Timing Is Key for Indonesia’s Second Rate Cut: Decision Guide

Timing Is Key for Indonesia’s Second Rate Cut: Decision Guide

(Bloomberg) -- Indonesia’s central bank is ready to cut interest rates for a second time this year, but most economists aren’t convinced it will come as soon as Thursday.

Pressure is building on policy makers to provide additional stimulus to Southeast Asia’s biggest economy in the face of ongoing trade tensions and fears of a U.S. recession. Having already cut rates last month, Bank Indonesia Governor Perry Warjiyo has made it clear that more easing is in the pipeline.

However, heightened market turmoil and a weakening currency may give the central bank reason to pause for now. Of the 34 economists surveyed by Bloomberg, 21 are predicting Bank Indonesia will leave its benchmark interest rate unchanged at 5.75%, while the rest see a 25 basis-point reduction.

“BI will not rush into another rate cut,” given plenty of risks, such as U.S.-China trade tensions, geopolitical threats and pressures in emerging markets like Argentina, said Nomura Holdings Inc.’s economist Euben Paracuelles. “A pause would be prudent and consistent with BI still placing top priority to its stability objective,” he said.

The central bank has plenty of reason to ease policy though. The Federal Reserve cut interest rates last month, and traders predict there’s more easing to come. Inflation in Indonesia also remains benign, while growth is under pressure.

Here’s what to look out for in Thursday’s policy decision:

Growth Concerns

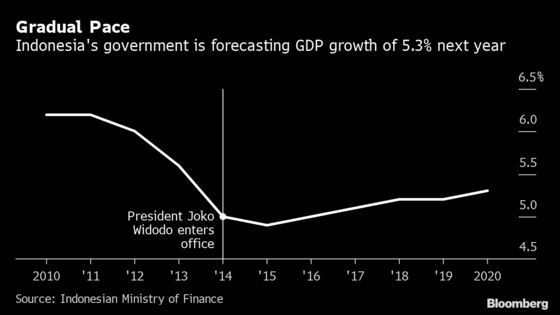

Bank Indonesia lifted its benchmark rate six times last year -- by a total of 175 basis points -- to fend off an emerging-market rout. This year, its focus has shifted, from stabilizing the currency to supporting growth.

After winning a second term in office, President Joko Widodo is spending billions on infrastructure to push the growth rate up to 5.3% next year. That’s still a far cry from the 7% he pledged in his first term.

Finance Minister Sri Mulyani Indrawati last week warned of downside risks to the 2020 growth forecast coming from a global slowdown.

“Given the recent inversion in the yield curve, the global bond markets are telling us that many central banks are behind the curve, particularly in responding to the global economic slowdown, and that is the risk that Bank Indonesia cannot afford to ignore,” said Satria Sambijantoro, an economist from PT Bahana Sekuritas in Jakarta.

Current Account

The current account deficit remains a risk for the economy and is one of the reasons why the central bank isn’t in a rush to cut interest rates. The deficit means Indonesia is reliant on foreign inflows to finance its import needs, and lower interest rates would make local yield assets less appealing to international investors.

The deficit widened to 3% of gross domestic product in the second quarter from 2.6% in the previous three months.

“A further unwind of tight monetary policy is in the offing but we suspect that BI would only be comfortable matching the same pace of rate cuts as the Fed for now,” said Philip Wee, a currency strategist at DBS Group Holdings Ltd. “External funding risks are still a concern in the current volatile environment.”

Market Turmoil

A sell-off in global markets has hit Indonesia’s rupiah, which is down 2.2% against the dollar in the past month. The central bank has repeatedly intervened in recent weeks to contain the fallout, with the rupiah still 1% higher against the dollar so far this year.

Bahana Sekuritas’s Sambijantoro said the bond market is already pricing in a rate cut on Thursday and “as we learned from latest surprise rate cuts in Thailand and Chile, sometimes traders know something that economists overlook,” he said.

--With assistance from Tomoko Sato.

To contact the reporter on this story: Karlis Salna in Jakarta at ksalna@bloomberg.net

To contact the editors responsible for this story: Nasreen Seria at nseria@bloomberg.net, ;Thomas Kutty Abraham at tabraham4@bloomberg.net, Michael S. Arnold

©2019 Bloomberg L.P.