Foreigners Ignore Downgrade to Junk and Snap Up Colombian Bonds

Foreigners Ignore Downgrade to Junk and Snap Up Colombian Bonds

(Bloomberg) -- As Colombia was getting cut to junk in the second quarter, and the finance minister was quitting over a failed tax bill and deadly protests were raging, an odd thing happened in the local bond market: Foreigners piled in at the fastest pace on record.

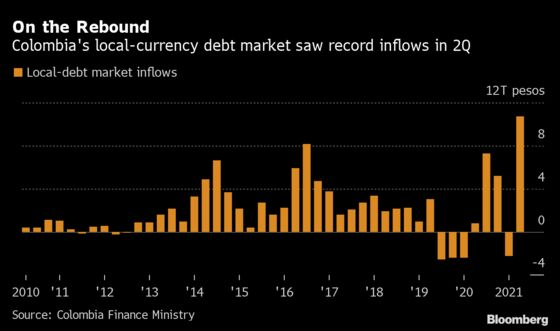

Net inflows surged to an unprecedented 10.8 trillion pesos ($2.8 billion) in the three months through June, a full 30% above the previous quarterly high set in 2016. And the notes have begun to outperform Andean peers in recent weeks after a rough start to the year. Investors have been impressed by the government’s pledges to right the ship after losing investment-grade status, and faster economic growth should help fortify government coffers, according to Alejandro Arreaza, an analyst at Barclays Capital Inc.

“The economy is recovering faster than what the market had been expecting, and that can also gradually help improve the fiscal situation,” Arreaza said from New York. The selloff earlier this year “was somewhat overdone and we’re seeing a correction.”

The growing appetite for Colombian debt shows investors looking beyond credit ratings, lured by yields topping 6% in a world with more than $15 trillion of debt that investors pay for the privilege of owning. While that sentiment could change as global interest rates rise, Colombia -- at least for now -- has impressed bondbuyers with its commitment to regain investment-grade status and stimulate the economy after last year’s downturn.

Finance Minister Jose Manuel Restrepo, who took over in May, said he “was positively surprised” when he met with more than 50 investors on a trip to the U.S. this month aimed at bolstering confidence in Colombia.

“They expressed their interest in continuing to invest in our country, continue to see that Colombia generates and has opportunities,” he said in an interview after the visit. “We are a responsible country and we are responding to the need for stability in public finances.”

The government isn’t backing away from its plan to raise taxes despite the street protests it sparked earlier this year as it looks to wrangle a fiscal deficit expected to reach 8.6% of gross domestic product in 2021. It’s proceeding with asset sales that should provide a one-time lift to finances, and also seeking to eliminate a levy on bonds to lure more foreign investors.

Amid all the government’s efforts, Barclays forecasts the economy will grow 9% this year, after contracting 6.8% in 2020. Meanwhile, the central bank last month boosted its forecast for expansion in 2021 to 6.5% from 6%, citing the economy’s strong performance in April.

Colombia’s record bond-market inflows are even more surprising when compared with regional peers. Both Peru and Chile have seen outflows from their domestic notes this year, according to data from the Institute of International Finance.

So far the performance for Colombia’s bonds hasn’t caught up with the rush of money coming into the market. While the notes have stabilized since the start of May, for the year they’re still down 14% in dollar terms, compared with an average loss of just 1% for emerging-market local notes.

Gorky Urquieta, a money manager at Neuberger Berman in Atlanta, predicts the nascent rebound in Colombian bonds will pick up speed. His firm has a slight overweight position on the local notes, attracted by the country’s history as a reliable debtor and relatively high returns, he said.

After the downgrades, the government has demonstrated that it’s committed to sticking with the fiscal discipline for which it is known, according to Urquieta.

“Colombia has a long track record of being a very stable, predictable country,” he said.

©2021 Bloomberg L.P.