Traders Are Grappling With a Whole New World of Bond Volatility

Traders Are Grappling With a Whole New World of Bond Volatility

(Bloomberg) -- Bond volatility is accelerating as Covid-19 and inflation fears play havoc with the policy outlook.

Treasury yields surged Wednesday after Federal Reserve Chair Jerome Powell suggested Tuesday that stubbornly high inflation warranted increasing the pace of policy tightening. That saw the market reverse course after benchmark 10-year yields fell to a two-month low this week on fears over omicron’s resistance to existing vaccines.

The whipsaw trading in bonds is threatening to compound the nervousness that has spread across financial markets as the recovery from the pandemic threatens to go off the rails. The higher the debt-market volatility gets, the greater the prospect it will filter through to spook stocks, which are still not far from record highs despite this week’s declines.

“The shift from one sentiment to another -- it’s quite surprising how quickly that’s happened,” said Georgina Taylor, a fund manager at Invesco Asset Management, in an interview on Bloomberg Television. “What it probably reflects bigger picture is that markets are trading on news flow, as opposed to maybe taking that slightly longer term view.”

Hedge funds have suffered losses in recent months when bond yields suddenly surged on inflation bets. Then, as investors brought forward wagers for rate hikes, central banks pushed back on those expectations to send yields lower.

After insisting for months that inflation is probably transitory, Powell in testimony to the Senate Banking Committee said it was time to retire the term, and possibly for the Fed to move more quickly toward raising interest rates by winding down its asset-purchase program faster. The new coronavirus variant, which last week caused a growth scare, also has inflationary potential by worsening supply-chain problems, he said.

That’s prompted money markets to ramp up rate-hike bets, with traders betting on two Fed rate increases by November. The shift has implications for other central banks too. Money markets priced in an interest-rate hike from the European Central Bank in December 2022 for the first time since the news of the Omicron variant incited traders to taper bets.

Transition Time

“What’s going to create a lot of volatility is the transition from one environment to another,” said Kathryn Kaminski, chief research strategist and portfolio manager at AlphaSimplex Group in Cambridge, Massachusetts, which oversees about $6.4 billion. Powell ditching “transitory” is “this pivot into an different environment from a macro perspective,” she said.

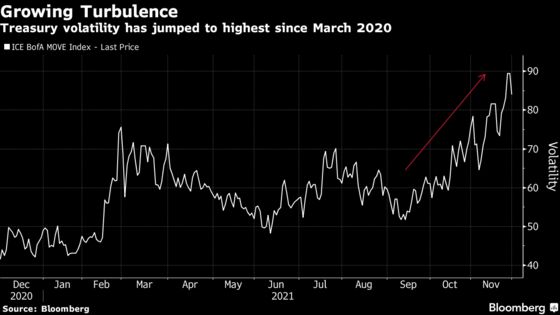

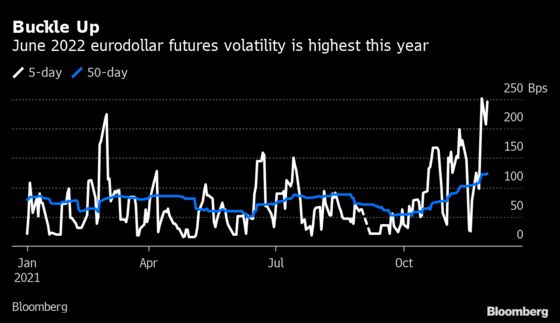

The June 2022 eurodollar futures contract, which can be used to bet on Fed policy, has seen historical volatility over a five-day period surge to the highest in more than a year. Its 50-day average has been rising since mid-September. Meanwhile, Treasury market implied volatility over the next 30 days, as measured by the ICE BofA MOVE Index, has climbed to the highest since the initial pandemic selloff in March 2020.

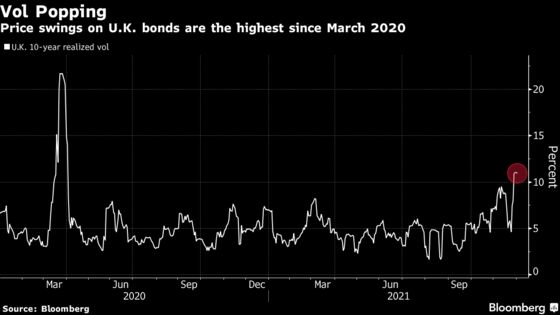

Volatility is also spiking across global markets. A gauge of expected price swings on U.K. 10-year bond futures has more than doubled in the space of two weeks, climbing over 10% for the first time since March 2020. Across to the Asia-Pacific, a measure of implied Japanese bond swings jumped to the highest since March, while price swings for Australian 10-year bond futures last week rose to the most since April.

U.S. 10-year yields were five basis points higher on Wednesday at 1.50%, after falling five basis points on Tuesday. Two-year yields climbed three basis points to 0.60%, approaching the high of 0.65% reached last week, which was the most since March 2020.

“A week ago the Treasury market was preparing for a higher interest-rate environment next year,” said Michael O’Rourke, chief market strategist at JonesTrading Institutional Services in Stamford, Connecticut. “This Treasury squeeze in reaction to omicron caught investors off guard, and now Powell’s comments caught them off guard once again. That sets the stage for additional volatility for both bonds and stocks.”

U.S. payrolls data on Friday, inflation numbers next week, and the mid-December Fed meeting will play out against this febrile macro environment, as well as year-end liquidity constraints that can also promote volatility.

“The November data will show elevated payrolls and inflation and reveal the Fed is behind the curve, while omicron leaves the data horizon looking foggier,” said John Brady, managing director at RJ O’Brien, a futures brokerage in Chicago. “Fed policy meetings and data releases that provide an update about the likely trajectory of inflation will underpin volatility.”

©2021 Bloomberg L.P.