Top Strategists Have a Warning for Argentina Bulls Calling Rally

Top Strategists Have a Warning for Argentina Bulls Calling Rally

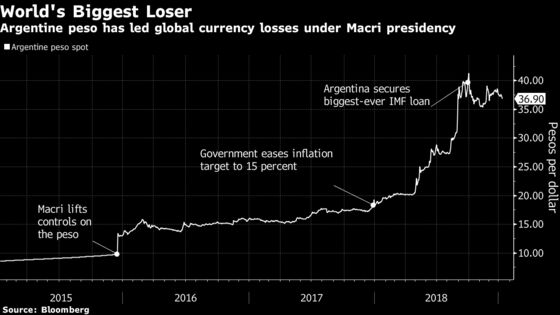

(Bloomberg) -- Since he swept to office in 2015, Argentina’s Mauricio Macri has been called plenty of names by his left-wing opponents. But the label that’s likely to sting most for an investor-friendly leader is the one applied by global currency markets: world’s biggest loser.

Wall Street cheered Macri’s decision during the first full week of his presidency to lift foreign-exchange controls, even though the peso lost about a quarter of its value that first day. They praised a move that would create a more competitive currency, boost growth and encourage foreign investment. Yet it’s all been downhill from there. The peso plunged in 2016, 2017 and 2018, bringing cumulative losses to 74 percent, more than any other currency.

Strategists who forecast last year’s selloff say that trend isn’t likely to change. The peso will fall another 20 percent this year, according to median forecasts of nine analysts surveyed by Bloomberg. The top two forecasters in the fourth quarter, Polish brokerage Cinkciarzpl and New York-based Morgan Stanley, both expect the peso to drop in the months ahead.

"There are still many, many issues," said Marcin Lipka, a senior analyst at Cinkciarzpl in Zielona Gora, a city in western Poland. He expects the currency to slide about 26 percent to 50 per dollar by year-end. "There’s strong demand from the population to lose some of the belt-tightening. Inflation will still probably be around 30 or 40 percent, which will push the currency lower."

That pessimism runs counter to fund managers and strategists including Franklin Templeton, Man Group and TIAA Bank, who argue the selloff created a buying opportunity for Argentine assets. Bulls got a boost late last year when the nation reported its first trade surplus in almost two years and the peso began to stabilize.

It’s also true that the central bank’s new monetary policies, implemented in October, have smothered most foreign-exchange volatility and given policy makers confidence they can rebuff speculators. The peso strengthened more than 11 percent since the end of September, and on Thursday, the currency actually got too strong, prompting the central bank to buy dollars to keep it within a predetermined trading range.

Yet bears have their own compelling case. Macri is seeking re-election this year and trying to dig his nation out of its second recession in three years while sticking to the terms of the largest-ever International Monetary Fund bailout. With that backdrop, it may be unrealistic for the peso to get back on track.

Economists polled by Argentina’s central bank are slightly more optimistic than Lipka. They raised their estimate for the peso to 48.3 per dollar by the end of 2019, stronger than a prior forecast, according to a December survey. It’s trading at about 37 per dollar now.

One caveat to the gloomy outlook: Strategists including Morgan Stanley’s James Lord, the second-best peso forecaster in the fourth quarter, say that while the currency will probably decline this year, it offers high carry relative to peers. That makes certain Argentine assets attractive, he said. Kathryn Rooney Vera, the head of research at Bulltick in Miami, agrees.

"The carry is massive," she said. "It will be a disproportionate beneficiary of a return to positivity for EM."

The currency turmoil isn’t entirely Macri’s fault. He inherited a government locked out of global markets after his predecessors, Nestor Kirchner and then his wife, Cristina Fernandez de Kirchner reneged on debts, got censured for publishing bad statistics and used ever-shifting restrictions to block imports.

Lipka, a Warsaw native, said he sees similarities to his 1980s childhood, when Poland tumbled into financial crisis during the final years of communist rule and the ensuing economic and political liberalization coincided with a steep depreciation of the zloty. Macri will probably make some policy concessions this year to help secure a second term in office, putting even more pressure on the currency, according to Lipka.

"Markets are still feeling the pain from 2016 and 2017, when they trusted the reforms would be swift," Lipka said. "There’s still more pain to be felt."

--With assistance from Carolina Millan.

To contact the reporter on this story: Ben Bartenstein in New York at bbartenstei3@bloomberg.net

To contact the editors responsible for this story: Rita Nazareth at rnazareth@bloomberg.net, ;Jeremy Herron at jherron8@bloomberg.net, Alec D.B. McCabe, Brendan Walsh

©2019 Bloomberg L.P.