Traders Need to Be More Picky in Betting Against the Dollar

Traders Need to Be More Picky in Betting Against the Greenback

(Bloomberg) -- There may be opportunities for investors to sell the dollar as the global economy rebounds in the second half of 2020, but they need to be fussy about what to trade it against as the U.S. currency looks set to remain broadly resilient.

That’s the view of JPMorgan Chase & Co. strategists who recommend selling the greenback against currencies of industrialized nations with strong current account balances, such as Sweden and Japan, even as they caution against taking an underweight stance on the dollar more generally. On the emerging-markets side, JPMorgan recommends sticking to bets on currencies with high real yields like Mexico’s, Russia’s and Indonesia’s, according to a mid-year outlook published by the bank on Thursday.

The global economic collapse triggered by attempts to contain the ongoing coronavirus pandemic has spurred drastic policy action from central banks around the world, compressing interest-rate differentials between countries. That means structural drivers should become more relevant for currencies, while carry trades should become less salient in driving the market, according to Paul Meggyesi, JPMorgan’s head of global foreign-exchange strategy.

“In a zero interest-rate world, currency markets should become more fundamental,” Meggyesi wrote in the report. “Currencies with structural resilience, big current-account surpluses, and cheap valuations should do well, and thus we expect the Japanese yen to perform well.”

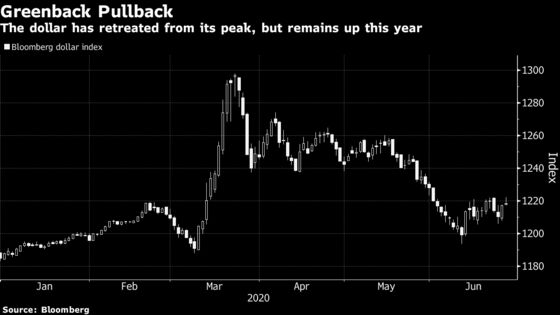

The Japanese yen has gained versus the greenback over the past three months, but has lagged against a majority of its Group-of-10 peers as riskier assets have outperformed. The dollar, meanwhile, has dropped against all of its G-10 counterparts and a Bloomberg gauge of the currency is down more than 6% from its late March peak, although it has plateaued in recent weeks amid growing concern about the virus and the economy.

“To transition to a period of outright weakness in the dollar, we would need to see a stronger and more complete global economic recovery than our economists are expecting,” Meggyesi wrote. For the dollar to weaken to the levels at the start of the year, global growth would need to be around 2 percentage points higher or there would need to be a 3 percentage point deterioration in the relative growth outlook between the U.S. and the rest of the world, according to the strategist.

He expects trade-weighted measures of the dollar to be broadly flat over the next three months or so and then bounce by 0.5% to 1% around the turn of the year as the economic scarring from the pandemic “becomes more apparent and dulls enthusiasm for the recovery trade.”

One factor that could weigh against that is America’s presidential election. According to JPMorgan, a change of administration could potentially dent the dollar by 2% to 3%, depending on the policies of Joe Biden, the presumptive Democratic challenger to incumbent Donald Trump.

©2020 Bloomberg L.P.