Treasury Volatility Bet Is Paying Off as Blue Wave Hopes Fade

Treasury Volatility Bet Is Paying Off as Blue Wave Hopes Fade

(Bloomberg) -- A large option wager that Treasuries will see less volatility than many had expected over the U.S. elections is paying off.

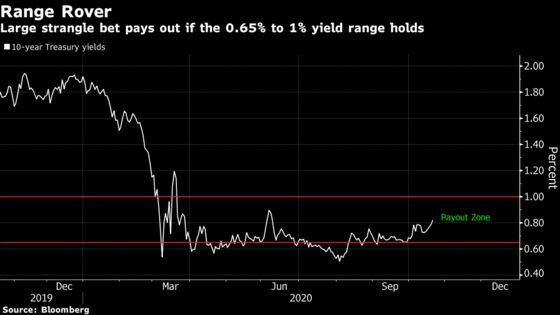

The bet was simple. A short position was built up in a so-called strangle on 10-year Treasuries -- a pair of upside and downside options -- which generated more than $31 million in premium.

It pays off if 10-year bond yields remain between 0.65% and 1% to the options’ expiry on Dec. 24. A break out in either direction though could have left the volatility seller with potentially unlimited losses.

The valuation of these options have collapsed as early polling results suggest that a Democratic sweep of both the presidency and the Senate, the so-called Blue Wave, is unlikely to happen. That’s left yields at around 0.8% as expectations for aggressive fiscal-spending plans from the Democrats are unwound.

As a result, the contracts are worth just $25 million, according to Bloomberg’s calculations, meaning the trader has realized a gain of over $6 million.

Not bad for a two-week wager.

©2020 Bloomberg L.P.