Top Returns Don't Make Russia's Bonds Any Less ‘Unanalyzable’

Top Returns Don't Make Russia's Bonds Any Less `Unanalyzable'

(Bloomberg) -- The largest ruble-debt auction on record, almost half a trillion dollars in reserves, and the best local-bond returns in emerging markets. All facts about Russia that Matthew Murphy says play second fiddle to the risk of sanctions.

The world’s biggest energy exporter is “fairly unanalyzable” with the threat of a U.S. ban on new sovereign bonds in play, according to Murphy, a Boston-based portfolio manager at Eaton Vance, which has $493 billion under management. Its local-currency bond fund for emerging markets outperformed 91 percent of peers in the past five years, according to data compiled by Bloomberg.

“We’re not sure what the U.S. administration is going to do,” he said. “Prohibiting western investors from owning Russian debt would be a very extreme event, but just because it is extreme does not mean that its probability is low. We think it is possible.”

The threat that Washington could hobble the local bond market has prompted investors including Eaton Vance, Ashmore Group Plc and Morgan Stanley Investment Management to cut their exposure to Russia. For others, the nation’s investment-grade credit score and high real yields are impossible to resist, while its low debt levels and growing reserves offer the hope that the economy is effectively sanctions-proof.

Fragile Gains

The optimists have driven a rally that’s seen ruble-denominated bonds deliver a 7.5 percent return so far this year, even after the U.S. Senate renewed a bill last month seeking more penalties on Russia for alleged elections meddling. The currency is up 5.7 percent in 2019, the best rally globally. According to Murphy, investors could easily see those gains flip to the kind of double-digit loss posted last year if geopolitical tensions worsen.

“They’re probably feeling great now,” he said. “They might regret it later.”

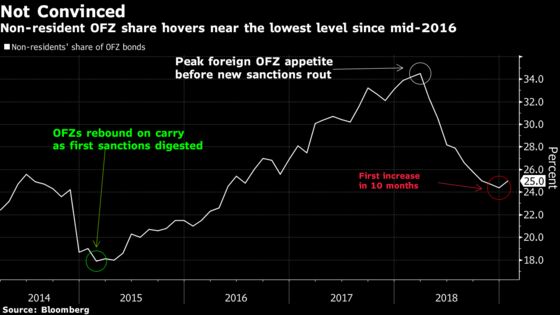

Foreigners’ share of ruble notes, known as OFZs, rose in January for the first time since March, according to the latest data from Bank of Russia. At 25 percent, the non-resident portion of Russia’s local debt is still far from its 34.5 percent peak.

“The fear of sanctions is off the table for now, but it won’t take much congressional action or administration preemptive action to return this risk to the front burner,” said Richard Segal, senior emerging-markets analyst in London at Manulife Asset Management, which oversees $364 billion. “If new sanctions in the U.S. do reach a congressional vote, the reality will set in that there is no place for these bonds to go."

‘Favorite’ Banker

Dovish noises from the Federal Reserve and other central banks mean the global hunt for yield is back on and a “wall of money” is heading for developing markets, according to the Institute of International Finance. Locally, the Russian market has been bolstered by government pledges of support in the event of tougher penalties as well as signals that the central bank may start easing rates as soon as this year.

For Jan Dehn, it’s not enough.

“My favorite central banker in the world is Elvira Nabiullina,” Ashmore’s head of research in London said, referring to the governor of the Bank of Russia. “But we have been reducing and continue to reduce exposure to Russia. We should see more sanctions, and no end to them, and we are not interested in locking our clients into some bonds that they can’t get rid of.”

--With assistance from Maria Kolesnikova.

To contact the reporters on this story: Selcuk Gokoluk in London at sgokoluk@bloomberg.net;Artyom Danielyan in Moscow at adanielyan@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, Alex Nicholson

©2019 Bloomberg L.P.