Treasuries Surge Despite Strong Jobs Data, Pricing In Slower Fed

Treasuries Surge Despite Strong Jobs Data, Pricing In Slower Fed

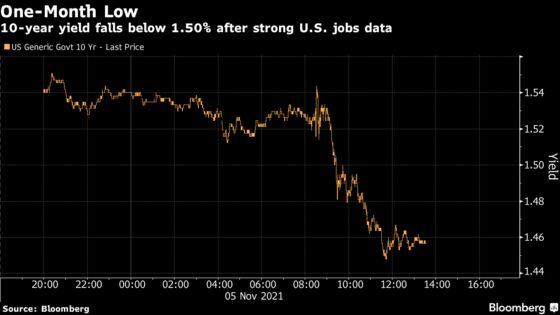

(Bloomberg) -- Treasuries surged Friday despite stronger-than-expected employment data, putting the market on pace for its biggest two-day advance in more than a year.

For a second straight day the U.K. bond market led global declines in government bond yields as investors priced in an extended period of ultra-low central bank rates.

Yields on the 10-year Treasury fell as much as 7.8 basis points to 1.45%, falling below its 50- and 200-day moving averages for the first time since September. Over the past two days it’s fallen by 14 basis points, on track for the biggest decline since June 2020. The U.K. 10-year yield is lower by 23 basis points over the same period.

“The report itself sets a firmer foundation for higher yields,” said Praveen Korapaty, head of interest-rate strategy at Goldman Sachs & Co., referring to October employment data showing payrolls growth exceeded expectations and was revised higher for September. “But there’s a broader environment of markets rethinking how aggressive central banks may get with regard to inflation given the outcome of Bank of England meeting yesterday.”

The U.S. two-year yield declined as much as 3.8 basis points Friday on the heels of a 4.1-basis-point drop Thursday. The U.K. two-year yield is lower by more than 30 basis points since the Bank of England defied widespread expectations it would raise rates.

The jobs data comes two days after the U.S. Federal Reserve, as expected, said it would begin tapering its asset purchases this month, a precursor to raising interest rates. At the announced pace, the taper could conclude by mid-2022. However the pace is subject to change based on economic conditions including recovery in employment metrics toward pre-pandemic levels.

October job creation of 531,000 versus the median forecast of 450,000 is “a good number,” but “not so strong that it would accelerate the Fed’s taper -- and thus rate hike -- timeline,” John Briggs, global head of desk strategy at NatWest Markets said.

After Thursday’s Bank of England decision, U.S. short-term interest-rate markets priced in a later start to -- and slower pace of -- Fed rate increases. Current pricing anticipates a first rate increase in September and a second by February 2023; previously, two increases were priced in for 2022, the first in July.

Friday’s yield-curve flattening is consistent with that, said Alex Li, head of U.S. rates strategy at Credit Agricole.

“The timing of liftoff is being pushed off a bit,” putting pressure on short-term yields, while “lower long-end rates are consistent with growth slowing down” as fiscal and monetary support are withdrawn, Li said.

Gains in Treasuries may be partly driven by short-covering, which appears to have contributed to Thursday’s U.K.-led rally. CME Group Inc.’s preliminary open-interest data for Treasury futures show steep declines, in particular for the two-year note contract. Open interest in two-year note futures fell 2.3%, its biggest drop in three weeks.

Fed officials continue to emphasize that inflation is too high even as they hope to foster labor-market recovery by keeping interest rates low.

Federal Reserve Bank of Kansas City President Esther George Friday said “the risk of a prolonged period of elevated inflation has increased,” and “the argument for patience in the face of these inflation pressures has diminished.”

The declines in 10- and 30-year yields -- which fell as much as 8.4 basis points to 1.88%, the lowest since Sept. 23 -- come despite next week’s auctions of those tenors. The auctions, whose sizes were announced on Nov. 3, are smaller than the previous new-issue auctions in August, however. The reductions were the first since 2016.

The 10-year auction was cut to $39 billion from $41 billion, the 30-year to $25 billion from $27 billion.

©2021 Bloomberg L.P.