Traders Add Hedges for 75-Basis-Point Fed Rate Hikes, Roiling Bonds

Traders Add Hedges for 75-Basis-Point Fed Rate Hikes, Roiling Bonds

(Bloomberg) -- The dust appeared to have settled on a rocky day for U.S. interest-rate markets -- even by recent standards -- when the options market lit up late Thursday with a couple of trades anticipating the Federal Reserve will make multiple 75-basis-point rate moves this year.

While bond bears are in control, the prospect that the Fed’s six remaining policy meetings will deliver multiple jumbo rate hikes remains a minority view. Uber-bearish options structures have minimal open interest -- the number of contracts in which traders hold positions. As such, they have the potential to drive short-term rates sharply higher in a search for market equilibrium.

The combined premium on Thursday’s late eurodollar trades amounted to almost $4 million. Look for that number to grow -- and to push short-term rates higher -- if the Fed’s tune becomes more hawkish in the lead-up to its May 4 decision.

Struck at around 5 p.m. New York time, the trades involved options on September 2022 eurodollar futures, a proxy for U.S. short-term interest rates listed by CME Group Inc. Open interest in the options increased Thursday, CME preliminary data show, suggesting that the trades established new positions, as opposed to altering existing ones.

The structures offer protection from the market pricing in an additional 125 basis points of hikes -- on top of what is already priced in for the September policy meeting. Early Friday in New York, the swaps market was forecasting a policy rate 200 basis points higher than the current level of 0.33% -- near the middle of the Fed’s 0.25%-0.50% range. The options expire two days before the Sept. 21 rate decision.

The put options have strike prices around 96.00, corresponding to a rate of 4% -- equivalent to at least four 75-basis-point moves over the next four gatherings.

Related story: Libor Successor on Cusp of Overtaking Eurodollar Futures Market

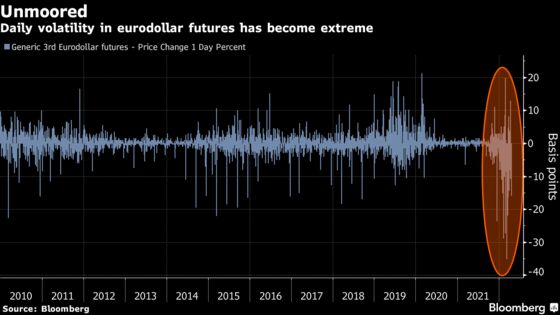

The emergence of deep-out-the-money plays can disrupt a market by creating the need for dealers to hedge their exposure, in this case by selling eurodollar futures. And there’s a wrinkle. Traders are migrating from CME’s eurodollar futures -- whose settlement rate is being phased out -- to its futures on the Secured Overnight Financing Rate, or SOFR. Shrinking participation in eurodollar futures makes it more vulnerable to large price swings.

©2022 Bloomberg L.P.