Treasuries’ Pain Seen Deepening Amid Grimmest Year Since 2013

For treasuries investors, 2021 could turn out to be even worse than eight years ago even as key measures of inflation surge.

(Bloomberg) -- The Federal Reserve is doing its best to avoid the taper tantrum of 2013 as it moves toward curbing its bond buying. Ironically for Treasuries investors, 2021 could turn out to be even worse than eight years ago.

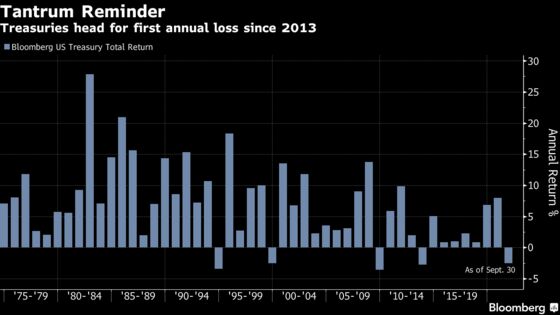

The latest bond selloff -- triggered by a hawkish shift in the Fed’s signal on its policy path -- has left the Bloomberg U.S. Treasury Index down 2.2% this year, on track for the first annual loss since 2013, when it declined 2.8%.

With key measures of inflation surging and coronavirus cases starting to ebb, investors and strategists from firms such as Societe Generale SA and UBS Group AG are bracing for more losses this quarter. Confidence in that view may only grow with the release of monthly jobs data next week, which is forecast to show hiring accelerated in September.

“It may not be a straight line higher, but there’s some catchup to do” for bond yields, said Leslie Falconio, head of U.S. fixed-income asset allocation at UBS Financial Services. “Our expectation is that consumer demand will recover from the setback” of the past few months, when the resurgent virus slowed economic momentum.

Falconio expects 10-year Treasury yields to rise to around 1.75% by year-end, around their peak for 2021. The yield reached about 1.57% this past week -- the highest since June -- before buyers started to nibble.

After several months of stability, global bond markets started to slump last month after central banks including in the U.S. and the U.K. signaled a move to reduce pandemic-era stimulus to head off inflation.

Traders boosted bets that the Fed will start raising rates late next year and lift them almost three times by the end of 2023. A power crunch across Europe and China is also keeping bond investors on edge.

There are plenty of forces that could limit a further selloff. Lawmakers are locked in a standoff over raising the U.S. debt ceiling, with the government weeks away from a possible default, in the estimate of the Treasury. And in China, growth is cooling amid a property-market slowdown and a power shortage.

But so far, international investors don’t seem to be swooping in with significant purchases, a dynamic that has capped Treasuries declines in the past.

The market is hardly anticipating a repeat of the rout eight years ago, when then-Fed Chairman Ben Bernanke triggered a surge in yields after he suggested the central bank could begin to reduce asset purchases. In that episode, 10-year yields jumped more than 100 basis points in four months.

Jobs Crossroads

But traders are now turning to the September labor report for the next potential catalyst for higher yields.

With the Fed all but teeing up November as the likely announcement of a plan to reduce its asset purchases, the payroll report Friday could ratify that view by offering fresh signs of broad economic strength. The median forecast of analysts surveyed by Bloomberg is for a gain of 470,000 jobs in September, double the previous month.

Investors have been tilting toward an extended selloff. A JPMorgan Chase & Co. survey showed that a net 25% of its clients were short Treasuries as of Monday, the most since early September.

Asset Managers Slashed Exposure to Treasuries Into Selloff: CFTC

“If we get a number close to the consensus, we see the potential for yields to rise in the back-end,” said Subadra Rajappa, head of U.S. rates strategy at Societe Generale, who predicts 10-year yields will rise to 1.7% by year-end.

What to Watch

- The economic calendar

- Oct. 4: Factory orders; durable goods orders; capital goods orders

- Oct. 5: Trade balance; Markit US services PMI; ISM services

- Oct. 6: MBA mortgage applications; ADP employment

- Oct. 7: Challenger job cuts; jobless claims; Langer consumer comfort; consumer credit

- Oct. 8: Nonfarm payrolls; wholesale inventories

- The Fed calendar:

- Oct. 4: St. Louis Fed’s James Bullard

- Oct. 5: Vice Chair for Supervision Randal Quarles

- Oct. 7: Cleveland Fed’s Loretta Mester

- The auction calendar:

- Oct. 4: 13-, 26-week bills

- Oct. 5: 52-week bills

- Oct. 7: 4-, 8-week bills

©2021 Bloomberg L.P.