Treasury Curve Steepens to February 2016 Levels Before Sales

Treasury Curve Steepens Toward Level Last Seen Around 2016 Vote

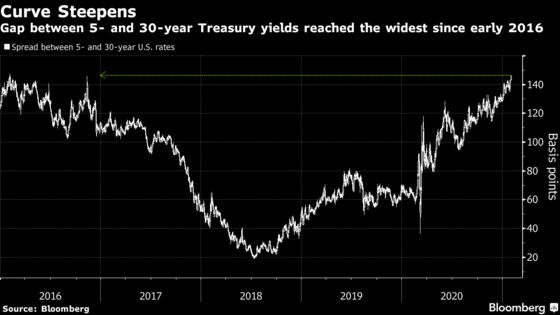

(Bloomberg) -- A widely watched segment of the Treasury yield curve has reached its steepest level in almost five years as expectations for more stimulus overshadowed the government’s decision to leave auction sizes for long-maturity debt unchanged.

The gap between 5- and 30-year yields touched 147 basis points, the widest level since February 2016. The driving force was a sell-off in long-dated debt, which continued even after the Treasury announced Wednesday that there would be no increase in sales of notes and bonds at next week’s quarterly refunding sales. The decision was in line with Wall Street forecasts, though a minority had seen another round of increases.

The curve has been on a steepening trend since July, mostly staying above its 55-, 100- and 200-day moving averages. Drivers include improving prospects for another round of pandemic-relief spending as well as rising expectations for consumer-price gains, reflected in higher breakeven inflation rates for inflation-linked debt.

“The curve is moving on the idea that the stimulus plan is going to get done and inflation is starting to gain steam,” said Tom di Galoma, managing director of government trading and strategy at Seaport Global Holdings. “The front end of the curve is anchored because the Federal Reserve can’t raise rates, but the back end is vulnerable to selling off because of the perception that inflation is building.”

A widespread view that more stimulus is on the way should be enough to keep the curve climbing, at least while the Federal Reserve remains reluctant to ramp up asset purchases, notes Gennadiy Goldberg, U.S. rates strategist at TD Securities Inc.

“We continue to look for a larger bill to be passed, which should put upward pressure on rates,” Goldberg wrote following the Treasury’s announcement of steady issuance this quarter.

©2021 Bloomberg L.P.