This U.K. Bond Trend Is Seen Powering Ahead, Brexit Deal or Not

This U.K. Bond Trend Is Seen Powering Ahead, Brexit Deal or Not

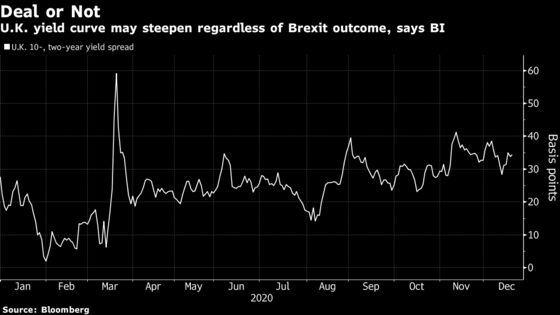

(Bloomberg) -- Britain’s yield curve will probably steepen next year, regardless of whether the U.K. and European Union agree on a trade deal.

“No-deal means an increased chance the Bank of England takes policy rates negative, bull-steepening the curve,” said Tanvir Sandhu, chief global derivatives strategist at Bloomberg Intelligence. “Meanwhile, a deal outcome may see a constrained bear-steepening move.”

In other words, failure to reach a trade agreement would fuel demand for two and five-year debt, the bonds most sensitive to interest-rate moves, on the assumption that the BOE would likely cut borrowing costs. A Brexit accord would prompt traders to unwind their haven plays, which typically results in the yield on longer-term bonds rising faster than those at the front end.

Either way, the bond yield curve will rise. The yield gap between two and 10-year government bonds is already headed for its first annual increase since 2013 due to the damage inflicted by the coronavirus pandemic, rising six basis points to 33.

Britain’s chief Brexit negotiator David Frost said Thursday that progress in the talks has been blocked, and European Commission President Ursula von der Leyen warned that the two sides still face big obstacles, particularly on fishing, that may prove insurmountable.

The caveat is that even if the U.K. enters a free-trade agreement with the EU, 4% would be shaved off the nation’s gross domestic product in the long run compared to where the economy would’ve been if Brexit never happened, the Office for Budget Responsibility estimates forecasts. And failure to reach a deal, which means adopting World Trade Organization rules, would entail another 1.5% loss in GDP and spur bets the BOE will cut interest rates.

BOE policy maker Gertjan Vlieghe said Friday that the central bank should be prepared to add monetary stimulus including negative rates to complete the economic recovery from the pandemic. Money markets have brought forward bets for interest-rate cuts, currently pricing 10 basis points of easing to 0% in March 2022 compared to nine basis points earlier Friday.

Week Ahead

- There are no euro-area or U.K. bond sales, redemptions or coupon payments scheduled until January

- European Central Bank and BOE pause their respective debt-buying programs until next year

- Consumer confidence numbers are the only major data releases from the euro zone and Germany next week

- U.K. is slightly busier as mostly second-tier, backward-looking data are crammed in ahead of the festive break including government borrowing numbers for November on Tuesday

Policy-maker speeches are few and far between with Mario Centeno set to speak in Portugal’s parliament on Tuesday and the ECB publishing its economic bulletin on Thursday

- There are no BOE policy maker speeches scheduled for next week

- There are no major sovereign ratings announcements scheduled for the remainder of the year

©2020 Bloomberg L.P.