Traders Pricing Seven Fed Hikes This Year as Global Bonds Tumble

Traders Now Betting at Least One Fed Hike Will Be Supersized

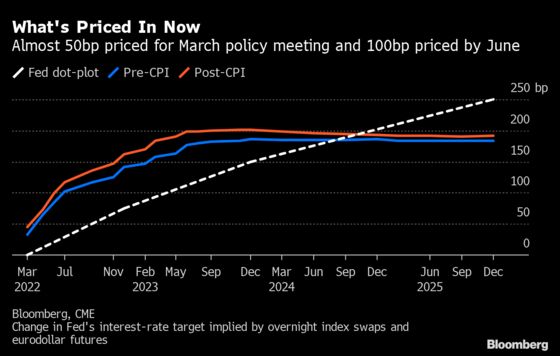

(Bloomberg) -- Global bond yields soared as traders wagered that the Federal Reserve will raise policy rates by 175 basis points by the end of the year, even as officials pushed back against expectations of a super-sized hike next month.

Overnight index swaps on Friday showed traders expect the Fed’s main rate to rise to 1.84% after the December meeting, from the effective rate of 0.08%. Goldman Sachs Group Inc’s economists are now calling for seven consecutive quarter-point hikes, up from the five they’d seen earlier. Two-year Treasury yields resumed gains as cash trading opened, shrinking the gap over 10-year yields to the flattest since April 2020.

The sharp repricing of rate-hike estimates and spikes in benchmark Treasury yields came after the Labor Department reported that consumer prices jumped at a 7.5% annual pace in January, higher than the 7.3% economists expected. That’s the fastest pace since 1982 and ramps up the pressure on the Fed and other central banks to accelerate their pull back from the unprecedented stimulus introduced in the early stages of the pandemic.

“What we do know is that an inflation rate of 7.5% when the funds rate is zero means the Fed has to get going now,” said Gene Tannuzzo, global head of fixed income at Columbia Threadneedle Investments.

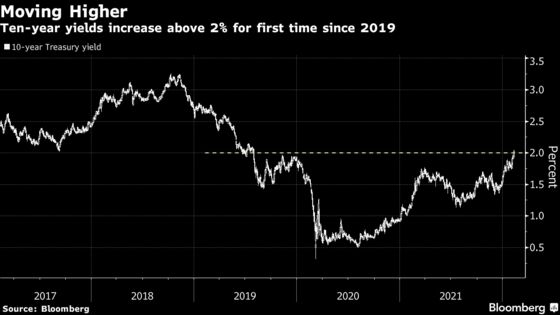

The yield on the policy-sensitive two-year Treasury note doubled its rise for the Thursday session and climbed more than 21 basis points to end the day at 1.58%, the largest one-day rise since 2009. The rate added three basis points to 1.61% Friday. Ten-year yields retreated two basis points to 2.01%, after breaching 2% for the first time since 2019 on Thursday.

The inflation shock was followed by comments from St. Louis Fed President James Bullard, who said he supports raising interest rates by a full percentage point by the start of July, including a 50 basis point hike in March. Other Fed officials, though, have suggested that such an outcome isn’t yet likely.

That helped to ease off market expectations, though swaps traders then focused on the longer-term horizon during Asian hours.

While there’s a case to be made for a 50-basis point hike in March given the combination of very high inflation, hot wage growth and high short-term inflation expectations, the indications from policy makers so far are pointing to more incremental moves, according to Goldman analysts.

With Japan shut on Friday, cash trading of Treasuries was closed until the London session. Instead, Asia-based investors sold bonds in Australia and New Zealand, with the three-year Australian yield jumping 14 basis points to 1.67% and touching levels last seen in March 2019. While Reserve Bank of Australia Governor Philip Lowe pushed back on policy tightening expectations, swaps traders stuck with their bets that he will have to hike in May.

New Zealand’s two-year yields jumped 10 basis points, with swaps traders pricing a better than 35% chance the nation’s central bank will raise rates by 50 basis points when it meets Feb. 23.

Interest-rate futures indicate the Fed’s hiking cycle will end with the overnight rate at 2% in late 2023, up from a recent estimate of 1.6%.

The inflation report and Bullard’s comments sent short-dated yields jumping the most and flattened the Treasury curve, which is traditionally a signal that traders expect economic growth to slow as rates move higher. The gap between 5- and 30-year yields narrowed to as little as 34.5 basis points, its flattest level since late 2018. The yield curve lows came after the regular monthly auction of 30-year bonds caused long-dated yields to climb further and prompted a short-lived bout of steepening.

“Monetary policy works with a lag,” said David Kelly, the chief global strategist at JPMorgan Asset Management. “We’re looking at very much slower growth, and that’s something that the bond market is pricing in -- and that’s why you’re seeing this flattening yield curve.”

Rising Treasury yields have saddled bondholders with losses, with an index of the securities losing 3.8% so far in 2022, marking its worst start to a year since at least 1980. The Treasury index declined 2.3% in 2021, its first annual slide since 2013. Global government bonds have lost 2.8% year-to-date.

Consumer prices climbing by more than 7% was a hallmark of the early 1980s and compelled aggressive tightening by the Fed that pushed the economy into recession.

The bond market and many economists expect inflation is nearing its pandemic-related peak and will subside over the course of the year to 4.8% and then ease to 2.4% by the end of 2023, according to a Bloomberg survey. Bond market expectations of inflation have fallen in recent months, with long-term expectations pacing the move back toward the Fed’s 2% target.

©2022 Bloomberg L.P.