Traders Face $400 Billion Headache as Libor Angst Hits Crossroad

Traders Face $400 Billion Headache as Libor Angst Hits Crossroad

(Bloomberg) -- The unprecedented uncertainty surrounding Federal Reserve measures to ease dollar funding stresses and the impact on Libor is creating an insatiable appetite for short-term interest rate options.

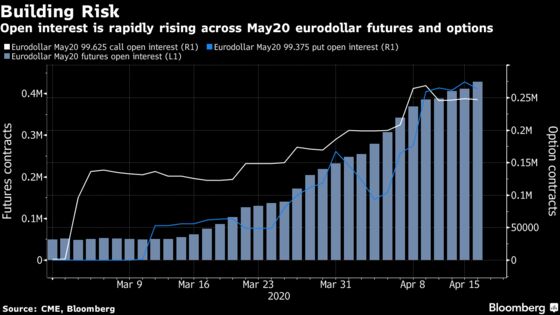

Open interest -- or the amount of new risk -- has topped 400,000 futures contracts in May 2020 eurodollars worth $400 billion. Thursday’s volumes topped 125,000, third most for the May 2020 contract and matched with rising open interest, yet there is no sign of positions being pared.

Uncertainty revolves around expectations for the path of FRA/OIS, the traded version of Libor and an essential tool for pricing eurodollar futures. That spread has narrowed to around 40 basis points, from near 60 at the start of the month.

One factor on which a further tightening of the spread is hinged upon is a return to liquidity in the commercial paper market. The spread there between 90-day AA non-financial paper and 3-month OIS remains elevated, representing a key outlier in the funding markets which the Fed has yet to fix. The central bank this week launched a commercial paper funding facility to ease liquidity constraint in this market. The vehicle purchased just $974 million of securities in the first week of its operation, according to data released Thursday.

Closely attached to the commercial-paper market, the current Libor/OIS spread tightened to 103 basis points Thursday as 3-month Libor rate resumed its recent decline. Credit Suisse Group AG analyst Zoltan Pozsar in a April 15 note forecast Libor/OIS spread narrowing to 75bp by the end of April, now an equivalent of near 3 basis point drop a day over the nine remaining sessions. With May 2020 eurodollar futures -- due to roll off May 18 -- trading the equivalent of OIS +57bp, there shows an expectation that the Fed’s commercial paper fix may have a positive effect on driving down FRA- and Libor/OIS spreads toward Credit Suisse’s forecast. Option trades for an extending tightening in those spreads emerged Wednesday.

Another issue. The May 2020 futures expiration incorporates the April 29 FOMC meeting, when the committee is widely expected to raise the interest on excess reserves. The OIS curve is pricing in an 8bp Fed effective rate vs. 5bp currently, indicating a 3bp “tweak” higher. Should the move be more or less, this would also impact where the May 2020 eurodollar contract settles.

Lastly, an expected influx of Treasury bill supply stands to effect both expectation for the Libor-OIS path and the potential for an IOER tweak at the April Fed meeting. In terms of Libor-OIS, the expected avalanche of bills stands to push short-term rates wider, acting as a potential floor for Libor-OIS tightening and eliminating the need for an IOER hike.

“There is some sense in waiting to see how the ongoing flood of bill supply is going to impact the front-end rate complex before trying to push EFFR higher,” NatWest Markets strategist Blake Gwinn said in April 16 note.

©2020 Bloomberg L.P.