Tiffany & Co. Could Attract Other Suitors Beyond LVMH

Tiffany & Co. Could Attract Other Suitors Beyond LVMH

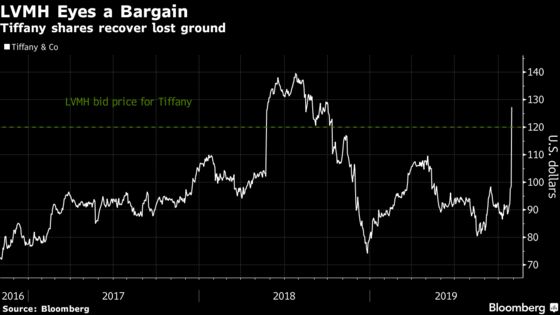

(Bloomberg) -- Tiffany & Co. may attract rival bids, analysts said, after the jewelry maker said it was reviewing an unsolicited $120 per-share bid from French luxury conglomerate LVMH.

Tiffany shares climbed as much as 30% on Monday, their biggest single gain ever, to the highest in a year. The confirmation of talks followed a Bloomberg report that the French company has offered about $14.5 billion. For LVMH, an acquisition has strategic logic as it would increase the company’s exposure to the U.S. market, analysts said, noting that LVMH has a strong track record in M&A.

Shares of the French company gained as much as 1.5%, boosting other luxury stocks in the region.

Here’s what analysts had to say about a possible deal:

KeyBanc, Edward Yruma

(Rates Tiffany overweight, raises PT to $125 from $115)

- Continuing consolidation in luxury makes sense given the shift to e-commerce, importance of the Chinese market, and likely synergies.

- Notes that LVMH could accelerate Tiffany’s growth in Europe and Asia, and says there are “significant real estate and marketing synergies that can be unlocked.”

- Deal looks “reasonable” in $125-$130 range; Richemont (owner of Cartier, strong presence in hard luxury) or Kering (need to diversify into hard luxury, owns Pomellato) could likely also look at Tiffany.

Deutsche Bank, Francesca Di Pasquantonio

(Upgrades Tiffany to buy from hold, PT to $130 from $100)

- An approach is credible, given the appeal of the sector.

- Tiffany management and board are likely to have a high bar in regards to any approach due to the company’s strong brand equity, the argument that earnings and margins are currently depressed, and the potential for a third party to get involved.

Cowen, Oliver Chen

- Tiffany deserves an “exceptional premium” of 20x Ebitda or higher (or $160/share), similar to Bvlgari and Versace transactions, as margin and growth opportunities at Tiffany are “substantial.”

- LVMH has ample financial capacity for a deal; expects many strategic and financial synergies given margin expansion.

- Says other factors to consider include: potential interest from other luxury players such as Richemont, other financial and strategic bidders, a leveraged or management buyout, and risk that deal doesn’t materialize.

Bank of America Merrill Lynch, Geoffroy de Mendez

(Rates LVMH buy)

- $120/share price would value Tiffany at 3.2x EV/sales, which is slightly higher than the valuation paid for Bulgari by LVMH in 2011.

- If a deal were successful, it would mean LVMH’s U.S. exposure would rise to 26% and would almost double the size of its watches and jewelry unit to EU8.4b.

- Notes that LVMH has been a leader in sector consolidation, and if the potential deal goes through, will likely lead to more M&A in industry.

RBC, Rogerio Fujimori

(Rates LVMH outperform)

- Tiffany could become a better company and stronger competitor under the LVMH umbrella, analyst says, citing the success of Bulgari.

- Purchase also makes strategic sense for LVMH, as jewelry is among the most attractive categories in luxury, yet the company isn’t a leader.

- Other perceived takeover targets in the sector may get some support from the news.

Bernstein, Luca Solca

(Rates both LVMH & Tiffany outperform)

- Tiffany takeover could make sense for LVMH, given the potential in the brand, and as it would give the French company a more balanced exposure to the U.S. market.

--With assistance from Janet Freund.

To contact the reporter on this story: William Canny in Amsterdam at wcanny3@bloomberg.net

To contact the editors responsible for this story: Celeste Perri at cperri@bloomberg.net, Beth Mellor, Monica Houston-Waesch

©2019 Bloomberg L.P.