The U.S. Shouldn’t Get Too Creative With Debt Sales

The U.S. Shouldn’t Get Too Creative With Debt Sales

(Bloomberg Opinion) -- It was with a sense of déjà vu that I read that U.S. Treasury Secretary Steven Mnuchin has asked the Treasury Borrowing Advisory Committee to cobble some together ideas on new sorts of debt securities the government could create and sell to finance the rapidly expanding budget deficit. The implication is clear: The U.S. needs to attract new investors to buy the more than $1 trillion of debt it’s likely to need to issue in 2019 and in years to come.

Or does it? There is much evidence to suggest there will not only be ample demand for Treasuries in coming years, but for the type of debt the government is already issuing without needing to reinvent the wheel.

Let’s begin with ideas that have been floated in the very recent past. Shortly after President Donald Trump took office, Mnuchin brought up the idea of ultra-long-term bonds with 40-, 50- and even 100-year maturities. Canada has issued 50-year bonds out there, as has Great Britain and even fiscally challenged Italy. Belgium and Mexico have issued 100-year bonds. In fact, at 5.75 years, the average maturity of U.S. debt is on the low side.

The idea here is that the Treasury could readily add to the average maturity without causing much consternation. Other nations have proven that there an appetite, presumably from international pensions funds and insurance companies seeking assets to match against long-term liabilities. Issuing longer-term debt is hardly out-of-the-box thinking.

The compulsion to consider securities that expand demand for U.S. debt is, of course, vital. But at the moment, the ballooning deficit has had surprisingly little market impact. Treasury 30-year bonds yield about 3 percent, which is about where they were when Trump took office. Also, the difference between two- and 30-year Treasury yields is about 50 basis points, narrower by some 130 basis points. What better time to start issuing longer-term debt?

Also, there’s reason to expect steady domestic demand no matter what form any new Treasury debt will take. At about 40 percent currently, Treasury market’s share of taxable debt is seen by the Congressional Budget Office as rising to about 50 percent in a decade or so. But given the rise in passive bond investing relative to active investing, investors will have to buy Treasuries merely to match their benchmarks.

There will be no shortage of ideas, and most will seem rather obvious in the sense they’ll largely be variations of the themes already suggested. I mean, Treasury debt is Treasury debt. So, in the mix is ready talk of longer-maturity floating rate notes, perhaps 15- or 20-year bonds, bonds with rates that are tied to health-care or education costs, and even zero-coupon bonds.

None of that is really exciting in terms of innovation. For that, the Treasury might want to look at older ideas. How many remember “Flower Bonds”? Those were bonds that couldn’t be redeemed until a person died, at which point they matured at par with the proceeds to pay federal estate taxes — when we still had estate taxes! Maybe the time is ripe for the U.S. to up the ante on estate taxes, and so take in more revenue, and then offer new Flower Bonds — or their cannabis equivalent — to raise money.

There is also a potential demographic audience for U.S. debt. Savings bonds bought for kids can be redeemed tax-free, on the accrued interest, if used for education. Perhaps savings bonds with similar characteristics could be used for targeted retirement accounts. The idea is you can buy such bonds and redeem them tax-free if the proceeds fund retirement. It’s a bit like a Roth IRA targeted to a bond audience with the goal of enhancing a Treasury market customer base. The Treasury could do the same for a bond tied to health care, sort of like a Treasury-sponsored Flexible Spending Account.

Here’s one for the history books: a bond tied to a commodity or currency. The idea here is that you buy the bond but can convert it to something else. The Confederates did it with something known as the Erlanger Cotton Bond, which was payable in either rebel dollars, cotton or French francs. (If you wanted the cotton, you had to run the Union blockade to get it. Maybe Bitcoin is a way around that today.) There was huge demand because the terms were generous, but as the one I own in my collection shows, there are still coupons left unpaid starting in April 1865.

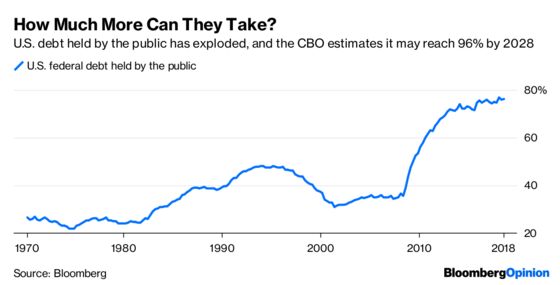

We maybe musing about new sorts of Treasury debt, but the sheer magnitude of what’s coming scares me. Putting the various ideas aside, with debt likely to rise to near 100 percent of GDP in less than 10 years from about 75 percent currently, I imagine that the interest rates offered will be the main attraction.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Ader is the former chief macro strategist at Informa Financial Intelligence and held similar roles at CRT LLC and RBS/Greenwich Capital. He was the No. 1 ranked U.S. government bond strategist by Institutional Investor magazine for 11 years, and was No. 1 in technical analysis for five years.

©2019 Bloomberg L.P.