The U.S. Bond Market Fools Traders Once Again

Traders Are Blindsided Again by Treasuries Paying Same as Cash

(Bloomberg) -- U.S. Treasuries are, once again, proving to be a buy at almost any price.

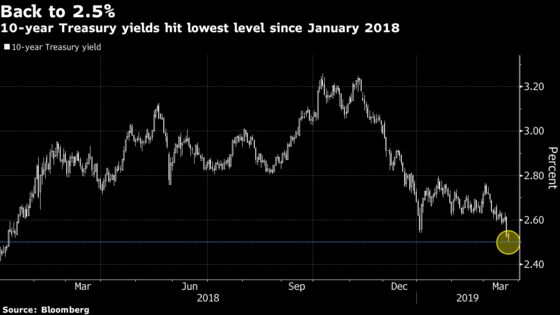

After the Federal Reserve’s surprise dovish turn this week, investors have piled into the $15.8 trillion market, leaving the 10-year note yielding less than 2.5 percent. Just a few months ago, it surged past 3.2 percent, sparking all sorts of talk -- yet again -- that this was the dawn of a new era of rising rates.

Of course, one might be forgiven for wondering who would put money in 10-year Treasuries now, particularly when you can earn nearly as much in interest on a run-of-the-mill savings account from any number of banks.

Yet for investors like JPMorgan Asset Management’s Alex Dryden, it’s perfectly sensible. The Fed’s darkening outlook about the U.S. economy is compounding worries over global growth, and few see inflation running hot enough to eat significantly into returns. If anything, the concern is that with inflation so low and growth so weak, yields will keep falling, which would make locking in today’s rates for years a smart move.

“Inflation has been persistently and stubbornly low,” said Dryden, the firm’s global rates strategist.

It’s not just in the U.S. where investors see weaker growth. In Canada, 10-year yields dropped below the overnight lending rate this week for the first time since 2008. The European Central Bank’s negative interest-rate policy means investors are still prepared to pay premiums to hold German debt due any time up to nine years from now. This month, the ECB slashed its 2019 growth forecast to 1.1 percent, the weakest in six years.

Least Bad

On Friday, disappointing data from the German manufacturing sector reinforced concerns about euro-area growth, driving investors into haven assets globally. That pushed yields on 10-year U.S. notes below the rate on three-month T-bills for the first time since the financial crisis. It’s a worrisome sign because the inversion of the yield curve, as it’s known, has reliably predicted U.S. recessions over the past half-century.

Investors around the world aren’t exactly spoiled for choice, despite the fact returns on Treasuries have actually been lousy for years. By JPMorgan Asset’s calculations, 10-year Treasuries yield more than roughly 80 percent of government debt in the developed world -- even at 2.5 percent. (That’s setting aside interest rate differentials and exchange rates, of course.)

Perfectly Rational?

Appetite for longer-dated debt has also been particularly strong among institutions such as pension funds and insurers, which are casting around for a way to match their long-term liabilities.

“In many respects, the U.S. 10-year Treasury is still, in an low-yielding world, a high-yielding asset,” Dryden said.

That’s enough for many investors, particularly after a string of poor manufacturing data and inflation reports added to worries about the U.S. economy. Stephen Bartolini, a fixed-income manager at T. Rowe Price, says the real surprise was just how little growth the Fed sees next year. Officials now forecast the economy will expand just 1.9 percent in 2020.

And if the economy ultimately does end up rolling over, price gains on holding longer-term Treasuries would be a better bet. Falling yields would force holders of short-term securities to reinvest at even less attractive rates than they would if they just held long-dated maturities.

“Rallying rates in response to what the Fed delivered,” Bartolini said, “is perfectly rational.”

--With assistance from Katherine Greifeld.

To contact the reporter on this story: Emily Barrett in New York at ebarrett25@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, ;David Papadopoulos at papadopoulos@bloomberg.net, Michael Tsang, Katherine Greifeld

©2019 Bloomberg L.P.