicago.

“If mortgage rates fall below 3.5%, then that’s a big deal,” Schmidt said, because more investors may look to hedge when 4% mortgages can be refinanced. “That could add some downward force to Treasury yields.”

Those declines may be coming soon, if they haven’t yet. Treasury yields have fallen about 0.35 percentage point since the beginning of May, and in recent sessions have reached their lowest levels since 2017 as weaker-than-expected job and inflation data have bolstered the case for the Federal Reserve to cut rates. That kind of drop in yields often pulls down mortgage rates too. Freddie Mac releases the results of its weekly mortgage rates survey on Thursday.

There are already some signs of lower yields translating to more buying from mortgage bond investors. Hedging may have led to about $150 billion of buying in 10-year Treasury equivalents in May, Barclays Plc strategists Dennis Lee and Anuj Jain wrote last month, and Wells Fargo & Co. analysts also attributed some of the recent rates rally to convexity hedging from mortgage servicers.

Another drop in rates could increase investors’ hedging needs because “investors may not have been prepared” for how rapidly rates have slid in the last few months. The 10-year yield, now at around 2.13%, stood at 2.75% at the start of March.

According to Barclays, about a third of investors in mortgage bonds look to protect themselves against a risk particular to the securities: that rates will fall and homeowners will refinance their loans. That refinancing translates to bond investors getting principal back sooner than they had planned, cutting into their returns and the duration of their portfolio. Money managers that hedge this risk, known as negative convexity, often respond by buying Treasuries when yields fall, to add duration to their portfolio, which in turn can help pull yields lower, creating a self-reinforcing cycle.

Mortgage hedging last took the spotlight in March when 10-year Treasury yields dropped below 2.5% in the aftermath of the Fed meeting, and reached as low as 2.34% later that month. Citigroup strategists attributed some of the speed of that drop to a pickup in hedging. Yields below 2.25% could open up additional hedging needs, Scott Buchta, head of fixed-income strategy at Brean Capital, said in a note last month.

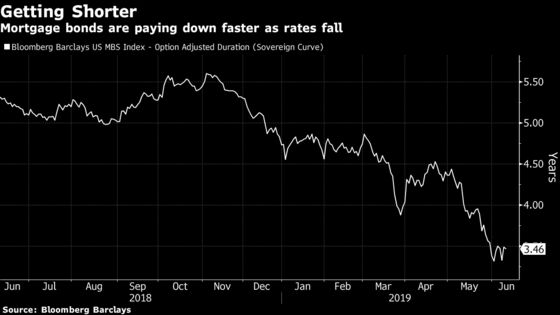

With those lower yields, more borrowers are already showing signs of refinancing their home loans, and paying them down faster. U.S. mortgage refinancing applications surged last week to their highest level since 2016, the Mortgage Bankers Association said on Wednesday. The duration of the Bloomberg Barclays U.S. Mortgage Index has dropped to about 3.5 years, down from 4.9 years in early March, on an option-adjusted basis.

The speed at which Fannie Mae and Freddie Mac bonds are paying down jumped 18% in May, and mortgage analytics firm Black Knight estimates that 6.8 million out of a universe of 44 million homeowners could save at least 0.75 percentage point if they refinanced. The 0.75 percentage point level has historically been the threshold for sparking an uptick in paydowns and refinancings, according to the firm.

Not everyone is convinced that this sort of hedging will have a big impact on the Treasury market. The single biggest holder of mortgage bonds is still the Fed, which has over $1.5 trillion of the securities, or about 21% of the market, and doesn’t hedge its holdings.

“The option-adjusted duration of the mortgage universe is most certainly falling,” said Praveen Korapaty, chief global rates strategist at Goldman Sachs Group Inc. “It may give the 10-year Treasury yield a kick lower for a few basis points for a few days. But it won’t be a sustainable kick lower in yields.”

But some investors say it makes sense to better protect portfolios against falling yields. Ian Anderson, a mortgage-bond analyst at Loomis Sayles & Co., said he has been buying securities that perform better when more borrowers are refinancing.

“We’re positioned for more negative convexity,” said Anderson, whose firm manages $264 billion.

--With assistance from Mark Tannenbaum.

To contact the reporters on this story: Claire Boston in New York at cboston6@bloomberg.net;Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Dan Wilchins, Boris Korby

©2019 Bloomberg L.P.