Treasury Levels Seen as `Danger' by Templeton's Desai

Treasury Levels Seen as `Danger' by Franklin Templeton's Desai

(Bloomberg) -- This year’s rally in Treasuries is an opportunity to sell or get short before the Federal Reserve signals more tightening in the second half of the year, according to Franklin Templeton.

Expectations that the Fed’s next move will be a cut are mistaken, since the central bank’s forbearance in January largely reflected equity market conditions, Sonal Desai, chief investment officer for fixed income at Franklin Templeton Investments, said in a Bloomberg Television interview. Gains in stocks and a strong economy mean the rally in bonds won’t hold, she said.

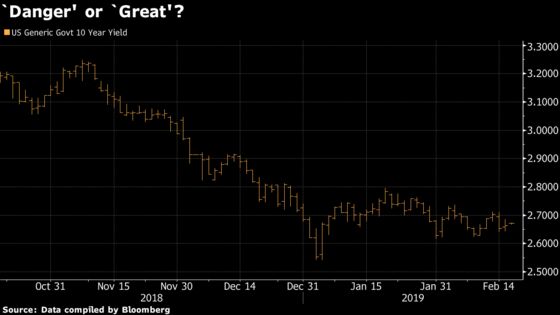

Sovereign debt in the U.S. have gained in recent months as the Fed indicated it would be patient on hiking rates, with the yield on the 10-year Treasury bond falling almost 60 basis points from the 3.25 percent highs in November.

“For anybody who takes this market pricing as fact, there’s danger there,” she said in Hong Kong. “Rather than buying, I’d be selling. I’d be looking for interesting places to put shorts on.”

Ten-year bond yields could reach 3.5 to 4 percent in the medium term, Desai added. “Being short U.S. Treasury duration is going to be safer than being long duration,” she said.

U.S. money markets traders are pricing that the Fed will hold steady throughout this year, before the chance of a rate cut gradually climbs in 2020. Still, Templeton’s views are shared by others, who also see the U.S. central bank raising rates.

Overly Pessimistic

There’s a reasonable chance of one or two increases in the second half of 2019, and markets may be “overly pessimistic on growth,” according to Campe Goodman, senior managing director and fixed-income portfolio manager at Wellington Management Company LLP. The front end of the curve will probably move higher, he said.

“I don’t think rates are excessively high now but any increase will be on the basis that it would not have a dampening effect on the economy,” Goodman said in an interview in Singapore. “We saw the rate-sensitive sectors of the economy slow last year -- in housing and autos -- that suggests to me that higher rates did have an effect.”

Households in the U.S. curbed their spending on real estate and cars after the Fed hiked interest rates four times in 2018.

Bob Michele, JPMorgan Asset Management’s chief investment officer for global fixed income, also said in a Bloomberg Television interview Tuesday that in an environment where the Fed hikes once or twice in 2019, “the 10-year will be dead at around 2.75 to 3 percent and there won’t be a lot of upward pressure or downward pressure,” he said. “For us as bond investors that’s great -- we like a stable bond environment.”

With stocks back up again and the U.S. consumer looking healthy, the central bank can turn more hawkish from here, Franklin Templeton’s Desai said. She wrote in a blog post this month she expects at least two rate hikes this year.

--With assistance from Sophie Kamaruddin, Bryan Curtis, Adrian Wong and Ruth Carson.

To contact the reporter on this story: Gregor Stuart Hunter in Hong Kong at ghunter21@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Tan Hwee Ann, Joanna Ossinger

©2019 Bloomberg L.P.