Three Crises Leaves Brazil’s Assets a Long Road Back to Recovery

Three Crises Leaves Brazil’s Assets a Long Road Back to Recovery

(Bloomberg) -- Brazil’s stocks and currency clocked up the biggest losses in the world as the coronavirus pandemic ravaged the nation during the first half. And few are brave enough to say it’s going to get much better in the second half.

Battered by the second-highest number of Covid-19 cases in the world -- over 1.6 million -- President Jair Bolsonaro’s administration is struggling to put the economy back on track less than a year after the approval of a pension reform plan fueled optimism the country was on the way back from decades of profligacy.

Even when the pandemic passes, the government will have to undo a series of stimulus measures to meet its fiscal targets, before convincing lawmakers to revive plans to overhaul the tax system and move forward with state-asset sales. In the meantime, the government has lurched from one political crisis to another as the virus ravages the country.

“Brazil entered the current crisis with little room for stimulus and it will end up in a worse fiscal situation,” said Aurelio Bicalho, chief economist at Sao Paulo-based Vinland Capital. “The high level of public indebtedness heightens risk perception.”

The Economy Ministry expects the government’s gross debt to reach 98.2% of gross domestic product this year, a 22.4-point increase from 2019. Not good news for a country trying to fix its fiscal accounts.

Century Recession

Virus cases are rising faster in Latin America than anywhere else in the world and the World Bank expects the region to face the worst recession since at least 1901. While Brazil’s GDP is expected to shrink less than peers like Mexico, its assets were hit hard.

Analysts surveyed by the central bank expect the Brazilian real to end the year at 5.20 per dollar, 1.6% stronger than current levels, but still about 23% down in 2020. It hasn’t fallen that much since 2015, when President Dilma Rousseff was impeached.

The currency has nosedived as falling interest rates diminish its carry appeal. While it has retraced some of its losses from an all-time low in May, its implied volatility suggests traders are bracing for more swings.

“They are facing three crises at the same time,” said Juan Prada, a currency strategist at Barclays in New York, pointing to the pandemic, the economic contraction and the political situation. “All of these aspects point to downside risk for the currency.”

Stocks Upside

The Ibovespa stock index fell 18% in the first half and strategists see room for some gains in coming months as the low-rate environment is expected to drive inflows. On average, they predict the benchmark will finish the year at 100,000, a Bloomberg survey showed. While that’s an 1% advance from where it stood at the end of June, the gauge would still be stuck with a loss for the year of 13.5%.

Stocks would have fallen still further if the central bank hadn’t cut rates to a record low.

“Brazil’s key rate will likely be at stimulative levels for a good time, which leaves real assets such as equities with greater upside,” said Marco Antonio Mecchi, a 25-year market veteran who helped found MZK Investimentos in Sao Paulo.

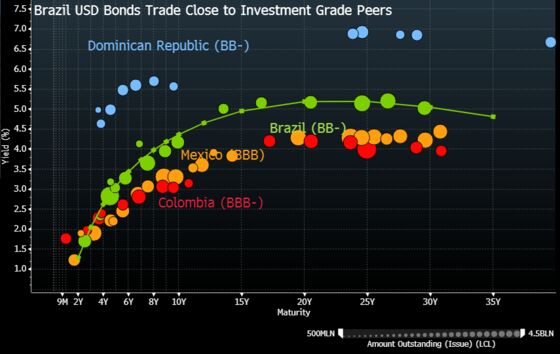

Tracking Peers

Unlike other assets, Brazil’s bonds moved in line with peers in the first half, as $350 billion in international reserves gave comfort to bondholders. The nation’s dollar bonds have returned losses of about 0.9% this year, similar to their emerging-market peers.

“We should expect about the same performance as in the past six months,” said William Snead, an analyst at BBVA in New York. “There is not much upside in the short term.”

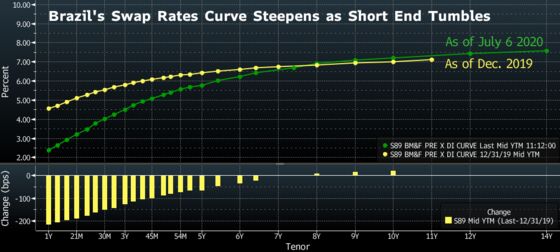

Fiscal and Monetary

Swap-rates traders are focused on the mounting fiscal burden, which could hit the long end of the curve.

In the first half, the curve steepened as the central bank cut rates more aggressively than expected. Short-term rates fell more than 200 basis points while longer rates rose 30 to 40 basis points. Officials have signaled the end of the easing cycle is near and the curve is pricing in less than 50% chance of a final 25 basis point rate cut in August.

“There remains risk that the central bank could embark on more aggressive easing measures, in addition to what they already have taken,” said Sacha Tihanyi, the deputy head of emerging markets strategy at TD Securities in Toronto. “What will be important is the speed at which the government returns fiscal accounts to pre-Covid levels.”

©2020 Bloomberg L.P.