Trade Brawl Unmasks the Stock Market's Many Warts

Trade Brawl Unmasks the Stock Market's Many Warts

(Bloomberg) -- A re-erupting trade war is casting a brighter light on the rough terrain investors have been traveling all year.

Alongside the biggest rally since 1987, analysts have been cutting earnings estimates. Valuations that shrunk in the fourth-quarter meltdown have all but reinflated, amid middling growth forecasts.

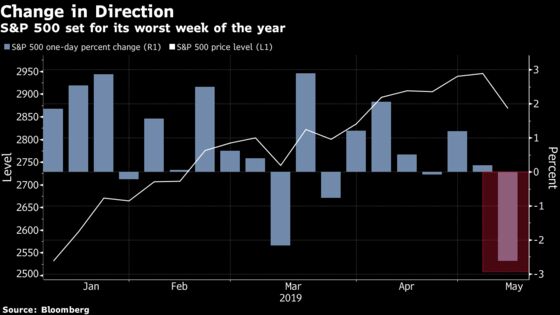

Investors are being reminded of why many professionals have stayed away from the market all year. The S&P 500 Index just suffered its worst week since December, hurt by concerns that trade tensions will make the profit and economic pictures worse.

While Treasury Secretary Steven Mnuchin may have characterized negotiations this past week as “constructive,” the new tariffs have been imposed, and China has vowed to retaliate. Few are confident about what the weekend will bring.

“We did a year’s worth of gains in four months,” said Donald Selkin, chief market strategist at Newbridge Securities Corp. “All of a sudden when you have all of these monkey wrenches being thrown into it, ‘Oh yeah, gee whiz, maybe we pushed things higher than they should’ve been.”’

Trade tensions are deepening worry around one big thing, profits, and a host of lesser ones. There was no earnings growth to speak of in the S&P 500 during the first quarter, and probably won’t be in the second or third, either. Semiconductor makers, whose market return approached 40% in 2016 and 2017, just saw profits plunge 20%.

With a 25% tariff rate instead of the current 10% level, gross margins for S&P 500 companies could shrink by 23 basis points, according to Bloomberg Intelligence. If the U.S. administration slaps the tax on all goods from China, the hit to margins could be an even larger 50 basis points.

“Commodity prices have been rising, wage costs have been rising,” David Joy, the chief market strategist at Ameriprise Financial Inc., which manages roughly $891 billion, said in an interview at Bloomberg’s New York headquarters. “If all of a sudden now other intermediate good inputs are rising, there’s all of a sudden a little pressure on margins that wasn’t there before.”

To convince themselves profit growth is salvageable, bulls must put an uncomfortable amount of faith in distant forecasts. With little expected to materialize in the first three quarters, earnings will supposedly surge 8% in the fourth, turning the full-year green. Waiting that long was never going to be easy. Doing that with China and the U.S. battling in public strikes some as impossible.

“You really need to have the global economy kick in to drive S&P earnings for the second half of the year,” Alicia Levine, BNY Mellon Investment Management chief strategist, said this week on Bloomberg Television. “If you continue with the trade war, then you’ll put earnings at risk. It’s not simply about trade. It’s the way U.S. corporates import weakness from overseas through their top line.”

Another worry is the potentially inflationary impact of tariffs, something that could push Federal Reserve Chairman Jerome Powell back into action -- a chilling thought for longs. On this point, however, Wall Street is divided. Morgan Stanley’s Hans Redeker points to last year when the first batch of tariffs took effect. Inflation stayed stable, even though the consensus view called for upward pressures due to higher import costs.

“Importers of Chinese goods tried to maintain their market share, absorbing higher tariffs via their profit margins,” he wrote. “U.S. inflation stayed stable and Chinese companies continued competing hard,not providing scope for US companies to increase their pricing power and profit margins.”

For 10 years, investors learned to live with scraps when it came to the domestic economy. Alongside the longest bull market ever has been one of the weakest recoveries of the past 50 years. While the expansion picked up in 2018, helped by President Donald Trump’s tax cuts, economists don’t see it cracking 3% for the next six quarters.

Throw in a trade war and another ominous sight -- the inverting yield curve -- and investors feel less confident about a rally that has added $2 trillion to U.S. equity prices since the start of the year. Versus its overall sales, a rough proxy for the S&P 500’s economic exposure, companies are trading at a multiple of 2.1, one of the highest since the tech bubble.

“The actual tariffs themselves are pretty small relative to the size of the economy,” said Hank Smith, co-chief investment officer at Haverford Trust, which manages $8.5 billion. “The real impact is on confidence. On business confidence, CEO confidence. So if we have an extended multi-month or even multi-quarter battle with China over tariffs, there’s going to be an impact because I think you’re going to see companies be more cautious.”

--With assistance from Elena Popina.

To contact the reporter on this story: Sarah Ponczek in New York at sponczek2@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.