The Stocks-Only-Go-Up Strategy Falls Into a $2 Trillion Ditch

The Stocks-Only-Go-Up Strategy Falls Into a $2 Trillion Ditch

(Bloomberg) -- Recent converts to a one-way trading blueprint popularized on Twitter and in chat rooms have learned it is not quite the bullet-proof strategy it had recently seemed.

“Stocks only go up” was the philosophy, and however tongue-in-cheek the intent, it got a jarring refutation Thursday as the S&P 500 plunged 6% and almost $2 trillion was erased from equities. Selling was worst in areas of the market embraced by armies of retail investors that have swarmed to equities in the last month, including airlines, energy producers and banks.

While the slide is still small next to the advance that lifted the S&P 500 by 45% since late March, at the very least it highlights the shaky foundations of a rally occurring alongside the worst economy in a generation. Small traders who dived in over the last few weeks absorbed their first big dose of pain. Whether they stick around now will go a long way in determining the tenor of the next few weeks.

“Retail piled into this trade in a relatively major way,” said Mike Mullaney, director of global markets research at Boston Partners. “How are they feeling today? Crappy, really lousy. They’re questioning whether this is a sustainable move.”

In some markets, a day like today might entice bargain hunters, or at least investors who doubt the intrinsic value of U.S. companies is likely to change by $2 trillion in just 6 1/2 hours. And yet, nothing that happened Thursday has made the market particularly cheap, a fact that could bode poorly for bulls’ long-term health.

Had Thursday’s selloff happened in 2019 instead of 2020, it would’ve been the biggest decline in eight years. But after it was over, the S&P 500’s forward valuation was still 13% higher than in February, when the virus crash began. It’s cheaper, but not at levels where bargain hunters would normally materialize.

Based on forecast earnings for the next 12 months, the S&P 500 was trading at a multiple roughly 1.5 points lower than Monday. But at 21.3, the ratio remains almost 2 points higher than where it was at its previous peak in February. In other words, if stocks were too expensive to own relative to earnings before the March meltdown, the valuation case hasn’t gotten enormously better.

“There has been a disconnect between the market and how the economy is doing,” Giri Cherukuri, head trader and portfolio manager at Oakbrook Investments LLC in Lisle, Illinois, said by phone. “This is just a small pullback after a large gain. I don’t think it’s a buying opportunity yet. P/E is still very high.”

Almost nothing was spared in the selloff -- but airlines, cruise operators and travel companies that surged in recent weeks bore the brunt. Among the hardest-hit were American Airlines Group and Carnival Corp., each of which slumped more than 15%. Brick-and-mortar retailers including Kohl’s Corp. and Nordstrom Inc. fell at least 11%.

Many of the tiniest of buyers -- who chased after recovery plays and insolvency stocks -- are likely feeling the pain. Chinese real-estate firm Fangdd Network Group Ltd., known by its ticker DUO, has since Tuesday lost near 75%.

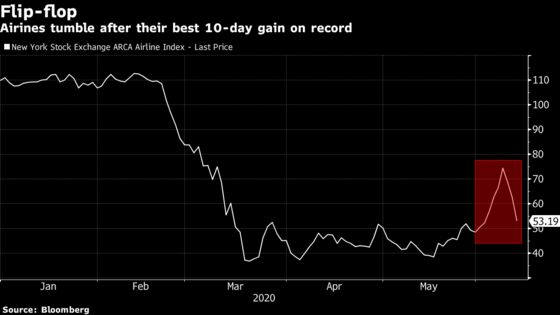

It’s a stark reminder of how quickly sentiment can sour. As for retail investors, while their recent foray into beat-down stocks like airlines showed some propensity for bargain hunting, their conviction has proved less sticky. The NYSE Arca Airline Index just tumbled 29% over three days, paring a 10-day, 65% rally that’s the best on record.

P/E ratios are historically a good gauge of valuations in the long-run, says Dan Skelly, Morgan Stanley Wealth Management’s head of market research and strategy. However, in the short-run “it can be very useless,” he said by phone. “It can be swayed by sentiment and by macro headlines and by any news of the day.”

Skelly points out when P/Es bottomed during the March crash, they were still 30% higher than the trough reached during the 2008 crisis. “That’s the case because interest rates were that much lower,” he said. “And the reason interest rates were that much lower was because rates were already on a declining path for some time.” But, assuming 2021 recovery earnings in the $150- to $160 range still yields “pretty rich” valuations on an absolute basis, he said.

Until recently, valuations were an after-thought for investors picking stocks. For institutional investors, a more important factor was a company’s ability to boost sales and profits amid all the economic woes. They’ve piled into tech giants and health-care stocks, betting that demand for automation and a virus cure would let them to weather the health crisis. Appetite was so strong that the Russell 1000 Growth Index was trading at the highest premium to the market since the dot-com era.

Instead of tempting traders, being cheap is viewed as being risky. A Dow Jones U.S. Thematic Market Neutral Value Index, which buys the least expensive against most expensive stocks, has tumbled 10% since Monday, the most over comparable periods in data compiled by Bloomberg.

Still in question for many are what earnings will look like this year. Analysts expect S&P 500 components to make $127 per share in 2020, data compiled by Bloomberg Intelligence show. That’s down from a forecast of $136.20 in mid-April. Among Wall Street strategists, the bleakest of calls predicts EPS of $50 this year.

New York Life Investments’ Lauren Goodwin, who is the firm’s economist and multi-asset portfolio strategist, says the economy -- and the market -- face an enormous amount of demand destruction. But, she says, “even if Fed programs can support risk assets, if there is no real aggregate demand you can’t pull up earnings.”

©2020 Bloomberg L.P.